Help with home work

Share this article

Michael Steed looks at the tax reliefs that are on offer when people work from home

Key Points

What is the issue?

An increasing number of people are working from home

What does it mean for me?

Advisers need to be able to advise on the tax reliefs available to home workers.

What can I take away?

That like many areas in tax, it’s necessary to understand the range of scenarios that may be in play. For example, mortgage interest is sometimes partially allowable and sometimes not allowable at all!

Can I get tax relief for working from home? – what an innocent question! The answer, as is so common in tax, is that there is a range of answers. In this article, I will be looking at what home working means for self-employed people (taken to include traditional partnerships) and employees. As you would expect, the language and some of the principles are different between these two groups.

In earlier articles in Tax Adviser, I have examined the issue of travel and subsistence costs for self-employed and employed workers generally, but in this article, I want to concentrate on home costs in particular.

Self-employed people

It is self-evident that the guiding test of deductibility for unincorporated businesses is the ‘wholly and exclusively’ test in ITTOIA 2005 s 34, so expenses that meet this test will qualify. How is that applied to people who work from home?

Before I address that question, let’s be clear about whether a client works from home at all. Many clients will assert that they do and therefore will want to claim tax relief for home expenses.

Leading case law reminds us that for many self-employed businesses, they will not effectively work from home as they have a ‘base of operation’ elsewhere, such as an office or a shop. The ‘base of operation’ test derives from Denning LJ’s judgment in the Court of Appeal in Newsom v Robertson [1952] 33 TC 452.

By way of contrast, an ‘itinerant worker’ does have a base of operation at home and this principally derives from Horton v Young [1971] 47 TC 60, so the implications as far as this article is concerned, is that home costs will be allowable, at least in part.

I don’t think that there’s any doubt that say an accountant who works full-time from home in a converted home office or a garden office (pod) will be able to claim some home costs and we will look at the detail of that below.

Whilst we are considering home offices and garden pods, clients will no doubt wish to claim either the costs of conversion or the capital cost of the garden pod and we will sadly have to advise them that no capital allowances are available for such expenditure, beyond say the costs of wiring and other services, office furniture and moveable partitions.

So what about the general house costs – what can a self-employed taxpayer claim?

An unincorporated business may be able to claim a proportion of its costs for things like:

- heating

- electricity

- Council Tax

- mortgage interest or rent

- internet and telephone use.

The taxpayer will need to find a reasonable method of dividing their costs, e.g. by the number of rooms used for business or the amount of time spent working from home.

So how does HMRC interpret the tax legislation in its guidance? It gives some specific examples in BIM47825 and I have kept the example numbers in this article.

If there is only minor use, for example writing up the trade records at home, then as example 1 shows, HMRC officers may accept a reasonable estimate without detailed enquiry. Therefore, if there is some use of the home for business purposes, then even if the ‘base of operations’ is elsewhere, there is potential for a modest claim.

CGT implications?

One of the critical conversations with clients that do work from home is that using a room exclusively for business use can have long-term adverse effects in respect of a possible loss of CGT PPR.

TCGA 1992 s 224(1) only excludes from relief any part of the dwelling house which is used exclusively for the purposes of a trade, business, profession or vocation. So a room which is used partly for business purposes and partly for residential purposes will qualify in full for relief. Our advice often includes having some domestic item in the office, such as a sofa and TV.

The kitchen of a small guest-house may be used equally to provide meals for the resident owner and to provide meals for the guests. As the kitchen is not used exclusively by the owner for the purposes of the trade TCGA 1992 s 224(1) cannot be used to restrict relief. Although a proportion of the expense of heating and lighting the kitchen, together with fuel for cooking, may be wholly and exclusively expended for the purposes of the trade and as such be deductible in computing the profits chargeable as income, it does not follow that a similar restriction should be made to the private residence relief.

The exclusive use test is a stringent one and HMRC guidance says that HMRC officers should not usually seek any restriction to relief for a room which has some measure of regular residential use. But occasional and very minor residential use should be disregarded. For example, if a doctor keeps private possessions in a room used as his or her surgery, the surgery should still be regarded as exclusively in business use (CG64663).

Simplified basis for expenses

In 2013, the government introduced not only the cash basis for self-employed people, but also a simplified basis of claiming some expenses

For taxpayers who work from home, it is possible to calculate allowable expenses using a flat rate based on the hours worked from home each month. This means it is not necessary to work out the proportion of personal and business use for the home, for example what percentage of the utility bills relate to the business.

The flat rate doesn’t include telephone or internet expenses. The taxpayer can still claim the business proportion of these costs by working out the actual costs.

