Freezing the threshold

Share this article

Neil Warren considers practical issues about the Budget announcement that the registration threshold will be frozen until at least April 2020

Key Points

What is the issue?

Many business owners were relieved that the Chancellor decided not to reduce the VAT registration threshold in his recent Budget. It will be frozen at the current figure of £85,000 until at least April 2020. But this decision could create hidden problems for thousands of UK businesses that trade close to the threshold.

What does it mean to me?

It might be worth discussing registration issues with clients that are trading close to the threshold, where an inflationary price increase next year could send them over the limit and create a VAT problem.

What can I take away?

VAT registration is not good news for a business with standard rated sales and very little input tax to claim and which sells goods or services to customers who cannot claim input tax. There might be scope to review trading structures to avoid a potential problem, which are considered in the article.

There was great excitement before Budget day that the Chancellor intended to slash the VAT registration threshold from £85,000 to £26,000. This speculation followed the publication of the OTS VAT report which identified that a large quantity of businesses were trading just below the threshold and that the £85,000 limit was a disincentive to trading growth. However, the speculation was unjustified, and the final announcement was that the £85,000 threshold would be frozen until at least April 2020. You might think that this policy is not very exciting but I personally think the issues are much wider than you might imagine.

Trip to the seaside

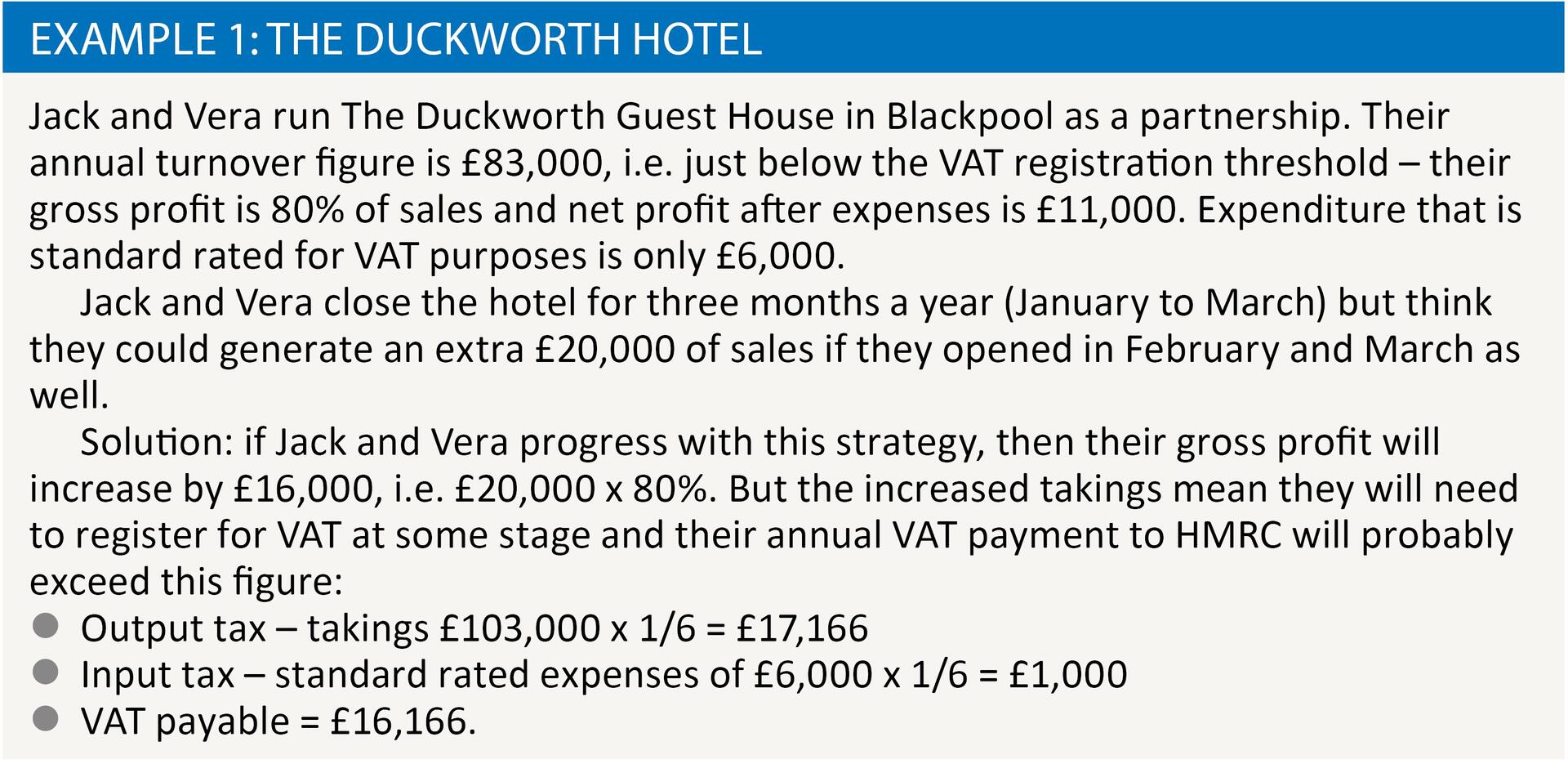

Let me take you to Blackpool, a fun packed resort that is very popular with holiday makers of all ages and a place that is packed with history dating back to Victorian times. There are 1,600 guest houses in Blackpool, as well as a lot of small businesses such as ice cream kiosks, cafes, bars, gift shops and tattoo parlours. My guess is that most of these businesses will not be VAT registered and are part of the ‘cliff edge’ problem identified by the OTS, i.e. many businesses are better off trading just below the VAT threshold if their income is mainly standard rated and they have very little input tax to claim and they also have customers who cannot claim input tax, i.e. the general public. See example 1.

Price increase?

We are hopefully all agreed that Jack and Vera will not be extending their opening hours because of the potential VAT problem but what will happen in March when they want to increase their prices for the new summer season? An inflationary increase of 3% would lead to anticipated turnover of £85,490 in the following 12 months, which is now above the VAT threshold because of the Budget announcement that it would remain at £85,000. So they might decide to freeze their prices for the year or restrict the increase to 1% or 2% but they will then have the same issue in April 2019 – and possibly April 2020. My personal view is that the VAT registration threshold will probably be frozen at £85,000 for many years to come – 2020, 2021, 2022 etc. There are numerous examples of thresholds being frozen in the VAT world – for example, the annual joining threshold of £150,000 for the flat rate scheme has not been increased since April 2003! It is very hard to reduce the threshold by a significant amount because this would capture thousands of businesses and potentially convert them into a loss