Entity identity

Share this article

Neil Warren considers the partial exemption de minimis rules and how these might produce a VAT windfall for some buy-to-let landlords of residential property

Key Points

What is the issue?

A business cannot normally claim input tax on costs that relate to activities that are exempt from VAT. However, if the tax amounts come within certain limits, it might still be claimable by using the partial exemption de minimis rules.

What does it mean to me?

There might be scope to identify clients who can claim input tax on exempt activities such as costs related to buy-to-let residential property by using the de minimis limits. Any past overpayments (errors) can be corrected going back four years.

What can I take away?

Always be clear that VAT issues are based on the ‘legal entity’ of an activity. And for partial exemption issues, the annual adjustment figures always override the monthly or quarterly calculations made on returns during the year.

I t seems to me that buy-to-let landlords have had some challenging tax issues to deal with in recent times. The phasing out of higher rate tax relief on interest payments; the new 3% SDLT charge on second properties and the ending of the wear and tear allowance for furnished properties (10% of rental income) are the main ones that spring to mind. However, there might be some good VAT news to share in these troubled times by considering the partial exemption de minimis rules and how these sometimes work in favour of a business that has two activities and where the second activity generates exempt income (such as buy-to-let rental income) and is a smaller part of the overall business activity.

Legal entity issues

VAT is a tax where the starting point is often the legal entity. So if Janet is a sole trader with three different sources of taxable income, then she will be liable to pay output tax on all of her sales if she is VAT registered and if all income is earned within her sole trader entity. And if she is not VAT registered, then she must take into account all sources of business income as far as the registration threshold is concerned. The key phrase in the legislation is ‘taxable person’, i.e. sole trader, partnership, limited company etc – rather than ‘taxable business.’

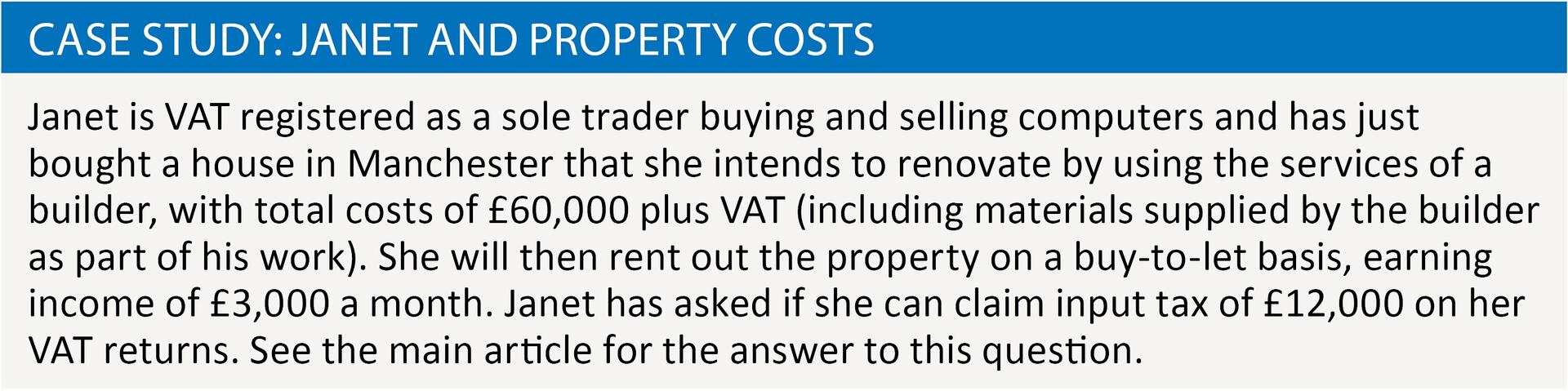

To illustrate the key issues with the partial exemption de minimis rules, let me introduce a case study based on Janet from the previous paragraph. See Case study: Janet and property costs. Your initial answer might be ‘no way’ but my answer is ‘yes, if the timing of the work is planned correctly’. Read on and all will be revealed.

