Get ready for Deddf Treth Trafodiadau Tir

Share this article

Ginny Offord provides an overview of the introduction and implications of the Deddf Treth Trafodiadau Tir, or land transaction tax in Wales

Key Points

What is the issue?

From 1 April 2018 stamp duty land tax will be abolished in Wales and replaced with a new devolved tax – land transaction tax – the first tax introduced by a Welsh Government in almost 800 years.

What does it mean to me?

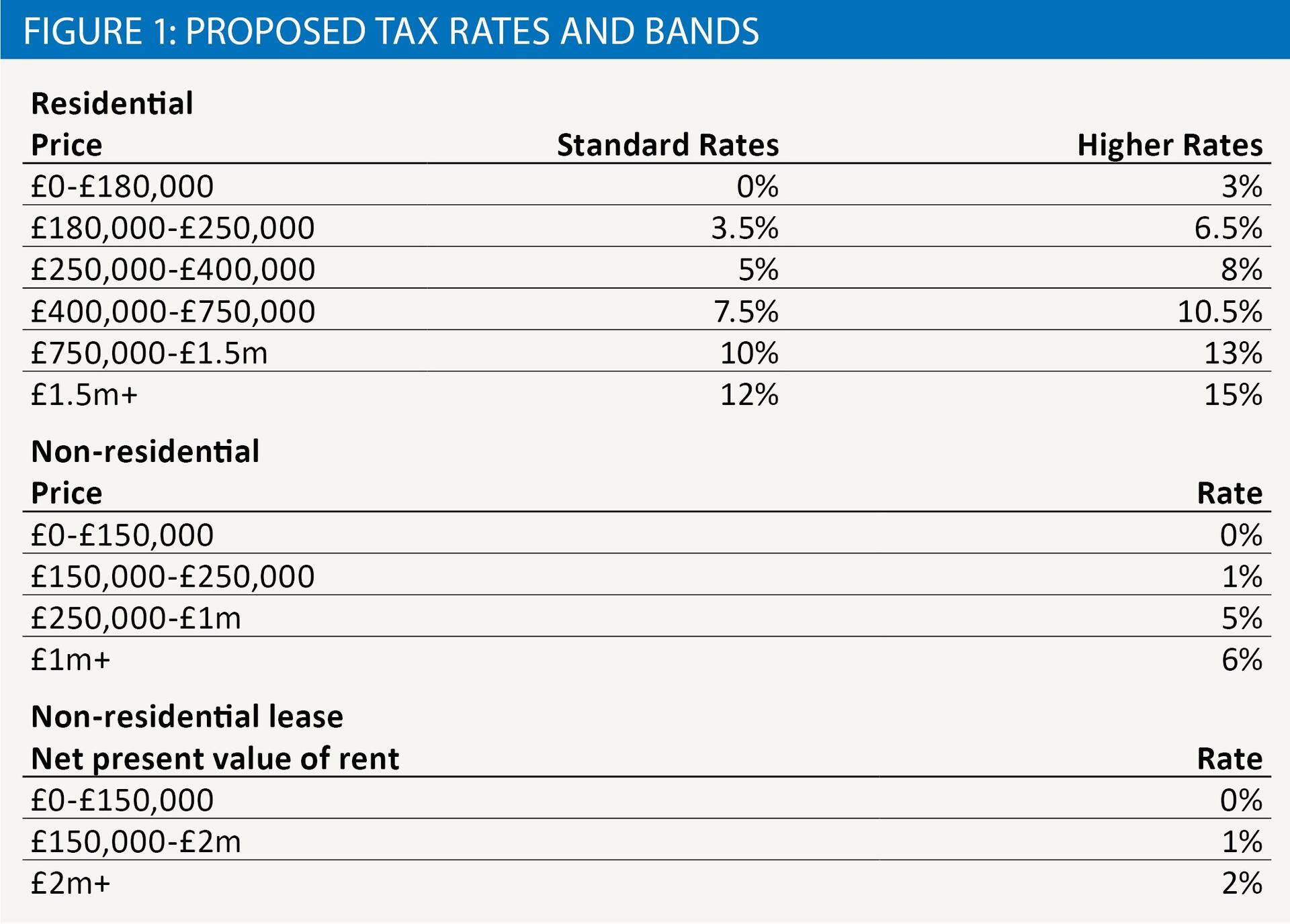

While broadly similar to SDLT the tax has some key differences, such as the tax bands and rates. Higher value residential and commercial land transactions are likely to be more expensive in Wales than they currently are in England and Northern Ireland.

What can I take away?

Those that regularly advise on, or enter into, land transactions in Wales should start considering how the new regime will affect them.

Following the Wales Act 2014, the Land Transaction Tax and Anti-Avoidance of Devolved Taxes (Wales) Act 2017 received Royal Assent in May 2017. It joins the Tax Collection and Management (Wales) Act 2016, which makes provision for the administration and enforcement of land transaction tax (LTT), and a new tax authority, the Welsh Revenue Authority (WRA).

The proposed rates and bands were announced on 3 October 2017 at the Welsh Budget, though the residential rates were amended on 12 December 2017 following the announcement of first-time buyers relief for SDLT at the Autumn Budget. The rates and bands set out below will be in the final Budget Regulations to be laid before the National Assembly in January 2018.

Rates

LTT will be a progressive tax, like stamp duty land tax (SDLT) and the Scottish devolved tax, land and buildings transaction tax (LBTT). The applicable tax rate will apply to so much of the consideration as falls within each band.

