The Register of Overseas Entities will soon be coming into force

Share this article

Legislation for the Register of Overseas Entities will require the registration of overseas legal entities that acquire UK land, as well as many existing holdings. Information will be due within six months of the Register coming into force.

Key Points

What is the issue?

The Economic Crime (Transparency and Enforcement) Act 2022 legislates for the introduction of a publicly accessible register of overseas legal entities that own UK land and their beneficial owners – the Register of Overseas Entities.

What does it mean for me?

Registration will be required in relation to both newly acquired UK land and many existing holdings of UK land. There will be a transitional six month period for registrations to be completed once the register comes into force.

What can I take away?

Failure to comply with the registration requirements will affect an overseas entity’s ability to buy and sell UK land, and to create a charge over land. Failing to update the register will also be a criminal offence which may result in financial penalties and imprisonment.

The Economic Crime (Transparency and Enforcement) Act (‘the Act’) became law on 15 March 2022. Among other matters, the Act legislates for the introduction of a publicly accessible register of overseas legal entities that own UK land and their beneficial owners – the Register of Overseas Entities (‘the register’). This article provides a high-level overview of the register which will be maintained by Companies House.

Overview of the register

Registration will be required for many existing holdings of UK land, as well as new acquisitions. There will be a transitional six month period for registrations to be completed once the register comes into force. Disposals by overseas entities between 28 February 2022 and the end of the transitional period will also need to be notified.

Failure to comply with the registration requirements will affect an overseas entity’s ability to buy and sell UK land, and to create a charge over land. Failing to update the register or provide required information will be a criminal offence which may result in financial penalties and imprisonment.

The Act enables the Secretary of State to specify a date from which the register will come into existence. A written ministerial statement issued by the Department for Business, Energy and Industrial Strategy on 26 April 2022 confirmed that the government is working to ensure the register is in place as soon as is reasonably practicable, taking account of the need for secondary legislation and Companies House systems.

Definition of overseas entity

‘Overseas entity’ means a legal entity that is governed by the law of a non-UK country or territory. ‘Legal entity’ means a body corporate, partnership or other entity that is a legal person under its governing law. Tax residence is not taken into account, which means that registration will be required by non-UK incorporated but UK tax resident companies, where the other conditions for registration are met.

Trusts do not typically have the legal personality needed to be required to register. However, registration may be required by overseas legal entities owned by trustees, which could lead to the disclosure of information about the trust and associated individuals.

While trusts do not need to register on the Register of Overseas Entities, most UK trusts and certain non-UK trusts, including non-UK trusts that acquire UK land after 5 October 2020, will need to be added to the UK’s separate trust register. Members of the public can access beneficial ownership information about registered trusts if they have a ‘legitimate interest’ in the information held, or more widely in certain cases where a trust controls a non-EEA entity.

Overseas entities that must register

Beneficial ownership information will need to be provided before an overseas entity can register the legal title, a long lease or a charge against UK land. Unregistered overseas entities may be restricted from registering a disposal of UK land and an offence may be committed if an unregistered overseas entity disposes of UK land.

Overseas legal entities will need to register if they already own:

- land in England or Wales that was acquired on or after 1 January 1999; or

- Scottish land that was acquired on or after 8 December 2014.

For England and Wales, ‘land’ ownership for this purpose is a freehold estate or a leasehold estate granted for a term of at least seven years. Northern Irish land may trigger a registration requirement if it is a freehold estate or a leasehold estate in land granted for a term of at least 21 years. Scottish land must be registered if it is a registrable deed which is a standard security or a ‘qualifying registrable deed’, which is defined as being a registrable deed which is a disposition, a standard security, a lease or an assignation of a lease.

Overseas entities will need to provide information to Companies House if they dispose of land between 28 February 2022 and the end of the six-month transitional period.

