Growing SMEs

Share this article

William Franklin considers how growth shares can be used to incentivise expansion in SMEs

Key Points

What is the issue?

How does HMRC see growth shares?

What does it mean to me?

Are my clients interested in using growth shares or something similar?

What can I take away?

An overview of current practice in this area

Taxation seems to be moving to the top of the political agenda in the UK. The post-Scottish devolution referendum settlement and the proposed decentralisation of many Whitehall powers to city regions in England seems likely to intensify pressures on tax revenues from tax competition. However, there is growing pressure in the opposite direction as well to increase the tax take. The Conservative government, struggling with a seemingly intractable deficit, has been targeting tax planning through a series of ‘anti-abuse’ measures, some of which are controversial, such as advance payment notices (APNs).

In this context one of the remaining areas where the tax regime remains relatively benign is employee equity incentives. The highly tax-efficient enterprise management incentive (EMI) scheme is still widely used and continues to enjoy cross-party political support because of the contribution it can make to promote the growth of SMEs and, through them, the wider economy.

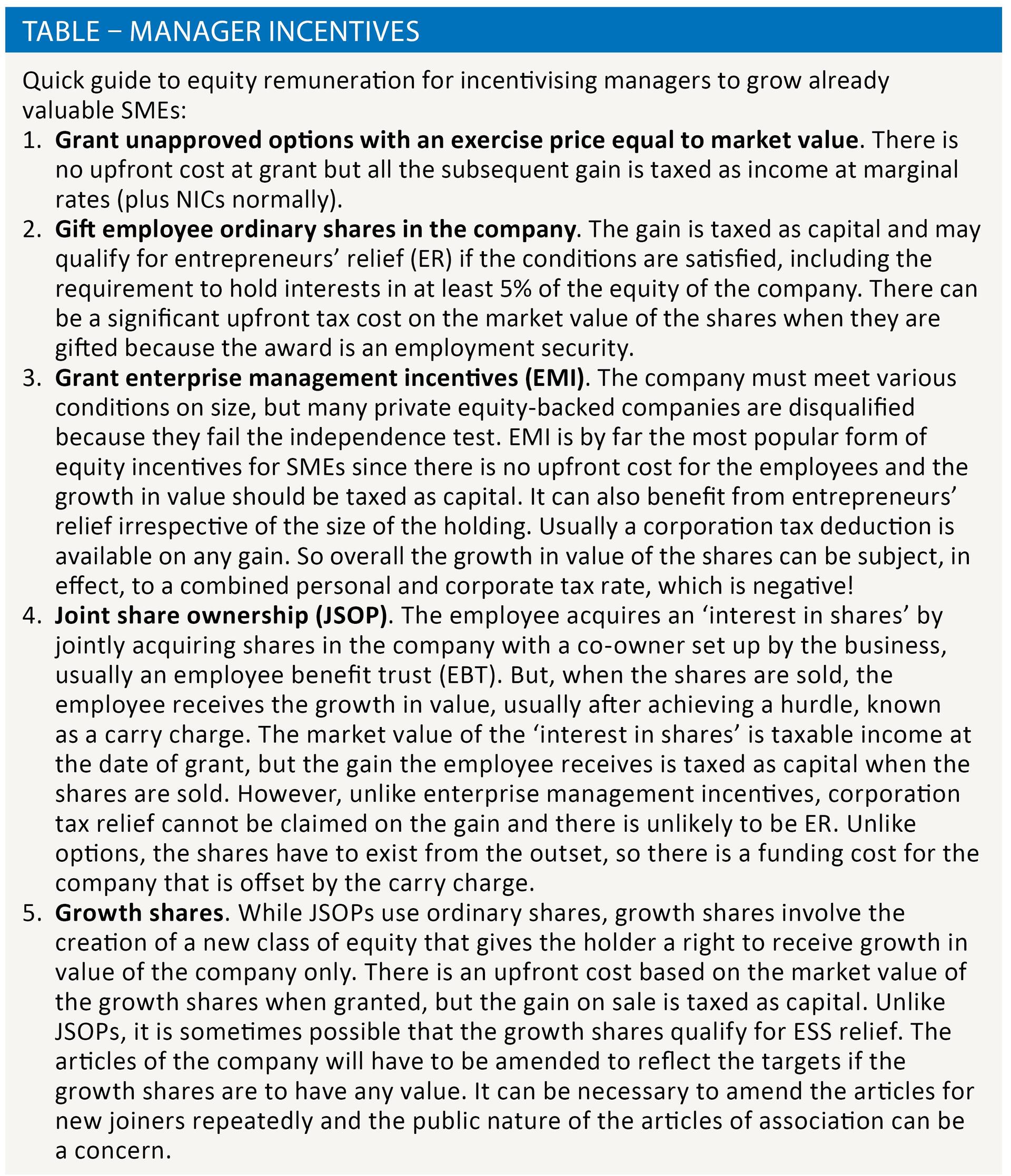

But if EMI is not available, perhaps due to the requirement for the business to be independent of other companies, the enterprise can turn to alternative equity-based arrangements as a tax-efficient way to reward growth. The most significant of these is growth shares. A summary of the main equity-based alternatives that are used in practice to incentivise the managers to grow their existing business is set out in the Table.

Growth shares usually involve the creation of a new class of equity that gives the employees who receive them the right to participate only in the growth in value of the company above the current value of the business when the shares are issued. In fact, usually a further increase in value (or hurdle) above the current value has to be achieved before the growth shares can participate in the value of the company and the employee can derive any value from them. Therefore they can be a powerful incentive to achieve exceptional performance and are usually introduced for this reason.

There is an initial income tax charge on the market value of the growth shares when they are awarded but any subsequent realised gain is taxed as capital. There is no National Insurance on the gain but the company does not qualify for a corporate tax deduction on it.

In recent years growth shares have often been used with the government’s employee shareholder status (ESS) scheme under which an employee can receive equity in his or her employer, on which the gain on realisation may be tax-free. However, this is on the proviso that the individual has agreed to forego some fundamental statutory employment rights in return for the shares.

HMRC has felt that growth shares had been a relatively under-reported and under-researched area of remuneration for some time. So last year they commissioned independent research into the use of growth shares and similar arrangements, and sought the views of employers, accountants, lawyers and employee benefit consultants.

The results were published last September in HMRC Research Report 372. Its central finding was that ‘growth shares have a definite and important role to play in encouraging the growth of businesses’. In the view of some advisers, they help to power the wider UK economy because they are used mainly by high-growth SMEs with a turnover of more than £10 million. These form a key part of the backbone of the UK economy, and are responsible for creating much of the economy’s new wealth and employment.

The report identified that growth shares were generally implemented by companies that were ambitious to grow and had short- to medium-term (three to ten years) exit strategies, including private equity backed companies. Technology, IT and media companies were strongly represented among the organisations that used growth shares but this was not limited to any particular sector. The arrangements were complex to implement and involved changes to the articles of the company, sophisticated share valuations and detailed explanations for the employees and the employer. It was considered that, since growth shares had to reflect the commercial circumstances of each company, they did not lend themselves to much standardisation. They were therefore unlikely to be used widely by companies unless they had a real need to use them to grow the business.

Perhaps surprisingly, the initial upfront cost of participation in growth shares was seen by some as a positive advantage compared with the tax and cost-free grant of unapproved share options because this required managers to have some ‘skin in the game’. Whether this was a widely held view among the employees concerned was not clear.

As HMRC noted, growth shares have been a poorly reported aspect of remuneration planning, so the survey findings are welcome.

Further information

Read HMRC Research Report 372.