Get ready for major changes

Share this article

Neil Warren considers the introduction of two reporting systems in the EU from 1 July 2021 and also new VAT rules for importing low value shipments of goods

Key Points

What is the issue?

From 1 July 2021, the introduction of the IOSS reporting system should simplify customs and paperwork procedures for businesses shipping goods worth up to €150 by accounting for ‘sales VAT’ rather than ‘import VAT’. A UK business will register for IOSS with the tax authority of a single member state and submit and pay monthly returns.

What does it mean for me?

A separate reporting system will be introduced to collect VAT on many services supplied in the EU; e.g. land services (B2C). Registration for the OSS and the submission of a single quarterly return to one tax authority will avoid having to separately register for VAT in each EU country where relevant sales are made.

What can I take away?

The new procedures are not changing the place of supply rules for services, only the way that the tax is collected and paid. For goods, there will be different VAT outcomes depending on whether a non-EU supplier sells goods directly to non-business customers or via an online marketplace.

Many GB businesses exporting low value shipments of goods to the EU have found the procedures very tricky since the end of the transitional deal on 31 December 2020. Arrivals in the EU are now subject to VAT and import duty – the free movement of the single market no longer applies. But a new system is being introduced by the EU on 1 July 2021, which should make procedures easier for shipments with a value of €150 or less. And, on the same date, the principles of the EU’s Mini-One-Stop Shop (MOSS) are being extended to include more supplies than just broadcasting, telecommunication and electronic services. This will make VAT accounting easier for many UK businesses.

Supplying services

Imagine the following situation: opera singer Mario is resident in the UK and registered for VAT. He has agreed to perform at three private concerts for wealthy individuals in Italy, France and Belgium; i.e. these are B2C supplies. The concerts are all taking place in September 2021. What does he do about VAT?

The opening challenge with any supply of services that involves international issues is to consider the place of supply rules for the service in question. In the case of B2C performance services, such as educational, entertainment and sporting activities, this depends on where they are taking place. In Mario’s case, his fees will be outside the scope of UK VAT but subject to Italian, French and Belgian VAT instead.

Until 30 June 2021, Mario would have needed to register for VAT in each EU country, submitting returns to three different tax authorities. He does not benefit from a local VAT registration threshold in these countries because he is not resident there; i.e. a zero-threshold applies.

The One Stop Shop scheme

The good news for Mario is that the introduction of the new One Stop Shop (OSS) non-Union scheme from 1 July 2021 will move the goalposts dramatically:

- Mario can still use the previous system if he wants to, having separate VAT registrations in each country. He might prefer this approach because it means he can claim input tax on local expenses when he submits his returns. With the OSS returns, only VAT on sales is being declared – any VAT on expenses must be recovered directly from the tax authority where the VAT was paid with the more cumbersome 13th directive system.

- Alternatively, he can register for the OSS non-Union scheme in any EU country of his choice – and then use his single registration number to charge and declare VAT in all EU countries where he performs. He still charges the rate of VAT that applies in the country where he is performing, not the rate that applies in the country where he has registered for OSS. A single OSS return will be submitted electronically each quarter, showing the VAT he has collected in each EU country.

- It makes sense for Mario to register in a country that speaks good English, namely Ireland, Malta or the Netherlands.

Land and other services

An important point to understand is that the new rules will not change any of the existing place of supply rules. The place of supply for Mario’s concerts has always been where they are held for B2C jobs, and this is unchanged from 1 July 2021.

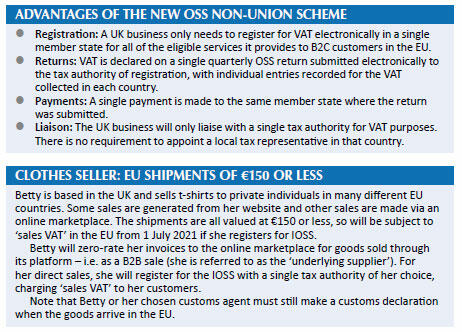

Another situation where the new rules will help is for land services (B2C); for example, where a UK bricklayer does B2C jobs in different EU countries. The place of supply for land services is where the property is based. However, these rules extend to many other ‘performance services’ – as listed in VAT Notice 741A s 9. For example, I have a private client who has holiday apartments in three EU countries and is VAT registered in each country – he could deregister on 30 June and pay all VAT through the OSS non-Union Scheme. See Advantages of the new OSS non-Union scheme.

The Import One Stop Shop scheme

Moving onto goods, the UK introduced new legislation on 1 January 2021, meaning that goods arriving into GB from anywhere in the world (or outside the UK and EU for a Northern Ireland business) would be subject to ‘sales VAT’ rather than ‘import VAT’ if the shipment value was €150 or less. This amount is also the duty threshold. Many overseas sellers have therefore registered for UK VAT if they directly sell goods to non-VAT registered customers in the UK. However, registration is not needed if they only sell goods via an online marketplace because the online marketplace deals with the VAT.

Similar procedures were due to be introduced in the EU on the same date but the start date was delayed until 1 July 2021 because of coronavirus. The new system will be known as the Import One Stop Shop (IOSS) scheme.

Features of the IOSS scheme

The new system is not mandatory and will work as follows:

- Goods enter the EU from third countries or third territories. The GB is a third country but different rules apply to Northern Ireland.

- The shipment value of the goods must be less than €150 excluding VAT (about £135) – this is the total value, not each item within a shipment.

So, for example, two print cartridges selling for €100 each in the same shipment would still be subject to import VAT. - The scheme excludes any goods that are subject to EU harmonised duties; e. g. alcohol or tobacco products.

- The goods are either being sold directly by the non-EU supplier or through an online marketplace. In the latter case, the online marketplace will account for the VAT on the sale to the customer. In this situation, the online marketplace is described as the ‘deemed supplier’. If a UK business only sells goods via an online marketplace, it will not need to register for the IOSS.

- Sales VAT will be charged rather than import VAT, based on the rate that applies for the goods in the EU country where they are being sold; e.g. Sweden and Denmark 25% and Germany 19% if the goods are standard rated.

- The VAT collected from customers is declared and paid to the tax authorities by the submission of a single monthly IOSS return to the member state of registration chosen by the non-EU supplier.

The IOSS is a practical way for a non-EU business to import low value goods into the EU which are free from import VAT. And the customer buying the goods has certainty about the amount of tax being charged. The shipments will also be free of customs duty – the €150 figure will replace the low value consignment relief threshold of €22. For a practical example of the new rules, see Clothes seller: EU shipments of €150 or less.

Accounting records and returns

As explained above, IOSS returns will be submitted monthly. They will record the total value of goods sold, the total VAT payable and the rate(s) of VAT for each member state where sales have been made. The first IOSS return will be due for July 2021, and must be submitted by the end of August; i.e. a one-month deadline. In terms of records and accounts, the EU VAT Directive does not require VAT invoices to be issued for B2C supplies, which extends to B2C deemed supplies as considered in the example of Betty. Records must be kept for ten years.

Conclusion

Now is a good time to start reviewing the new rules in time for 1 July 2021. The changes are very positive and will hopefully produce a welcome saving of time and administration costs for many UK businesses. Detailed guidance has been published by the EU, which is well written and is worth a read (see bit.ly/3dTTfgQ).