Registering overseas legal entities

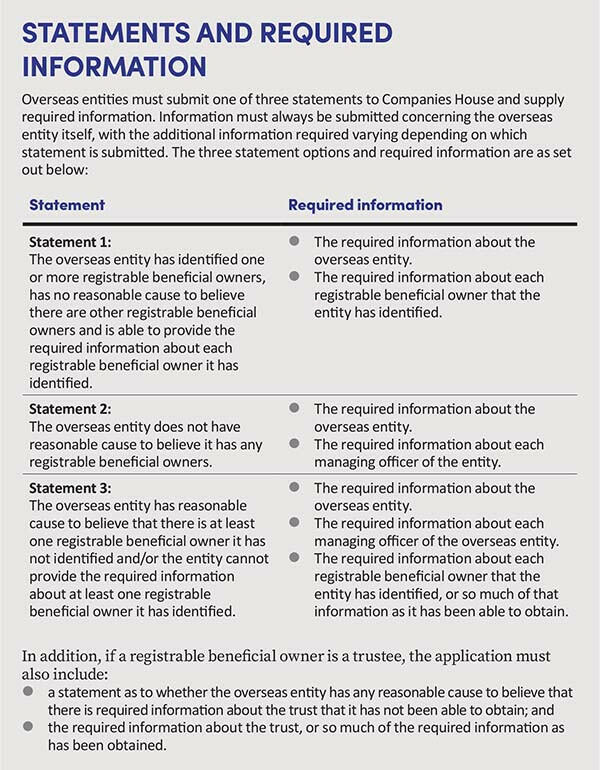

Registration applications from overseas entities must include:

- a statement concerning the information provided about registrable beneficial owners and, where obtained, the required information (see below);

- a further statement that the overseas entity has complied with its duty to take steps to identify beneficial owners;

- any further information required under separate regulations that have not yet been laid relating to the verification of registrable beneficial owners and managing officers; and

- the name and contact details of a person who may be contacted about the registration.

The Secretary of State may make further regulations about statements to be made and information to be provided.

Registration applications that are made within the six-month transitional period following the introduction of the register must also contain either confirmation that there have been no dispositions of UK land between 28 February 2022 and the end of the six-month period, or will need to provide the statements and the information specified below as it stood or stands at the date of disposal. The date of disposal and registered title number of the land (or title number of the title sheet for Scottish property) will also need to be provided. Exceptions from this requirement apply in some circumstances, such as where the disposal is or was required due to a court order.

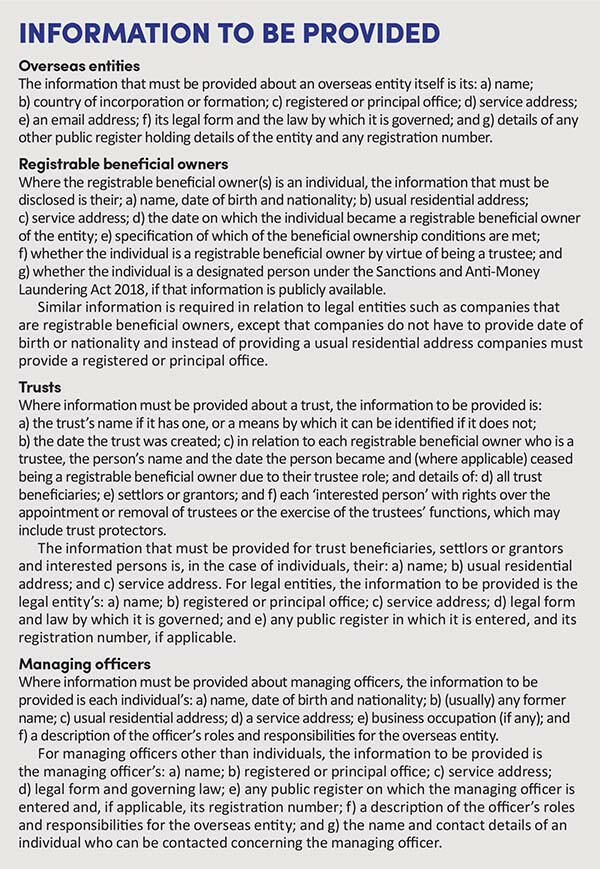

Image

Image

Updating the register

Annual updates or confirmation that there are no reportable changes will be required. The deadline for this is 14 days within the end of each year based on the anniversary date of the overseas entity first registering, unless the overseas entity changes the due date by shortening an update period and providing information by an earlier date.

