Post-Brexit trade: complexities of B2B and B2C

Share this article

In the second of two articles, we examine some more of the issues which Brexit has raised when importing and exporting goods and services.

Key Points

What is the issue?

Brexit has thrown up some new issues in respect of the cross-border movement of goods and services. In this second article, we will look at some more of these.

What does it mean to me?

Advisers need to understand the new post-Brexit tax landscape that they are operating in.

What can I take away?

For post-Brexit UK to EU sales, some VAT simplifications have been removed and others have been introduced.

Brexit introduced some important changes to the tax aspects of importing and exporting goods and to a lesser extent, services, in and out of the UK. In these two back to basics articles (the first, ‘Life after Brexit’ was in the July issue), I want to explain the issues and how the processes have changed.

In this second article, I will examine business-to-business (B2B) triangulation of goods and how the process has changed since Brexit. I will also look at business-to-consumer (B2C) sales of goods and services, particularly in respect of sales of goods and services from the UK into the EU27 and how the One Stop Shop simplifications (the One Stop Shop and the Import One Stop Shop) are used. We will also look at how cross-border B2B and B2C services have changed.

B2B triangulation: prior to Brexit

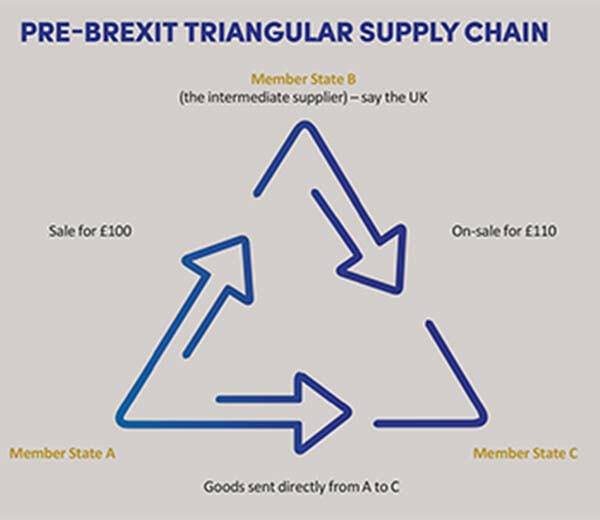

Prior to Brexit, the B2B triangulation process was a way to fix a particular problem that the EU had made for itself. To understand that, consider the pre-Brexit triangular supply chain that is shown on the page opposite.

A sells goods to B for £100. (The sale is zero-rated, as B gives A his VAT number.) B (the intermediate supplier) on-sells to C for £110. The goods are sent directly from A to C.

These were the original rules – and the UK version was contained in the Valued Added Tax Act 1994 until it was repealed by Brexit. The rules stated that for this one movement of goods, there are potentially two places of acquisition: one in C where the goods end up (which feels intuitively correct); but also in B because B had given A his VAT number to justify A’s zero-rating of the sale of the goods. So, the rules themselves created the problem – one movement of goods and two possible places of acquisition.

The EU Commission came up with a work-around to solve this: the B2B triangulation simplification. In simple terms, this meant that the supply to B and the supply from B were ignored for VAT purposes. They were to be treated as outside the scope of B’s VAT, thus leaving the A to C leg.

Note that although B’s supply to C was outside the scope of B’s VAT, it was still an EC sale, so it needed an entry on B’s EC Sales List (but with a Code 2 in the indicator column of the EC Sales List to explain the discrepancy).

The point of this simplification was essentially to prevent B from having to register in C to deal with the acquisition. It avoided what the EU was trying to avoid – lots of unwanted VAT registrations.

Image

B2B triangulation: post Brexit

So far, so good; but after Brexit, as the UK is no longer part of the EU, UK traders can’t use the simplification process, because the triangle needs all three corners to be member states in the EU.

Actually, that’s not quite true, as businesses with Northern Ireland VAT registrations (starting with ‘XI’ rather than ‘GB’) can still use the triangulation simplification as part of the Northern Ireland Protocol. As far as trading with the rest of the EU is concerned, it is treated as a mini-EU member state.

But this does mean that businesses in Great Britain (GB) cannot use the simplification in a post-Brexit world. GB here is a geographical term and not a political term, and means Scotland, England and Wales, and effectively the Isle of Man as well.

So what does this mean for GB businesses that are buying and selling B2B goods? Let’s look at the diagram again. We’ve still got B in position as the UK trader, buying goods from A in the EU and selling goods to C in the EU; and the goods are still going directly from A to C, thereby not entering the UK.

How does all this work post-Brexit? The critical point is that GB traders will need to be registered somewhere in the EU to make the VAT work. There are a couple of obvious options:

- Option 1: B could VAT register in state A and buy the goods in A. It could then do a zero-rated despatch to C and complete an EC Sales List and Intrastat entries to the extent that the value of the goods exceed the Intrastat threshold. B may have to appoint a fiscal representative to deal with the VAT compliance in A (this requirement varies between member states), thus increasing B’s costs.

