Grappling with the anomalies of inheritance tax penalties

Share this article

Inheritance tax administration, time limits and penalties bring their own unique complexities when compared to other direct taxes, which can have real consequences to the taxpayer.

Key Points

What is the issue?

The provisions governing the administration and collection of inheritance tax differ in important respects from those applicable to the main direct taxes and are frequently obscure in meaning.

What does it mean for me?

This article concentrates on anomalies in the penalty regimes for ‘inaccuracies in documents’ and ‘requirement to correct’, which may mean these regimes are wholly or partly ineffective in the inheritance tax context.

What can I take away?

These apparently pedantic distinctions have real consequences, particularly where the distinctions have been ignored in the drafting of legislation applicable across a number of different taxes.

Recently, there has been much litigation about the procedural aspects of the tax code, including several decisions of the Supreme Court on the Taxes Management Act 1970 alone. The provisions governing the administration and collection of inheritance tax, by contrast, have in many cases been the subject of no judicial consideration at all. These provisions differ in important respects from those applicable to the main direct taxes and are frequently obscure in meaning.

Paradoxically, the position has in some ways been made more difficult by the (so far partial) homogenisation of time limit and penalty regimes across different taxes starting from the Finance Act 2007, since the drafting of the common regimes does not always take into account the unique procedural background applicable to inheritance tax.

The overall result is a number of apparent anomalies, some of which operate harshly on taxpayers, and some of which may work to their advantage. This article concentrates on anomalies in the penalty regimes for ‘inaccuracies in documents’ (Finance Act 2007 Sch 24) and ‘requirement to correct’ (Finance (No. 2) Act 2017 Sch 18), which may mean these regimes are wholly or partly ineffective in the inheritance tax context.

In order to understand these anomalies, however, it is necessary to make some basic introductory points about the difference between administration and collection of inheritance tax and other direct taxes.

Inheritance tax is not an ‘assessed’ tax

In a well-known passage in Whitney v CIR (1924) 10 TC 88, it was said that there are three stages in the imposition of a tax: ‘There is the declaration of liability, that is the part of the statute which determines what persons in respect of what property are liable. Next, there is the assessment. Liability does not depend on assessment. That, ex hypothesi, has already been fixed. But assessment particularises the exact sum which a person liable has to pay. Lastly, come the methods of recovery, if the person taxed does not voluntarily pay.’

In its essentials, this statement remains true of the main direct taxes. The existence of an obligation on the taxpayer to pay a sum in respect of income tax, capital gains tax or corporation tax depends on the existence of an assessment (self- or otherwise). Where the taxpayer has filed a self-assessment return and has not received notice of enquiry within the enquiry window, HMRC’s ability to issue a further (‘discovery’) assessment is subject to the familiar time limits of four years in the ordinary case; six years in the case of a loss of tax brought about carelessly; and 20 years in the case of a loss of tax brought about deliberately.

If no assessment is made within these time limits, no debt is due, no matter what the taxpayer’s true liability was under the substantive provisions of the Taxes Acts. If an assessment has been validly made, however, there is no limitation period applicable to an action by HMRC to recover the resulting debt (Limitation Act 1980 s 37(2)(a)).

None of this is true of inheritance tax. Liability to inheritance tax does not need to be particularised by assessment. For inheritance tax, in Whitney terms, only stages 1 and 3 exist. The closest inheritance tax equivalent to an assessment, in that it carries a right of appeal to the tribunal, is a notice of determination under the Inheritance Tax Act 1984 s 221.

Unlike assessments to other direct taxes, however, notices of determination do not themselves create a debt. The obligation on the taxpayer to pay HMRC (if any) already exists simply by virtue of the chargeable transfer in question and the provisions of the Act specifying who is liable to pay the tax thereon (ss 199-205). Their salience, rather, is that HMRC may not take legal proceedings for the recovery of the debt unless the amount has been specified in a notice of determination, or agreed in writing by the taxpayer (Inheritance Tax Act s 242). Further, there is no time limit for the issue of a notice of determination. The time limits in the Inheritance Tax Act 1984 s 240 do not apply to the issue of notices of determination, but rather to HMRC’s ability to issue proceedings for recovery. In that sense, the time limits in s 240 operate more like conventional limitation periods than the assessing time limits in the Taxes Management Act 1970 ss 34 and 36.

