Frequently asked questions

05 February 2021

Share this article

HMRC answers the most frequently asked questions on the HMRC Inheritance Tax Helpline

Has my form IHT421 been issued?

- HMRC now emails all IHT421s for grants in England and Wales directly to HM Courts and Tribunals Service. You can expect HMRC to do this within 15 working days of receiving your IHT400 or payment of the tax due on delivery of the account, whichever is later. If tax is due on the estate, HMRC will confirm that it has issued your IHT421 in writing once it has processed the account.

- If you want to check that HMRC has received your form IHT400, you should wait for at least 20 working days from the date you sent the form, before contacting HMRC.

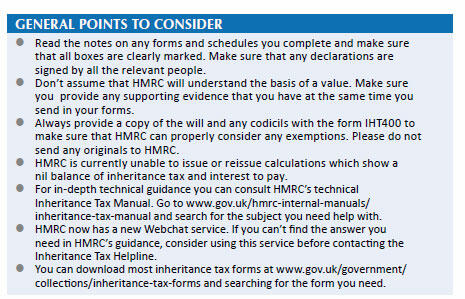

Help needed to complete the IHT400 and IHT400 schedules

- You should read the guidance notes for completing form IHT400 (see bit.ly/ 38o6R0R) and the schedules before calling the Inheritance Tax Helpline.

- For more in-depth guidance for professional agents, there is an Inheritance Tax toolkit to help you complete the form IHT400 and schedules (see bit.ly/3s1ux2P).

Telling HMRC about amendments and claiming loss on sale relief

- If there are changes to the values in an estate after you’ve submitted your form IHT400, you must tell HMRC. Use the following methods:

- { Form IHT35 ‘Claim for relief – loss on sale of shares’: to claim relief on shares sold at a loss within 12 months of the date of death.

- { Form IHT38 ‘Claim for relief – loss on sale of land’: to claim relief on land or buildings sold at a loss within four years of the date of death.

- Form C4 ‘Corrective Account’ or form C4(S) ‘Corrective inventory and account (Scotland)’: to tell HMRC about any other amendments to the estate.

You may not always pay less tax by claiming a relief, so read the guidance carefully before you make a claim.

- For copies of the forms, go to www.gov.uk/government/collections/inheritance-tax-forms.

- HMRC expects agents to work out the amount of any additional tax due as a result of amendments, and place money on account if they wish to stop or reduce interest.

Completing form IHT35 ‘Claim for loss on sale of shares’ and form IHT38 ‘Claim for relief – loss on sale of land’

- Make sure that you answer all the questions and give all the information asked for on the form.

- To avoid delays establishing whether the claim is provisional or final, make sure that the declaration is marked.

- HMRC will not be able to accept your claim unless it is signed by all the relevant people.

Completing form C4, ‘Corrective account’ or form C4(S), ‘Corrective inventory and account (Scotland)’

- Make sure that the description of any assets and the original value matches the information that you gave on the form IHT400.

- To avoid delays, don’t include amendments to property or shares sold at a loss on this form. Instead, use form IHT38 ‘Claim for relief – loss on sale of land’ or form IHT35 ‘Claim for loss on sale of shares’ to claim relief on these assets.

- Include any additional information to support an amendment with your form; e.g. a letter from an insurance company to explain why a policy is now not part of the estate. This will prevent HMRC having to request this later.

Applying for a reference number

- If there is tax to pay, you must get an Inheritance Tax reference number before sending your form IHT400 or IHT100 to HMRC. You don’t need to get a reference number if there is no tax to pay.

- You should apply for your reference at least three weeks before you submit your IHT400 or IHT100.

- To avoid delays HMRC recommends that you apply online for a reference for a form IHT400 (see bit.ly/2XcxcIC).

- To apply for a reference for a form IHT100 you will need to complete a form IHT122 (see bit.ly/2LkNuMV).

Applying for a clearance certificate

- If you wish to apply for a formal clearance certificate, you should use form IHT30 ‘Application for a clearance certificate’ to do this. Only do this when you are sure that there will be no further changes that will affect the tax position on the estate.

- Because of Covid-19, HMRC is currently unable to issue a stamped and signed copy of your form IHT30. Instead, it will issue a letter, containing a unique code, that has the same effect as a stamped and signed copy of the IHT30.

Paying by instalments

- If you have elected to pay some of the inheritance tax due by instalments, you are responsible for making sure that each instalment is paid on time.

- You can use HMRC’s online interest calculator at bit.ly/38joxL1 to calculate any interest due.

Checking receipt of payment

- HMRC is not able to send receipts for payment.

- Paying electronically is quicker, easier and more secure, and means that you can easily see what you have paid and when.

- HMRC is currently unable to accept cheques as a method of payment for inheritance tax.

- For more information on how to pay inheritance tax, go towww.gov.uk/paying-inheritance-tax.

Requesting a repayment

- HMRC is now making all repayments of inheritance tax by Faster payments. This means that you will get your repayment more quickly, once it has been processed. HMRC may need to write to ask for the bank account name, account number and sort code of the bank account you want the repayment to go to, if it doesn’t have these details.

- HMRC aims to deal with all repayments within 15 working days of receiving your form or letter. You should allow 20 working days for HMRC to process your repayment and check your bank account before contacting HMRC.

- HMRC is currently unable to issue copies of inheritance tax repayment calculations, but will usually write to advise the amount to be repaid. If you believe the amount of your repayment is incorrect, contact the Inheritance Tax Helpline on 0300 123 1072.

Image