The farmer’s wife: the impact of relationship status

Share this article

Farming families must rethink succession, relationships and legal protections to avoid unexpected inheritance tax shocks.

Key Points

What is the issue?

New rules from April 2026 will cap agricultural and business property relief at £2.5 million (with possible £2.5 million from the spouse) before dropping to 50%, making the surviving spouse exemption and formal relationship status central to farm succession planning.

What does it mean to me?

These changes place far greater tax pressure on farming families, particularly unmarried partners who lack the protections afforded to spouses.

What can I take away?

Farms must now reassess ownership structures, relationship status and legal agreements to secure reliefs that previously applied more generously. Without proactive arrangements – such as cohabitation, nuptial or updated partnership agreements – families risk substantial inheritance tax liabilities and potential disruption to the business.

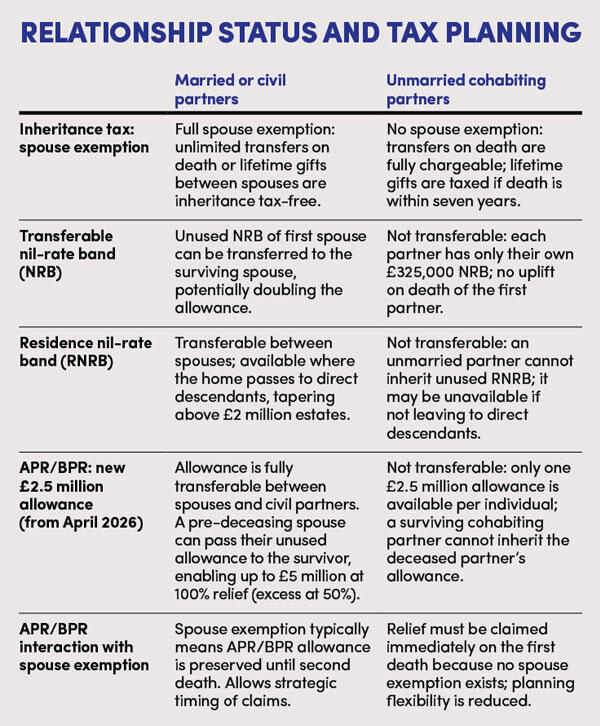

Just before Christmas, the government announced that, with effect from 6 April 2026, agricultural property relief (APR) and business property relief (BPR) would be capped – referred to in the draft legislation as an ‘allowance’ – at £2.5 million (increased from £1 million) and thereafter provided at 50%. The chancellor had previously confirmed in the 26 November 2025 Budget that this allowance will be transferable between spouses and civil partners, including where a spouse or partner dies before 6 April 2026.

This big tax news ties into the increased relevance of the surviving spouse exemption for inheritance tax, which from 30 October 2024 became significantly more important for farming families as they plan to maximise inheritance tax relief moving forward.

Now that the draft legislation has been published, the surviving spouse exemption is under the spotlight, as are the implications for unmarried partners on the family farm. Both factors must be considered in all farm succession planning, as must valuations. The tension between personal choice and legal protection can make these decisions considerably more complex. In particular, the legal status of a farming ‘partner’ (in the romantic sense) becomes a more central issue in capital tax planning.

The legal considerations of cohabitations

Despite the misleading myth of a ‘common law marriage’, UK law does not grant unmarried couples the same legal protections as married partners. This misunderstanding can result in serious legal and financial consequences if a relationship breaks down, especially where the family farm is involved. It is therefore essential that all family members and partners should seek advice on their specific position.

Marriage can therefore provide legal clarity and stronger inheritance tax protection, both through the surviving spouse exemption and the transferable £2.5 million allowance. For some long-term cohabiting couples, formalising the relationship through marriage or civil partnership may reduce the inheritance tax liability that will arise on the death of the farm owner and possibly prevent the need to sell or reduce the size of the farm to meet the inheritance tax bill, although matters are strongly improved by the increase to £2.5 million.

Open conversations with unmarried partners – whether before moving in together or once already cohabiting – can help to clarify expectations. However, informal arrangements offer limited rights in legal terms and, given the new inheritance tax implications, these issues now need to be addressed directly. Every farming business has to be assessed on a case-by-case basis. When the allowance was only £1 million, a large amount of lifetime gifting was undertaken and that has to be incorporated into the current planning.

Cohabitation agreements

A cohabitation agreement is a legally binding document that outlines what should happen if the relationship ends. For farming families, such an agreement can be particularly valuable in giving other farming business partners confidence with regard to the protection of assets. Key benefits include:

- providing clarity regarding ownership of the farmhouse, farmland and farming assets;

- setting out financial arrangements, including each partner’s contributions to the business;

- recording how each partner participates in the business – the work they do, how they are paid and their responsibilities;

- specifying how business or personal assets should be divided if the relationship breaks down; and

- addressing inheritance issues in the event that one partner dies.