- Option 2: B could VAT register in state C to deal with the acquisition from A and on-sell to the final customer in C. Intrastat entries will be needed above the Intrastat threshold. A fiscal representative may be needed.

In both cases, there will be VAT entries on a local VAT return. It’s worth remembering that B would be a non‑established taxable person in either A or C, so no local VAT registration threshold would be available.

A third way

However, there is another possibility post-Brexit. This is to make an EU triangle that is completed by B but in another member state that is neither A nor C. Although this may at first sight sound a bit strange, it does make sense as it puts B into the classic EU triangle, such that the triangulation simplification would then work.

The outcome is that B can now give an EU VAT number to A, and A can therefore zero-rate the supply to B. B will on-sell to C with no VAT (as this is outside the scope of B’s VAT), remembering to make an EC Sales List entry with the appropriate marker to show that this is a triangular sale and not a direct sale. There are no Intrastat entries for B in either direction as there is no actual movement of goods. There would be no entries on the VAT return as the supplies in and out of B are outside the scope of B’s VAT (so in contrast to registering in A or C).

As we have noted above, it will be necessary to check with the member state of choice whether a fiscal representative is required.

B2C movements of goods

Let’s now have a look at B2C sales of goods. I want to restate an important point about B2C sales. Many of these do not exceed £135 (€150) per consignment and are very often sold via the internet. Therefore, when these are sold from GB into the EU (and vice versa), there is no customs duties or import VAT to worry about and the rules replace import VAT with supply VAT (i.e. final mile VAT in the place where the B2C purchaser lives). The responsibility for the final mile VAT rests:

- with the seller (who will need to VAT register where the B2C customer lives); or

- with the sales platform, such as Amazon or Ebay, which will do this on behalf of the seller.

GB to EU sales of goods sent from the UK: the Import One Stop Shop simplification

In this section, I want to consider a GB VAT registered seller of goods not exceeding €150, selling via the internet to EU B2C consumers across the EU.

In order to understand this, let’s remind ourselves of what the drivers are. The place of supply of B2C goods post-Brexit is the place where the customer lives. A GB seller who is selling goods not exceeding €150 euros over the internet to B2Cs in different member states would be obliged to register for VAT in every member state that a customer lives in. This is a huge compliance burden and is the reason why the Import One Stop Shop simplification has been introduced to reduce that burden for third country sellers (including GB). Note that Northern Ireland sellers can use the EU One Stop Shop and don’t need to consider the Import One Stop Shop.

The simplification works as follows. The GB seller signs up for the Import One Stop Shop in one member state (the member state of identification). This gives the seller what I think of as a ‘toehold’ in the EU from which it can ‘springboard’ into the other member states where he has B2C customers. The seller is required to complete a single monthly multi-member state Import One Stop Shop return through which it can account for the local supply (final mile) VAT remotely.

The system also works in reverse. The UK insists that overseas sellers supplying goods B2C to UK consumers have to account for the UK (final mile) supply VAT, unless a digital platform such as Amazon or Ebay will do this for them.

B2C services provided by UK providers to EU B2C customers

So far we have been considering the cross-border movement of goods, but I now want to turn to services.

Brexit has made changes to B2C services that will affect such businesses as accountants and tax advisers, builders working in the EU and providers of EU holiday accommodation.

The key point to appreciate is that Brexit has changed some of the place of supply rules in both Northern Ireland and GB. Under the old rules, the basic place of supply (so where VAT is charged) was where the supplier belonged. As accountants and tax advisers, we would have been quite familiar with this when billing EU B2C clients in the EU; we would have charged UK VAT.

This has now changed and the place of service for such services is now where the EU B2C customer lives. These supplies are now therefore outside the scope of UK VAT.

Logically, you’d conclude that this means that there would be an obligation for the UK service provider to have to register in the EU to account for the B2C VAT. However, as I see it, at the moment this has not yet happened.

The position is clearer for other services. Holiday accommodation is charged where the land is, so a UK owner of holiday accommodation in Spain would have to charge Spanish VAT. A UK builder working in Spain for B2C customers would similarly have to charge Spanish VAT. Remember that there is no registration threshold for non-established taxable persons.

If UK traders (so both GB and Northern Ireland) have customers in more than one EU member state, they can choose between multiple VAT registrations, or using the One Stop Shop simplifications.

B2B supplies of services

This is one area of cross-border VAT where the rules have changed the least.

Consider a GB business user of, say, Adobe software licences, purchased from Adobe in the Republic of Ireland. Before Brexit, this would have been a standard cross-border EU supply of services and the place of supply would have been the UK (i.e. where the customer lives). The supply would therefore be outside the scope of Republic of Ireland VAT and inside the scope of UK VAT, where the VAT would have been brought to account in the UK by the standard 4-box reverse charge on the customer’s UK VAT return.

That has not changed as a result of Brexit; the rule is the same. The only change is that as we are now no longer members of the same VAT club, there is no need for the Republic of Ireland invoice to carry the words which in effect say ‘please do a reverse charge at your end’ for GB traders. Northern Ireland traders will still be in the same VAT club as the Republic of Ireland, so the pre-Brexit invoices will still be in play.