Further extensions to support schemes

Share this article

Rachel McEleney and Natalie Backes review the extensions to the Coronavirus Job Retention Scheme and the Self-employment Income Support Scheme

Key Points

What is the issue?

The chancellor announced in his Budget that both the Coronavirus Job Retention Scheme (CJRS) and the Self-employment Income Support Scheme (SEISS) will be extended to 30 September 2021.

What does it mean for me?

Throughout the duration of CJRS, employees will continue to receive 80%of their wages (up to a monthly maximum of £2,500) for the time they are furloughed. There will be a fourth SEISS grant covering the period from 29 January to the end of April 2021, followed by a fifth grant covering May to September 2021.

What can I take away?

Although the extension of these schemes will be welcome news, many of the complexities associated with CJRS and SEISS remain. It’s important that businesses understand these and are able to assess the impact on them.

As widely expected, the chancellor announced in his Budget speech on 3 March 2021 that both the Coronavirus Job Retention Scheme (CJRS) and the Self-employment Income Support Scheme (SEISS) will be extended to 30 September 2021. This is welcome news to businesses affected by Covid-19 but, as always, the devil is in the detail. We have outlined in this article the key points on the extension of these schemes.

Coronavirus Job Retention Scheme Throughout the duration of the scheme, employees will continue to receive 80% of their wages (up to a monthly maximum of £2,500) for the time they are furloughed. In most other respects, the rules governing the CJRS remain unchanged. Employers continue to pay employer NICs and pension contributions. Employees being furloughed must agree to a change in the terms and conditions of their employment; and the furlough scheme continues to enable part-time working. Where the employee works reduced hours (compared to their ‘usual hours’, determined according to a prescribed formula), the grant available for unworked time is reduced accordingly.

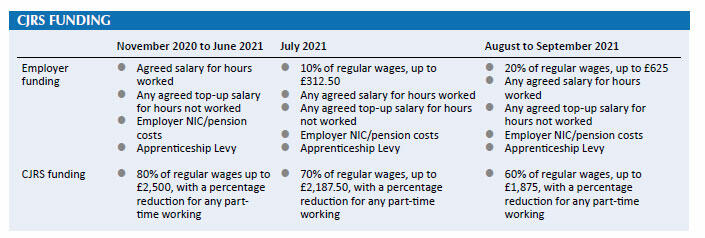

Funding levels

For claim periods up to 30 June 2021, the government will continue to pay 80% of wages up to a maximum of £2,500 monthly. For claim periods falling into July 2021, the government will pay 70% of wages up to a cap of £2,187.50 for the hours the employee is on furlough. Employers will need to make an additional contribution of 10% towards the cost of paying for unworked hours.

For claim periods in August and September, the government will pay 60% of wages up to a cap of £1,875 monthly for the hours the employee is on furlough. Employers will need to contribute 20% towards the cost of paying for unworked hours.

For claim periods up to 30 June 2021, the government will continue to pay 80% of wages up to a maximum of £2,500.

Eligibility

Under the current set of rules, which governs claim periods up to 30 April 2021, employees must have been included on a PAYE Real Time Information (RTI) submission from the employer to HMRC in the period between 20 March 2020 and 30 October 2020. Any employees made redundant after 22 September 2020 could also be re-hired and put on furlough.

For claim periods from 1 May onwards, eligibility has been extended to more recent hires. Employees must have been on an RTI submission between

20 March 2020 and 2 March 2021 to qualify. HMRC has not yet announced whether there will be another extension of eligibility to re-hired staff who have previously been made redundant.

Complexities

Many of the complexities of making claims under CJRS will continue under the extension of the scheme. These include:

- Determining the ‘reference salary’: CJRS grant claims are based on a percentage of the reference salary. There are very detailed rules as to how to determine an employee’s reference salary, depending on whether their pay is fixed or variable. For variably paid employees, the determination involves a comparison of the amounts earned in 2019/20 and the earnings in the same calendar period in either 2019 or 2020, depending on the month involved. Getting these calculations right requires a great deal of expertise and care.

- Determining ‘usual hours’: A similar set of rules with equal complexity determines an employee’s usual hours. Because of the level of detail required, employers may not have sufficiently good records to determine the hours an employee worked in a previous year.

- Unusual results: Whilst the rules normally result in a grant claim in line with expectations, there are circumstances where the correct treatment can seem counter-intuitive. For example, a fixed pay/fixed hours employee who has started to work part time (for reasons unrelated to CJRS) since March 2020 could be entitled to receive more income if they are furloughed than if they were working. Simply paying a furloughed employee less than the strict rules suggest is not advisable, since this could invalidate any CJRS grant claim made in relation to the employee. Employers should consult with HMRC or their advisers in such situations.

Self-employment income support scheme

There will be a fourth SEISS grant covering the period from 29 January to the end of April 2021, followed by a fifth grant covering May to September 2021. In order to be eligible for either of the grants, the individual’s 2019/20 tax return must have been filed by midnight on 2 March 2021.