These apparently pedantic distinctions have real consequences, particularly where the distinctions have been ignored in the drafting of legislation applicable across a number of different taxes.

Inheritance tax penalties under Finance Act 2007 Sch 24

Inheritance tax penalties comprise a mixture of ‘common regime’ penalties in various Finance Acts, and inheritance tax specific penalties in the Inheritance Tax Act 1984. The most important are:

- penalties for (careless or deliberate) inaccuracies in documents under Finance Act 2007 Sch 24, which are tax-geared; and

- penalties for delivering accounts late under Inheritance Tax Act 1984 s 245 of up to a maximum of £3,000.

The common regimes for late filing of returns and late payment of tax, in Finance Act 2009 Sch 55 and 56 respectively, do provide for tax-geared penalties but have not yet been brought into force for inheritance tax purposes. As long as this situation continues, it gives rise to one obvious piece of practical advice; namely, it is much better to file a correct account late (even very late) than an incorrect one on time.

There is more to say, however, because the application of the Finance Act 2007 Sch 24 regime to inheritance tax is not straightforward. Penalties are quantified as a percentage of ‘potential lost revenue’ (PLR). Para 5 provides that PLR ‘in respect of an inaccuracy in a document … is the additional amount due or payable in respect of tax as a result of correcting the inaccuracy’.

This applies straightforwardly enough to, say, income tax. Suppose a taxpayer has carelessly self-assessed in an amount of £100 and on the closure of an enquiry that amount is amended to £200. The effect of the amendment is that, subject to any appeal, an additional amount of £100 becomes due and payable (Taxes Management Act 1970 s 59B).

It breaks down, however, when applied to inheritance tax. As mentioned above, liability to inheritance tax does not need to be particularised by assessment. The filing of an inheritance tax account does not create a debt, and the correction of an inheritance tax account does not change the amount of any debt. It follows that, strictly speaking, no additional amount can become ‘due or payable’ as a result of correcting an accuracy in an inheritance tax account.

What is wrong with the drafting of para 5 emerges from comparison with its inheritance tax-specific predecessor, Inheritance Tax Act 1984 s 247. That quantified penalties for incorrect accounts as a percentage of ‘the amount by which the tax for which that person is liable … exceeds what would be the amount of that tax if the facts were as shown in the account’ (emphasis added). The drafter of s 247 recognised that unlike in the case of the assessed taxes, the obligation on a taxpayer to pay sums by way of inheritance tax to HMRC is independent of what is stated in the account. The drafter of Finance Act 2007 Sch 24 apparently did not.

Now, you will have observed that the logical consequence of this argument is that the PLR in respect of an inaccuracy in an inheritance tax account will always be zero, and therefore that nobody could ever be liable to a penalty of more than zero. Needless to say, this is an argument that the courts would be slow to accept. But it is not immediately easy to identify what is wrong with it, and the courts do not always shy away from holding that an administrative provision of the tax code has, in particular circumstances, simply misfired. For a recent example, see HMRC v Wilkes [2021] UKUT 150 (TCC).

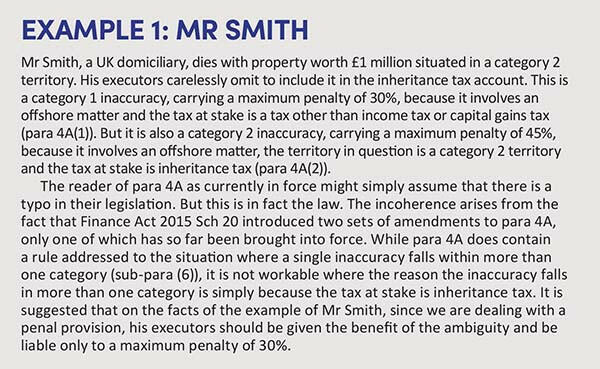

Other anomalies in Finance Act 2007 Sch 24 are starker. Fairly soon after its enactment, the Sch 24 regime was amended to create different ‘categories’ of inaccuracy, with a higher range of penalties applicable to higher categories. Categories 2 and 3 initially applied only to income tax and capital gains tax. They were then supposed to have been extended to cover inheritance tax with effect from 1 April 2016 – except that, because of an apparent drafting error, they may not have been.