Each annual update must include the information required as set out in the box above to register. The entity must also either:

- confirm it has no reasonable cause to believe that anyone has become or ceased to be a registrable beneficial owner during the update period; or

- provide details and relevant dates of each person who became or ceased to be a registrable beneficial owner during the update period, or as much information as the entity has been able to obtain.

Registrable beneficial owners

The definition of ‘registrable beneficial owner’ is intended to align with that which applies to the UK’s separate People with Significant Control (PSC) register that applies to UK legal entities. Individuals, legal entities, governments and public authorities can be registrable beneficial owners. Governments and public authorities are not considered further in this article.

Individuals and legal entities are registrable beneficial owners if they meet one or more of the below conditions:

- They directly or indirectly own more than 25% of the shares in the overseas entity.

- They directly or indirectly own more than 25% of the voting rights in the overseas entity.

- They hold the right, directly or indirectly, to appoint or remove the majority of the board of directors.

- They have the right to exercise, or actually exercise, significant influence or control over the overseas entity.

- Where trustees of a trust or members of a partnership, unincorporated association or other entity that is not a legal person under its governing law meet the above listed conditions in their capacity as trustees, etc. and have the right to exercise, or actually exercise, significant influence or control over the activities of that trust or entity.

Legal entities are not registrable beneficial owners if they are subject to their own disclosure requirements, as defined. This includes companies that must register on the PSC register and eligible Scottish partnerships which are within the scope of the Scottish Partnership (Register of People with Significant Control Regulations) 2017. Exemptions can also apply where individuals or legal entities own their beneficial interests through one or more legal entities if at least one legal entity in the chain is subject to its own disclosure requirements. The Act also contains provisions such that limited partners in non-UK partnerships may not be considered to be registrable beneficial owners in certain circumstances to be defined in Regulations to be laid by the Secretary of State.

Where shares are held by nominees, it is the person on whose behalf the nominee legally owns their interest in the overseas entity who will need to be named on the Register, where the registration conditions are met.

Obtaining information

Overseas entities must take reasonable steps to identify and obtain information about registrable beneficial owners. This includes giving an information notice to anyone the entity knows or has reason to believe is a registrable beneficial owner in relation to the entity.

Information notices must require recipients to state within one month whether or not they are a registrable beneficial owner in relation to the entity. If so, they must confirm or correct any information that is specified in the notice and provide any information that the notice states the overseas entity does not already have. If the registrable beneficial owner is a trustee, they must confirm or correct any of the required information about the trust that is specified in the notice and supply any information that the notice states the overseas entity does not already have.

Information notices may also be issued to persons that an overseas entity believes knows the identity of a registrable beneficial owner and to legal entities that are beneficial owners of overseas entities but do not meet the definition of a registrable beneficial owner. Such notices must ask the recipient to supply any information they have that might help the overseas entity to identify its registrable beneficial owners and to state whether that information is being supplied with the knowledge of the person to whom it relates. Recipients of these notices are not required to disclose information that is subject to legal professional privilege or, in Scotland, is subject to confidentiality of communications.

Removal from the register

Registered overseas entities will remain on the Register until they have successfully applied to be removed once they are no longer the registered owner of UK land. The Act does not provide a specific deadline by which applications for removal should be made, so presumably removal applications will need to be made in line with the usual annual deadlines for updating the register.

Next steps

Registrations can be made once the Secretary of State has specified a date for the Register to come into force. Where registration is required, it will be due within six months of the Register coming into force. Overseas legal entities may wish to consider whether they will be required to register or submit information to Companies House about disposals that occur between 28 February 2022 and the end of the six-month transitional period once the Register comes into force.

Overseas legal entities that need to register can consider to whom information notices should be issued once the Register is in force, and what information should be requested in information notices that are to be issued.