Jointly owned property

Before I progress with the Janet story, don’t forget that an important principle of VAT and property is that jointly owned property (say between a husband and wife) is classed as a partnership. I still talk to accountants who think that a jointly owned property represents two sole trader arrangements, where each sole trader has 50% of the property as far as his VAT issues are concerned. This is not correct: see HMRC VAT Notice 742, para 7.2.

Input tax block: exempt supplies

Having established that Janet is the sole owner of her property in Manchester, i.e. it is the same legal entity as her VAT registration, the next stage is to consider the challenges of partial exemption:

- A basic principle is that input tax cannot be claimed on costs that are directly relevant to exempt supplies. And rental income from residential property is always exempt from VAT – there is no scope to charge VAT on residential property income with an option to tax election as is the case with commercial property (or at least an option to tax election is possible on the building, but its impact is then overridden in relation to residential income – see HMRC Notice 742A, para 3.1).

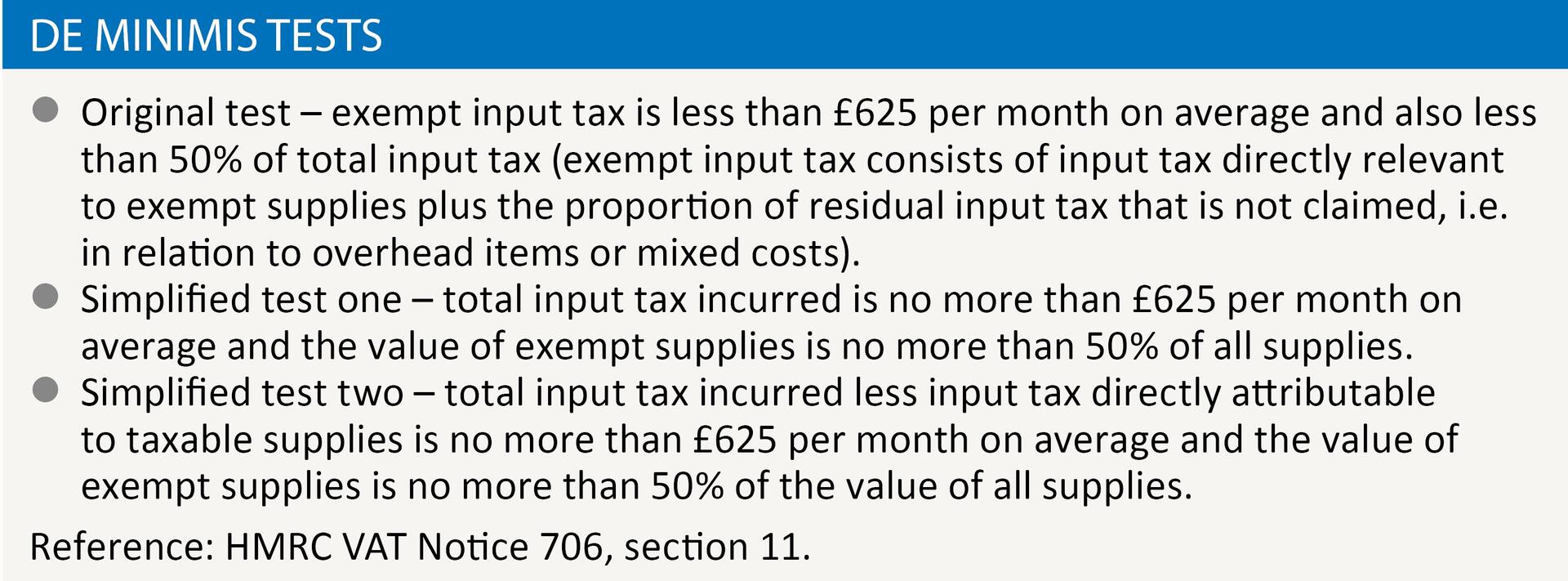

- The good news is that there is a window of opportunity to claim input tax on exempt costs by taking advantage of the partial exemption de minimis rules, where a claim can still be made on exempt expenditure, as long as the total VAT is less than certain limits. There are three tests, which I have shown in De Minimis Tests, and a business only needs to pass one test to be fully taxable and claim all of its input tax.