- Para 4A(1) as amended provides that an inaccuracy is in category 1 if, inter alia, ‘it involves an offshore matter and: (i) the territory in question is a category 1 territory; or (ii) the tax at stake is a tax other than income tax or capital gains tax’ (emphasis added).

- Para 4A(2) then provides that an inaccuracy is in category 2 if, inter alia: ‘(a) it involves an offshore matter; (b) the territory in question is a category 2 territory; and (c) the tax at stake is income tax, capital gains tax or inheritance tax’ (emphasis added).

- Para 4A(3) defines category 3 inaccuracies in similar terms to para 4A(2). This leads to the incoherent result that the same offshore inheritance tax inaccuracy may simultaneously fall within category 1 and category 2 or 3. See Example 1: Mr Smith.

Image

Inheritance tax penalties under requirement to correct

The oddities continue when one looks at the requirement to correct penalty regime so far as it applies to inheritance tax. The requirement to correct regime applies where a taxpayer had ‘relevant offshore tax non-compliance to correct’ as at the end of 2016/17. If non-compliance was not corrected by 30 September 2018, the taxpayer may be liable to penalties of up to 200%; critically, careless or deliberate conduct is not a pre-condition for the imposition of such penalties.

However, problems arise with the definition of PLR as applied in the context of inheritance tax. The quantification of PLR for the purposes of requirement to correct penalties depends on whether the non-compliance consists of:

- a failure to deliver a return or other document: the PLR is the amount of the liability to tax under the applicable provisions of Finance Act 2009 Sch 55 para 24; or, if the non-compliance took place before 1 April 2011, the amount of liability to tax that would have been shown in the return as defined in Taxes Management Act 1970 s 93(9); or

- delivering a return or other document containing an inaccuracy: the PLR is the amount of the liability to tax under the applicable provisions of Finance Act 2007 Sch 24 paras 5-8; or, if the non-compliance took place before 1 April 2008, the difference described in Taxes Management Act 1970 s 95(2).

The significance of 1 April 2011 and 1 April 2008 is that these were the dates from which Finance Act 2009 Sch 55 and Finance Act 2007 Sch 24 respectively became applicable for income tax and capital gains tax purposes.

Three points arise. The first is that the general problem that arises with the quantification of PLR under Finance Act 2007 Sch 24 in the inheritance tax context, discussed above, applies equally to the requirement to correct penalty regime insofar as the non-compliance consists of delivering an inaccurate account.

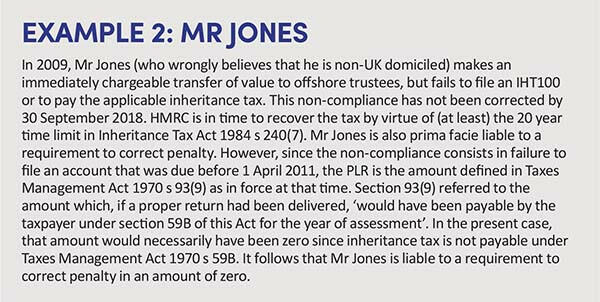

The second is that the amounts referred to in Taxes Management Act 1970 ss 93(9) and 95(2) are, by the terms of those provisions, amounts of income tax and capital gains tax only. It follows that offshore inheritance tax non-compliance earlier than a certain date cannot attract requirement to correct penalties, even if HMRC would be in time to recover the tax. See Example 2: Mr Jones.

The third point is that, in the case of non-compliance consisting of failure to file a return or other document on or after 1 April 2011, the PLR is quantified by reference to the applicable provisions of Finance Act 2009 Sch 55 para 24. But, as already mentioned above, Sch 55 has not yet been brought into force for inheritance tax purposes.

In the case of failure to deliver an inheritance tax account, therefore, it is arguable that there were no ‘applicable’ provisions of Sch 55. Accordingly, even if the facts of Example 2 were such that Mr Jones’s chargeable transfer took place in (say) 2015, it is arguable that he would still be liable to a requirement to correct penalty in an amount of zero.

Further discussion of some of these topics may be found in Dymond’s Capital Taxes, Chapters 28 and 29.