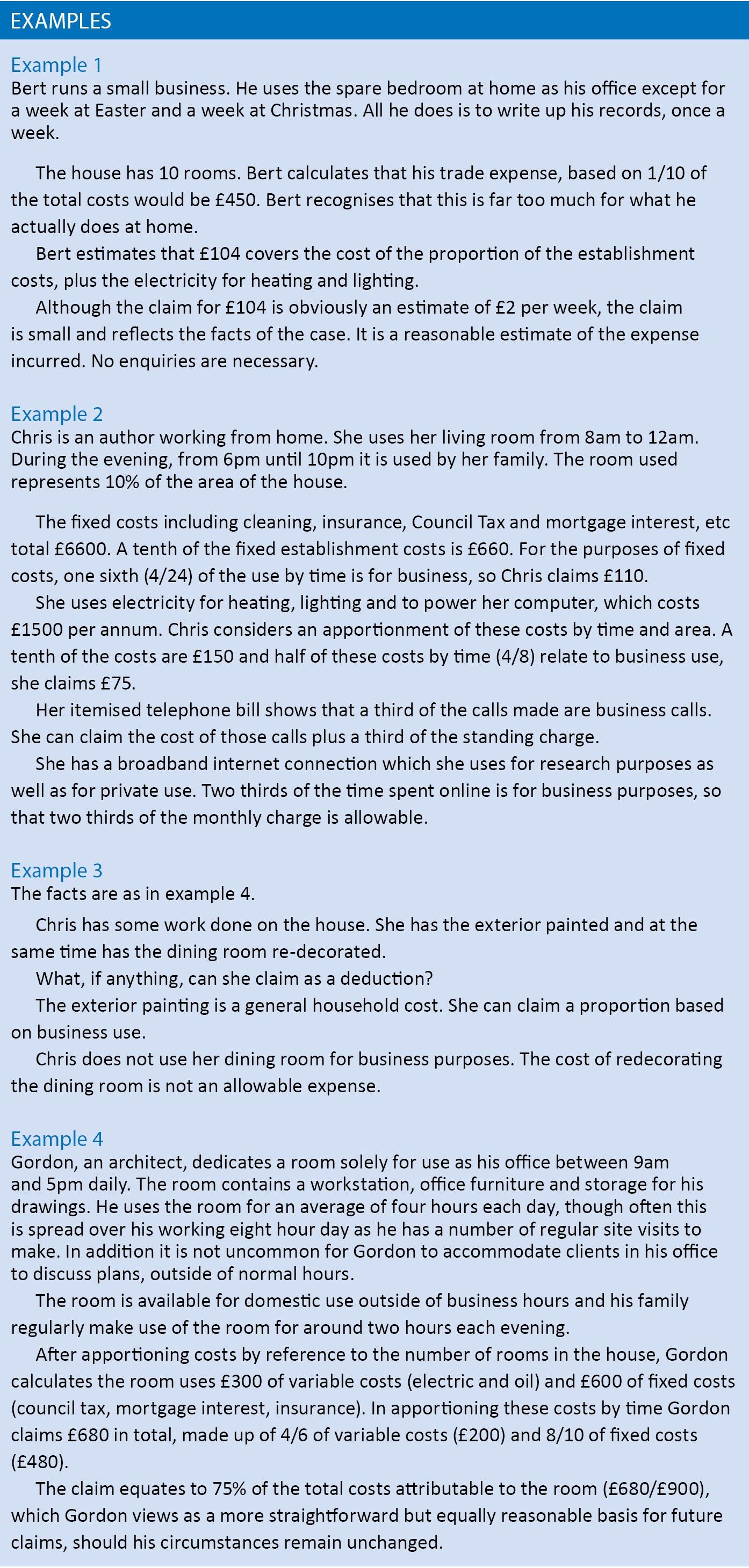

A flat rate deduction is only permitted if the individual works 25 hours or more a month from home. See table 1.