The proposed tax rates and bands are as shown in figure 1.

Costing comparisons

When announcing the rates the Welsh Government highlighted the requirement for a smooth transition between SDLT and LTT, which has been achieved by keeping the rates broadly similar to those under SDLT.

Following the announcement of first time buyers relief for SDLT at the Autumn Budget, while no parallel relief is expected to be introduced for LTT, the residential rates as first announced on 3 October 2017 were amended to increase the nil rate band from £150,000 to £180,000, with the intention of removing 80% of Welsh first-time buyers from the scope of LTT, the same percentage of first-time buyers in England and Northern Ireland who are expected to benefit from first-time buyers relief. Increasing the nil rate threshold has the added benefit of applying to all residential transactions that fall under £180,000 (except higher rates transactions), and not just first-time purchases, which is likely to be of benefit to far more Welsh homebuyers than the introduction of a first-time buyer relief.

The increase in the nil-rate threshold has been offset by a slight increase in rates for higher value purchases.

The 3% higher residential rates which apply to the purchase of second homes and buy-to-let properties under SDLT will continue under LTT with some modifications (see below). For non-residential property, a new top rate band of 6% has been introduced for properties valued over £1 million which will generally make the purchase of commercial property in Wales more expensive than the purchase of such property in England.

Look at the following examples:

- The purchase of an individual’s first home for £180,000 in England or Wales, following the introduction of first-time buyers relief in the Autumn Budget, would result in no charge to either SDLT or LTT. If instead the purchase was a replacement of an individual’s main dwelling, there would still be no tax to pay under LTT as this would fall within the nil rate threshold, but the amount of SDLT payable would increase to £1,100 as first-time buyers relief would not be available.

- The purchase of an individual’s only residential property for £2,000,000 in England would result in a charge to SDLT of £153,750. The same purchase in Wales would result in a charge to LTT of £171,200.

- The purchase of a warehouse in England for £1,750,000 would result in a charge to SDLT of £77,000. The same purchase in Wales would result in a charge to LTT of £83,500.

Main differences

When drafting the LTT legislation, it was a policy objective for the Welsh Government that any changes from SDLT would only be made to simplify the tax, make it more efficient and fair in its application, or focus on Welsh needs. Accordingly, there are many similarities between the two regimes and (so far) only a few key examples of where the LTT rules are significantly different. Those differences are as follows:

Anti-avoidance

There is an overarching ‘General Anti-avoidance Rule’. Like the Scottish equivalent, this is intended to be broader than the General Anti-abuse Rule that applies in the rest of the UK. It enables WRA to counteract ‘artificial tax avoidance arrangements’.

In addition, a claim for an LTT relief is subject to passing a targeted anti-avoidance rule, which bars a claim where the transaction is a tax avoidance arrangement or part of such arrangements. A tax avoidance arrangement is one which ‘lacks genuine economic or commercial substance other than the obtaining of a tax advantage’. There is no equivalent to the controversial SDLT anti-avoidance rule, section 75A.

Residential leases

The rent element on the grant of new residential leases will not be taxed.

Reliefs

The reliefs under LTT are very similar to the reliefs for SDLT; however, as mentioned above, are subject to increased anti-avoidance provisions. As discussed at the top of this article, the biggest difference so far is the absence of a first-time buyers relief for LTT. There is also no seeding relief for Property Authorised Investment Funds and Co-ownership Authorised Contractual Schemes (as introduced for SDLT in 2016), though this is a point on which the Welsh Government are consulting. The relief is niche, and it is likely that it was not considered that a high enough volume of qualifying property transactions were to take place in Wales for the inclusion of a parallel relief to be of real benefit. Nevertheless, until April 2018, the relief will be available on qualifying Welsh property transactions, and will effectively be withdrawn once LTT is introduced.

Penalties

Cumulative tax-geared late payment penalties apply. They consist of an initial penalty of 5% of the tax due, plus a further 5% if the tax is unpaid after six months, plus a further 5% if the tax is unpaid after 12 months. Currently, there are no late payment penalties for SDLT, only late filing penalties.

Returns

An LTT return will need to be filed, and tax will need to be paid, within 30 days beginning the day after the effective date of the land transaction. As with SDLT, it will be possible to submit the returns to WRA online, once you have registered for an online account. Registration is available from 20 February 2018. The 30-day filing and payment window for SDLT will reduce to 14 days from 1 April 2019.

Enquiries

WRA have a 12-month period to open an enquiry into an LTT return. HMRC have a nine-month period to open an enquiry into an SDLT return.

Transitional arrangements

LTT will apply to land transactions in Wales which complete on or after 1 April 2018 subject to transitional arrangements.

Land transactions which complete on or after that date pursuant to contracts exchanged before 17 December 2014 will be subject to SDLT, not LTT, provided that

- the contract has not been varied

- the transaction does not involve the exercise of an option and

- the transaction does not comprise an assignment of rights or sub-sale

unless the contract was substantially performed before 17 December 2014.

Regulations are expected to make provision for additional transitional arrangements for various types of land transactions that span 1 April 2018.

Next steps

Those that regularly advise on, or enter into, land transactions in Wales should start considering how the new regime will affect them. At its simplest, land transactions that are anticipated to span 1 April 2018 should be reviewed to determine whether the tax cost will be higher or lower under the new regime.