As another important issue, you might be thinking that we should ignore Janet’s property activity as far as her VAT registration is concerned on the basis that it is not a business venture. However, property income (or land income to be more precise) is always classed as a business activity (or ‘economic activity’ to the use the phrase in the EU VAT Directive) – there is no such thing as non-business property income. The motive of Janet’s arrangement might be to provide capital growth and income for her future ‘pension pot’ but it is still a ‘business’ activity as far as the nation’s favourite tax is concerned.

The planning opportunity

A key point with partial exemption is that when we apply the de minimis test(s) on each quarterly or monthly VAT return, the figures are always provisional and are superseded by an annual adjustment calculation. The annual adjustment covers the 12-month period to 31 March, 30 April or 31 May, depending on the VAT periods of the business. For a business on monthly returns (usually repayment traders such as farmers or exporters), the relevant date is 31 March. So the main challenge (using the ‘original test’ as our favoured test) is to ensure that our annual exempt input tax is less than £7,500 and not be too concerned if the figure goes over £1,875 on some of our quarterly returns within the year, i.e. when we will be partly exempt and suffer an input tax restriction.

So here is the key question: How can Janet claim exempt input tax of £12,000 when the maximum annual figure within the de minimis tests is £7,500? The answer is that she must ensure that the builder provides his services and invoices (for completed work) over two partial exemption tax years. So if £6,000 exempt input tax is incurred in the partial exemption tax year to, say 31 May 2016, this will hopefully mean that total exempt input tax is less than £7,500 (£625 per month x 12 months) when a bit of extra exempt input tax is added on for overhead costs (residual input tax not claimed), and the same process will be carried out again for the year ended 31 May 2017. And hopefully the 50% total input tax calculation (the second part of the ‘original test’ which must also be met) will not be a problem in either year because Janet will incur a lot of input tax (taxable) on her computer activities.

Timing of input tax claim

Here is another twist to the tale: although Janet will almost certainly incur the second £6,000 of input tax on builder services in the early part of the 2016/17 partial exemption tax year (say August 2016 VAT quarter), she will not actually claim it until after the year ended 31 May 2017 when she carries out her annual adjustment calculation. This is because £6,000 of exempt input tax will obviously exceed the quarterly figure of £1,875 (£625 per month x 3 months) so she will be partly exempt in the August quarter and suffer an input tax block. But when the annual calculation is carried out at the end of May 2017, that process should produce a happy ending because £6,000 is less than £7,500 and she will reclaim the full amount as part of her annual adjustment process. As the old saying goes……it’s all about the year-end results!

Note – a taxpayer has a choice of either including the VAT payable or repayable following the annual adjustment calculation on the return at the end of the partial exemption tax year or the following period. So if Janet is due a rebate when the calculation has been carried out (as will be the case in May 2017), it makes sense for her to include the VAT repayable by HMRC on her May rather than August return. (HMRC VAT Notice 706, para 12.6).

The bad news: flat rate scheme

Some readers might be wondering if the use of the de minimis rules to claim input tax on exempt buy-to-let property costs is playing the game of cricket with a straight bat. If you think this is the case, then consider the implications for Janet if she was using the flat rate scheme (FRS). To cut to the chase, HMRC would expect her flat rate percentage to be applied to the exempt rental income from her property as well as her taxable sales. So Janet would lose a proportion of her rent in FRS tax, even though she is obviously not charging VAT to her tenant.

As a final comment, I have focused on the situation where the secondary exempt activity relates to residential property lettings but the partial exemption de minimis rules can provide winning outcomes and VAT savings in many other trading situations. As a panellist on the TV show Dragons’ Den might say...it’s all about the numbers!