making position. If we were starting with a blank sheet of paper and inventing VAT as a new UK tax, rather than one that is 44 years old, then it would be a different ball game. A classic example of this is the self-employed personal trainer I use at my gym, who I estimate has annual income of about £40,000 and his only significant input tax would be about £800 on the trading fee he pays to the gym owners. So his net profit would fall by nearly £6,000 if he had to register for VAT and it would be very difficult for him to raise prices to his customers in a very competitive market. I know he has a big mortgage on his Manchester apartment so a big VAT hit would be very unwelcome!

Alternative strategies

This is where I think the VAT issues will become very interesting: Jack and Vera will be faced with increases in their costs each year but we have identified how difficult it will be for them to increase prices on their sales when the VAT threshold is frozen for two or three years. And there are many thousands of businesses in the same position as Jack and Vera. I used to act for an architect who deliberately controlled his work level to avoid exceeding the VAT threshold in any rolling 12-month period. So I suspect that clients will start thinking about how they can have their cake and eat it, i.e. increase their selling prices but still avoid a VAT problem.

Income splitting

The reason I have chosen the Blackpool guest house theme for this article is because I was talking to a guest house owner at a football match a while ago, who told me (with great pride) that the way he avoided a VAT registration problem was by splitting his charge to guests between his own business and that of the self-employed cleaner he used to service the rooms. So he would charge a guest £30 a night for the room and breakfast and the cleaner would separately charge the guest £5. The annual total of the £30 fees is less than the VAT threshold, which would not be the case if the relevant figure was £35. As VAT enthusiasts will know, this strategy would be challenged by HMRC (almost certainly with success) because the reality is that the guest house is making all supplies to the guests, and the cleaner is working for the guest house. This outcome was reaffirmed in the case of Wendy Lane T/A Spot On (TC2909) a number of years ago. But can you see the likely permutations that might be put forward by clients affected, many of which will be non-starters? Here are a few suggestions Jack and Vera might propose:

- There is a small bar in the guest house. Would it be possible for the bar activity to be organised by Jack or Vera as a sole trader i.e. a separate legal entity to the partnership guest house? This deflects taxable sales from the partnership to another business.

- How about if guests pay a ‘room only’ fee to the partnership – and then a separate payment of, say, £6 if they wanted breakfast? The breakfast service would be organised as a separate business to the partnership – say Vera as a sole trader.

- What would be the position if Jack and Vera ask their son Terry to organise either the bar or breakfast activity as a separate business, i.e. separate characters are being introduced to part of the operation?

I have not directly answered the above questions because each trading situation is different and the circumstances needs to be thoroughly reviewed with business owners. It is also important that advisers remember the Professional Conduct in Relation to Taxation (PCRT) guidelines, and do not embark on any business splitting arrangements that are highly artificial or contrived.

