EU withdrawal: a half-hearted separation?

Share this article

Jeremy Woolf considers the continued relevance of European Union law to indirect taxes

Key Points

What is the issue?

EU law has not ceased to be of any relevance to UK indirect taxes, largely because of the European Union

(Withdrawal) Act 2018, which is primarily responsible for the continued relevance of EU law going forward.

What does it mean for me?

Although the basic philosophy of the European Union (Withdrawal) Act 2018 is to be commended, there are several features of the Act that make the snap-shot appear half-hearted and which may generate disputes going forward.

What can I take away?

One of the surprising features of many of the changes made by the EU (Withdrawal) Act 2018 is their retroactive nature. Transitional savings should generally ensure that the changes made by the Act do not impact on proceedings commenced prior to 31 December 2020 but decided after it.

The transitional period under the Withdrawal Agreement between the United Kingdom and the European Union has now expired. Apart from Northern Ireland, where there are ongoing obligations under the Northern Ireland Protocol to the Withdrawal Agreement, there are no ongoing treaty obligations to continue applying EU law.

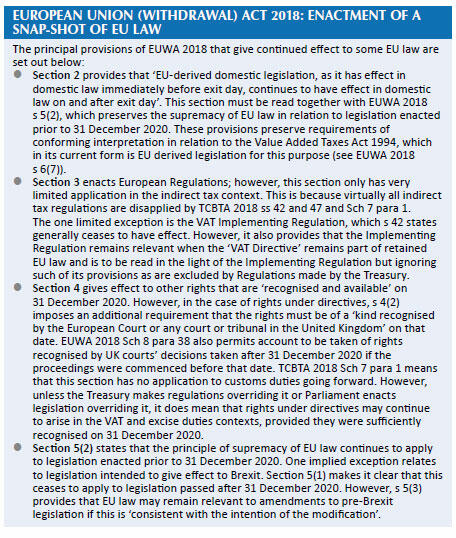

However, that does not mean that EU law has ceased to be of any relevance to indirect taxes. This is largely because of the European Union (Withdrawal) Act (EUWA) 2018. That Act was modified by the European Union (Withdrawal Agreement) Act 2020, which gives legal effect to the Withdrawal Agreement. Despite its name, EUWA 2018 sought to enact a ‘snap-shot’ of EU law and is therefore primarily responsible for the continued relevance of EU law going forward (see box opposite). However, particularly with customs duties and excise duties and to a lesser extent VAT, its impact has been limited by the Taxation (Cross-border Trade) Act (TCBTA) 2018.

A half-hearted snap-shot of EU law

Although the basic philosophy of EUWA 2018 is to be commended, there are several features of the Act that make the snap-shot appear half-hearted and which may generate disputes going forward.

1. Recognition of rights

EUWA 2018 includes the requirement that directives only confer rights if they are of a ‘kind recognised by the European Court or any court or tribunal in the United Kingdom’ on 31 December 2020. This in turn raises questions about how specific the recognition needs to be before a right is recognised. Paragraphs 96-97 of the explanatory notes to EUWA 2018 suggest that the recognition needs to be fairly specific. However, it is not entirely clear from the wording that this is correct. Especially if the loss is retroactive, it does not appear satisfactory that rights should be lost just because of the absence of a more specific decision when, in practice, there can be no serious dispute about the fact that the provisions would previously have had direct effect.

2. Charter of Fundamental Rights

The Charter of Fundamental Rights is not incorporated (see EUWA 2018 s 5(4)). Despite this, however, s 5(5) provides that the underlying general principles may remain relevant. This exclusion may cause some uncertainty about the status of any decisions that have placed reliance on the Charter of Fundamental Rights.

3. Incompatibility with general principles of EU law

There is ‘no right of action in domestic law on or after [31 December 2020] based on a failure to comply with any of the general principles of EU law’. Also, the courts cannot ‘disapply or quash any enactment or other rule of law’ or ‘quash any conduct’ on the basis that it is ‘incompatible with any general principles of EU law’ (see EUWA 2018 Sch 1 para 3).

This paragraph raises several issues:

- What is a ‘general principle of EU law’? It is reasonable to infer that it is not intended to apply to issues such as the direct effect of provisions of directives, which are specifically dealt with elsewhere in the Act. It clearly does apply to general principles, such as proportionality, abuse and equal treatment, that otherwise run through EU law. Reflecting the ‘snap-shot’ approach of the legislation, EUWA 2018 Sch 1 para 2 states that general principles are only retained if recognised by the Court of Justice on 31 December 2020, although that recognition need not be in an essential part of the decision.

- What may be more open to question is whether this extends to directive specific principles, because it may be argued that they are not sufficiently ‘general’ to be ‘general principles’. Examples may be the principle of neutrality in VAT, at least when it relates to rights to deduct input tax and therefore differs from the principle of equality. Another example may be the Kittel principle, restricting rights to deduct input tax when a person ought to have been aware of a fraud, insofar as it is wider than the principle of abuse, which is clearly a more general principle.

- If these principles are not ‘general principles’, then Sch 1 para 3 will presumably have no impact on their continued relevance. TCBTA 2018 s 42(4) explicitly states that the abuse principle and the Kittel principle continue to apply in accordance with EUWA 2018. However, since s 42(4) only applies ‘in accordance with’ the EUWA 2018, on its literal wording, it does not appear to add anything to the EUWA 2018.

- Although Sch 1 para 3 states that it is no longer possible to mount challenges to the validity of decisions and legislation relying on the general principles of EU law, it is also clear that the general principles are intended to have some continued relevance. EUWA 2018 s 6(3) provides that ‘any question as to the validity, meaning or effect of any retained EU law is to be decided … in accordance with any retained general principles of EU law’. Paragraph 210 of the Explanatory Notes states that this means that the courts are required to interpret retained EU law in accordance with the retained general principles.