It is on the death of the farmer after April 2026 – when they are the holder of relevant assets – that the new problem of the 50% APR and BPR structure is triggered above the £2.5 million. It is therefore likely that some cohabitation agreements within farming families will evolve into nuptial agreements, whether pre or post marriage. What is clear is the considerable benefit that the surviving spouse exemption and the transferable £2.5 million allowance at 100% provide for APR and BPR planning.

Cohabitation v marriage

The legal differences between marriage and cohabitation are substantial. Married couples benefit from a comprehensive framework that provides certainty over property, inheritance, tax and financial support. Cohabiting partners, by contrast, have very limited protections, regardless of how long they have lived together or how intertwined their financial lives have become.

One of the most important distinctions concerns property. Married couples fall within a system that allows the court to redistribute assets on divorce according to fairness, taking into account both partners’ needs and contributions – financial and non-financial. Homes, savings, pensions and business assets can all be shared. Unmarried couples, however, have no such safety net. Ownership depends strictly on title and any provable financial contributions. If a home is legally owned by one partner, the other may have no claim at all unless they can show evidence of a shared intention or contribution, which can be extremely difficult.

Inheritance and tax rules create even sharper contrasts. Spouses inherit automatically under intestacy rules, and transfers between them are fully exempt from inheritance tax. They also benefit from transferable allowances, including the nil-rate band, residence nil-rate band and, from 2026, the full £2.5 million APR/BPR allowance. Cohabiting partners receive none of these protections. Without a legal will, they may inherit nothing (subject to a claim for reasonable financial provision under the Inheritance (Provision for Family and Dependants) Act 1975). Any transfer of assets is potentially taxable. This can result in significant financial exposure, particularly where a family home or a business is involved.

These differences illustrate why financial legal and tax planning is essential for unmarried couples. Without proactive arrangements – such as cohabitation agreements, wills and clear ownership structures – they face significant financial vulnerability that must be part of farm succession planning.

Pre and post nuptial agreements

The main advantage of a cohabitation agreement is that it reduces the risk of disputes and helps to protect family farming assets. It provides clarity for both partners and reassures the wider family that the farm is safeguarded. If the partners later marry and become eligible for the surviving spouse exemption, their legal status will change. In that case, they should consider putting a post-nuptial agreement in place – or a pre-nuptial agreement prior to marriage – to ensure the intentions of the original cohabitation agreement continue to apply. To achieve the best outcome, farmers should seek specialist legal advice from an agricultural solicitor with family law expertise who understands the nuances of both the farm and the change to the relief including the spouse angle.

Farming partnership agreements

Historically, farms were often owned just by the father of the farming family, while the mother typically was not a farming partner but would inherit everything under the farmer’s will – on the assumption that ‘she can sort out the children’. Changing social patterns have shifted this dynamic, with fewer marriages, more cohabiting couples and far more spouses actively involved in running the farm in a more formal capacity.

For a spouse to utilise their own £2.5 million allowance for 100% APR and BPR, they must be genuinely involved in the business and able to evidence that involvement. As a result, spouses will need to be considered in a ‘fresh tax planning light’ following the Budgets of 2024 and 2025 and the latest government announcement.

To achieve tax efficiency under the reduced APR and BPR rates – dropping to 50% after the first £2.5 million from April 2026 – every farm will require full or at least updated succession planning. This demands difficult emotional and technical conversations about all members of the farming partnership and their partners, including:

- life expectancy;

- marriage suitability and the tax advantages of achieving surviving spouse exemption, potentially transitioning from cohabitation;

- valuations of the farm to calculate potential inheritance tax liabilities where the surviving spouse exemption and the £2.5 million allowance may not be enough;

- identifying weak areas of inheritance tax exposure under the 50% APR and BPR regimes; and

- creating a potential ‘hit list’ of assets that could be sold to pay the possible inheritance tax bill and developing a ‘war chest’ to support farmers through future challenges.

The increase to £2.5 million has meant that some farms are covered by the government 'U-turn' to £2.5 million and the 'hit list' and lifetime gifting that was taking place in 2025 are not so key in 2026; however, each position must be carefully re-evaluated with strong valuation.

Every farm is different: each has its own physical characteristics, its own partnership structure, its own trading activity and aspirations, and often widely differing attitudes to tax planning risk. As a result of all the Labour government changes, the role of the spouse must be fully understood. Substantial, targeted individual tax planning will be required to integrate with the broader strategy for all farm partners. The months ahead will be extremely busy for valuers, tax planners and agricultural solicitors – and perhaps even an increase in marriage celebrations as more spouses join the farming partnership.

There will also need to be predictions of future inheritance tax liabilities and consideration of practical tax planning options on death. As mentioned, the ‘hit list’ of assets to sell will be high on the list of priorities as appropriate, with careful attention paid to any capital gains tax consequences. However, after a turbulent 2024 and 2025, farmers and their advisers must be prepared to act swiftly. With the prospect of a ‘mansions tax’ on the horizon, downsizing the main farmhouse may become part of tax planning discussions, especially with principal private residence relief for capital gains tax. That topic will be explored in future articles, as the practical implications evolve.

© Getty images