For eligible individuals, the fourth grant is equivalent to 80% of three months’ average profits, capped at £7,500. The fifth grant will work in a similar way, but the amount of the grant will depend on the extent to which turnover has been affected. Those whose turnover has dropped by 30% or more should be entitled to the full 80% subject to the £7,500 cap. If the drop is smaller, the grant is at 30% with a cap of £2,850.

As highlighted in the chancellor’s speech, about 600,000 individuals who were ineligible for the first three grants are expected to be eligible for the fourth and fifth grants.

How the new grants differ from the first three

The eligibility rules for the fourth grant are intended to be broadly the same as those for the third, with the exception of the years that are considered for the income criteria for eligibility and the calculation of average profits.

For the first three grants, the income criteria were based on 2018/19 profits and non-trading income of that year, or average profits and average non-trading income over the three years to 2018/19. Either 2018/19 profits or average profits had to be £50,000 or less, but greater than or equal to non-trading income over the same period. Average profits were normally based on the results for 2016/17, 2017/18 and 2018/19 but this could vary, depending on when trading commenced and whether the individual was subject to special rules for parental leave or military reservists.

For the fourth grant, the income criteria are based on either 2019/20 profits and non-trading income, or average profits and non-trading income for the four years to 2019/20. Although the guidance is not explicit, it is expected that the grant will be based on the four-year average where the individual meets the income criteria for either 2019/20 alone or on average.

The detailed rules for the fifth grant have not yet been published, but it is expected that the average profits will be determined in the same way as they are for the fourth grant. Whether the changes are beneficial will depend on the individual’s circumstances. Some examples that illustrate this are set out below:

- Individuals who became self-employed in 2019/20 were not eligible for the previous grants, so they now have the potential to qualify for the fourth and fifth grants.

- Some individuals who became self-employed in 2018/19 were also unable to apply for the previous grants due to the requirement to have trading profits in that year and for them to be greater than or equal to non-trading income. If they were employed at the start of the tax year and self-employed at the end, but their employment income exceeded their trading profits, they would not have been eligible.

- Individuals whose trading profits for 2019/20 were higher than the average profits for the preceding three tax years could be entitled to higher grants than before in some cases. This could include some new parents who were eligible for the earlier grants based on the original criteria, but whose average profits had been reduced by a period of parental leave. The parental leave will still have an impact, but the extra year of profits could dilute the effect.

- In some cases, having lower profits in 2019/20 than previous years could make someone who was ineligible for the first three grants eligible for the fourth and fifth grants. For example, if the individual’s 2018/19 profits and three-year average both exceeded £50,000, they would have been ineligible for the first three grants. Having 2019/20 profits of £50,000 or less could allow them to meet the income criteria.

- Any individuals who failed to file their 2019/20 tax returns by midnight on 2 March 2021 will be ineligible for the fourth and fifth grants. Some individuals who meet all other criteria and who qualified for the first three grants could therefore find they are not eligible if they are behind on their paperwork.

- Those who were eligible for the first three grants and whose average profits over the four years to 2019/20 are lower than the three years to 2018/19 will be entitled to lower grants than before.

The government will be investing heavily in combatting fraud and error arsing from the Covid-19 support schemes.

- As noted above, those who don’t meet either set of income criteria are not eligible for grants. The population affected for the fourth and fifth grant may differ from the first three, however, as the criteria are based on different tax years. Some of those who qualified for the first three grants could find that they are ineligible for the fourth and fifth grants if both their 2019/20 and four-year average profits exceed £50,000.

- The turnover test for the fifth grant seems set to create a cliff edge. The average amount paid as a third grant, which was based on 80% of profits, was £2,800. An individual who remains eligible for the scheme and whose average profits do not fluctuate should therefore expect to receive £2,800 as a fifth grant if their turnover reduces by 30%. If it only reduces by 29%, the grant would only be £1,050 (a £1,750 drop).

Enforcement: CJRS and SEISS

The government has also announced that it will invest heavily in combatting fraud and error arising from the Covid-19 support schemes. £100 million is being set aside for a new HMRC ‘Taxpayer Protection Taskforce’ of 1,265 staff, mainly dedicated to CJRS and SEISS.

HMRC has already started a large number of probes into CJRS claims. Whilst the new Taskforce places the biggest emphasis on addressing fraud, HMRC will also expect employers to rectify any significant mistakes. Employers should be prepared to explain the basis of their claims and be able to show that HMRC guidance was followed when making claim calculations. HMRC is encouraging employers to undertake a self-review and is facilitating repayments from employers who find that they have inadvertently overclaimed.

Mistakes on calculations may be less of an issue for SEISS, as the grants are based on tax return data that HMRC already has. The main area for enquiry is whether the individual meets the other eligibility criteria, such as the requirement for the trade to be continuing and for it to have been adversely affected by Covid-19. HMRC has already written to some taxpayers who are thought to have ceased trading, and further compliance activity after the 2020/21 tax returns are filed should be expected.

Conclusion

Although the extension of these schemes will be welcome news to many businesses, particularly the newly self-employed, many of the complexities associated with CJRS and SEISS remain. It’s important that businesses understand these and are able to assess the impact on them.