Business splitting

The powers of HMRC to treat separated business as one legal entity (a partnership) are given by paras 1A(1) and 2, Schedule 1(A), VATA1994. The key challenge is for HMRC to be able to prove that the two businesses have ‘financial, economic and organisational links.’ The key word is ‘and’ i.e. all three links have to be proved rather than one or two of them. The main outcome of a direction from HMRC is that the combined businesses will need to register for VAT as a single entity moving forward, i.e. not retrospectively. But if HMRC decide there never was two separate businesses (such as in the example of the split between the room charge and the cleaning fee I gave), this will become a late registration issue. And don’t forget that HMRC have the power to go back up to 20 years to correct a late registration. For guidance about business splitting issues, see HMRC VAT Manual: VAT Single Entity and Disaggregation.

As a general tip, there is no doubt that the most precarious business splits are those that involve family members. There is not the same incentive to do things on an arm’s-length basis as there is with non-family structures e.g. for shared overheads that are recharged or goods that move from one entity to another. However, a recent First-tier Tribunal case (MG and ND Stoner (TC6193)) involved four separate trading operations in one building down in Swanage. There did not seem to be any HMRC concern about the business splitting issue (two entities were VAT registered and two were not) and the case was all about input tax claims.

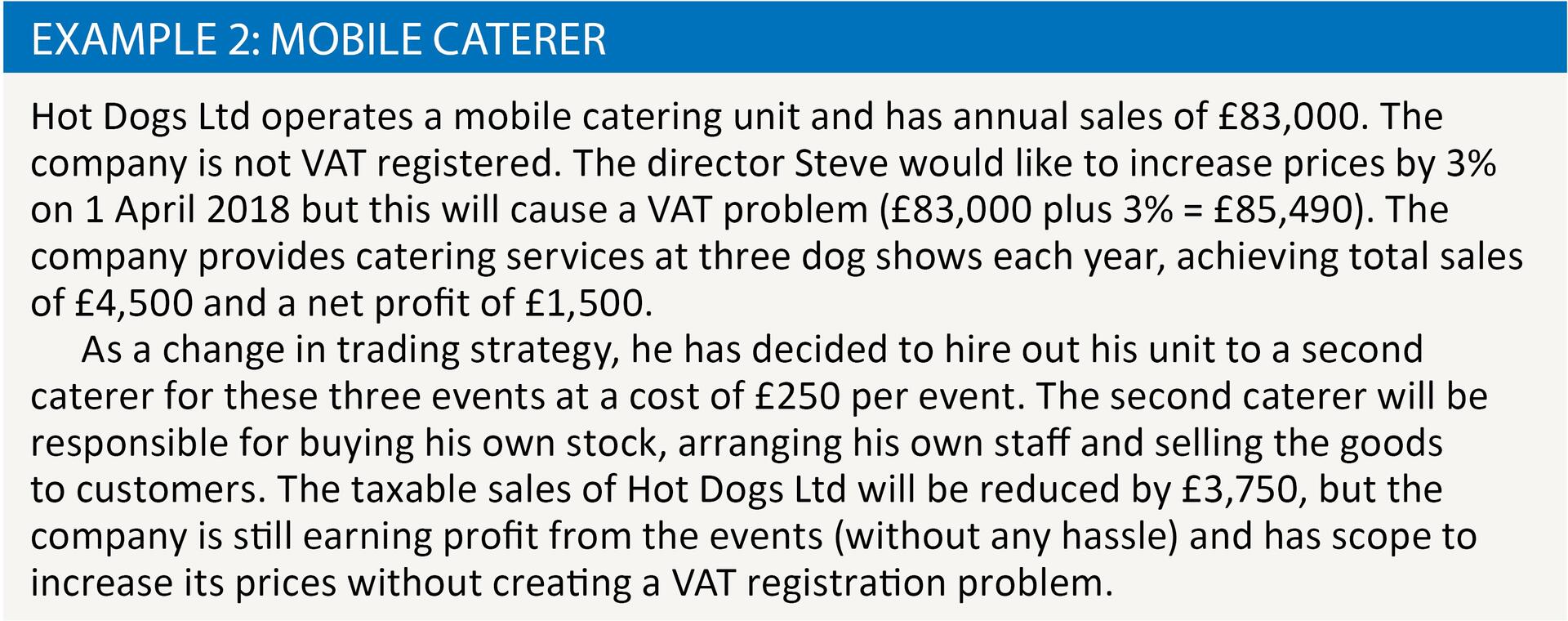

Final thought

To share an example of a commercial arrangement that would work, see example 2. A plus point with this scenario is that the second caterer is not related to the first caterer, so there is a commercial incentive to do things correctly. And there is no doubt that the second caterer is clearly selling food and drink to the punters at the shows i.e. he is responsible for any VAT issues on the takings.