While it is therefore clear that the general principles are intended to have some effect, how EUWA 2018 s 6(3) and Sch 1 para 3 are intended to interrelate is not entirely clear. It would appear that para 3 is intended to prevent freestanding challenges to legislation and decisions. However, it is possible that when the principles impact on the correct construction of the directive, then the directive when read with general principles may continue to have direct effect, so that the general principles may continue to have an impact on the validity of UK legislation for that reason.

If this is correct, it may continue to be possible to rely on decisions such as J P Morgan Fleming Claverhouse Investment Trust v HMRC (Case C-363/05), in which the Court of Justice considered that principles of neutrality meant that the fund management exemption in the Principal Directive art 135 1(g) applied to closed funds. That article gave member states a discretion to decide what funds were eligible for exemption. However, they were required to exercise that discretion in accordance with the principle of neutrality and could not seek to exclude closed funds for that reason.

However, there may be other cases where it may be more difficult for a party to rely on general principles going forward. One ironic example may be provided by the Supreme Court’s decision in Pendragon v HMRC [2015] UKSC 37. That case related to the Cars Order. The Supreme Court accepted that the Order was not giving effect to any specific provision of the Principal Directive. However, the court considered that it was still open to HMRC to rely on the principle of abuse because the entire VAT code was giving effect to the Directive. It is therefore difficult to see why this should not be considered a freestanding challenge to the domestic provisions relying on general principles that is precluded by EUWA 2018 Sch 1 para 3. The recognition to the abuse principle in TCBTA 2018 s 42 probably does not impact on the position because the section just states that the principle has effect in accordance with EUWA 2018, and on its literal wording therefore adds nothing to that Act.

Another possible example is provided by attempts to challenge penalty provisions on the basis that they are disproportionate (see, for example, HMRC v Trinity Mirror [2015] UKUT 421). In these cases, decisions are being made against the backdrop of the Principal Directive including article 273, which confers a wide discretion to take measures to implement the Directive. There is therefore possibly a slightly stronger case for considering that there is a relevant directive provision requiring interpretation for that reason. However, if a proportionality challenge does remain possible in these circumstances for that reason, then EUWA 2018 Sch 1 para 3 will clearly have only a very limited application in practice.

4. Power to depart from Court of Justice decisions

EUWA 2018 s 6(4)– 6(5D) gives the Supreme Court and the High Court of the Justiciary and, if authorised by regulations, other courts, power to depart from decisions of the Court of Justice. Section 6(5) states that the Supreme Court and the High Court of the Justiciary are only to do so on grounds on which they depart from their own decisions. In the case of the Supreme Court, these are set out in a Practice Statement of 1968.

There was a consultation over the summer about which, if any, other courts should have the relevant power. It is possible that these provisions could result in attempts to relitigate the correctness of Court of Justice decisions. At least in relation to issues outside the transitional period, future decisions of the Court of Justice are just of persuasive significance (see EUWA 2018 s 6(1)-(2)). No references can be made after 31 December 2020 (see EUWA 2018 s 6(1)).

5. The Principle Directive

TCBTA 2018 s 42 just provides for the Implementing Regulations to remain relevant when the Principal Directive remains part of retained EU law. Section 4 arguably adopts a fairly restrictive approach to giving effect to rights under the Directive for the reasons explained above in 1. Recognition of rights.

However, the Principal Directive probably remains relevant in a wider number of situations because of obligations of conforming interpretation, so the Principal Directive should hopefully remain part of retained EU law in a wider range of circumstances for that reason. If this is not considered to be the position, it is unfortunate that s 42 does not also make any specific reference to the Implementing Regulation continuing to be relevant to the interpretation of UK VAT legislation when it was previously relevant to its interpretation.

Transitional issues

One of the surprising features of many of the changes made by EUWA 2018 is their retroactive nature. Transitional savings should generally ensure that the changes made by the Act do not impact on proceedings commenced prior to

31 December 2020 but decided after it (see EUWA 2018 Sch 8 paras 38 and 39(3)). However, the same is only true to a more limited extent to proceedings commenced after 31 December 2020 but related to issues that arose on or prior to that date. There is an explicit two year window for bringing claims for Francovich damages, which are otherwise abolished (see EUWA 2018 Sch 8 para 39(7). There is also an explicit three year window for bringing claims for breach of the general principle of EU law.

However, such proceedings cannot seek the disapplication of an Act of Parliament or other rule of law of any other enactment that could not have been made differently (see EUWA 2018 Sch 8 para 39(5)).

The retroactive nature of the changes is also almost certainly inconsistent with articles 4 and 86 of the Withdrawal Agreement. Article 4 states that the agreement and the treaty rights conferred by it shall have the same legal effect as if the UK were a member state and also requires inconsistent legislation to be disregarded. Article 86 gives the Court of Justice jurisdiction against the UK in proceedings commenced in the court within the transitional period or referred during that period.

The European Union (Withdrawal Agreement) Act 2020 s 7A gives effect to such provisions except those relating to Part 4, which relate to the transitional period insofar as effect is given to them under the European Communities Act 1972 s 2(1). However, neither Articles 4 nor 86 of the Agreement are in Part 4, so legal effect is probably given to them by EUWA 2018 s 7A as amended. There may also be arguments that the apparent retroactive nature of the legislation is contrary to the European Convention of Human Rights. Unless the law is reviewed by the Supreme Court, decisions such as R (oao Zeeman) v HMRC [2020] EWHC 794 suggest this may only be the position when the legal position was fairly clearly established at the end of the transitional period.