Living at on the business premises

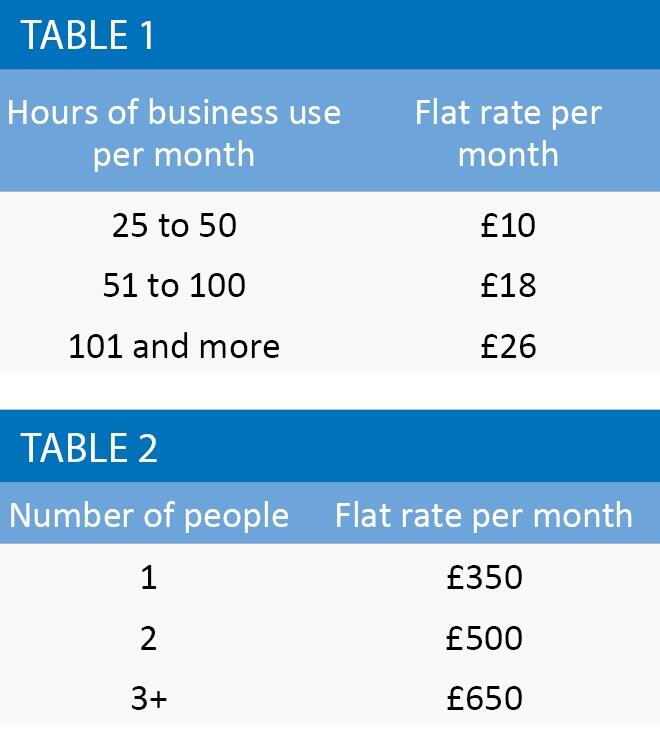

A small number of businesses use their business premises as their home, for example guesthouses, bed and breakfasts or small care homes.

Where the premises are mainly used to carry on the trade, a simplified expenses rule can be used instead of working out the actual split between private and business use of the premises.

After calculating the total expenses for the premises, a flat rate adjustment is subtracted to represent the personal use of the premises based on the number of people living on the premises. What is left can be claimed as a business expense. See table 2.

HMRC example

You and your partner run a bed and breakfast and live there the entire year. Your overall business premises expenses are £15,000.

Calculation:

Flat rate: 12 months x £500 per month = £6,000

You can claim:

£15,000 - £6,000 = £9,000

HMRC provides a simplified expenses checker so that taxpayers can compare a claim using simplified expenses with that from working out the actual costs.

Employees

As far as employees are concerned, there are in essence two groups: those who have to work at home (i.e. substantive duties at home) and those who choose to work at home. The primary legislation that is in play is ITEPA 2003.

Essentially the legislation provides a deduction for costs incurred by those who have to work at home (ITEPA 2003 s 336). For those who choose to work at home through, say, a homeworking arrangement then there may be an exemption for certain reimbursements paid by their employer (ITEPA 2003 s 316A).

The requirements of S336 ITEPA 2003 that the expenses for those employees that have to work at home, must be incurred ‘wholly, exclusively and necessarily’ ‘in the performance of’ the employee’s duties, means that relief can only be allowed for:

- the additional unit costs of gas and electricity consumed while a room is being used for work.

- the metered cost of water used ‘in the performance of the duties’ (if any)

- the unit costs of business telephone calls (including internet access).

Where it is not practical to calculate these extra costs, then a claim for £18/month for monthly paid employees (£4/week otherwise) can be made without having to justify the figure. This does not cover the cost of business calls for which an additional claim can be made based on actual costs.

Employees that arrange to work at home

Employers can make tax-exempt payments to employees for the additional household expenses incurred through regularly working at home. The relief (given by ITEPA 2003 s 316A) covers, for example, payments for heating and lighting costs, additional insurance, metered water, telephone or internet access charges. Where working at home leads to a liability for business rates, this can be included.

Costs must relate to the work area of the home. Costs that are the same, whether or not you work at home, cannot be included. Specifically this includes mortgage interest, rent, council tax and water rates.

Also excluded are costs that put the employee in a position to work at home. This would be expenses such as building alterations, furniture or office equipment. However, the employer can provide office equipment and office furniture to the employee tax free under ITEPA 2003 s 316.

Section 316A, allows employer tax-free reimbursements up to £4 per week without the need for supporting paperwork. If reimbursements are higher than £4 these must be justified and detailed records kept by the employee, or they must be specially agreed with HMRC. No relief is given for occasional working at home or for informal arrangements. This excludes, for example, work done at home in the evenings or at weekends. To qualify, employees need some sort of home working agreement where they regularly work at home.

S316, ITEPA provides for the tax-free provision by an employer of goods and services. This may be useful as it allows the provision to employees of supplies and services such as:

- office furniture and equipment such as desks, filing cabinets, fax machines etc

- stationery and normal office or workshop materials and supplies

- home telephone lines in some circumstances

- computer equipment and in certain circumstances an internet connection.

Not surprisingly, some benefits are excluded from the exemption, such as yachts and helicopters!

Using the £1,000 property allowance

It would be tempting for a client to ask if the 2017 £1,000 property allowance introduced into ITTOIA 2005 would be available for profit extraction from a company that operates from the client’s home, but the short answer is that the allowance is not available between connected persons.