Capital tax issues affecting residential property investment

Share this article

In the second part of a series on property matters for individuals, we review the capital tax issues for property investors.

Key Points

Key Points

What is the issue?

Tax advisers will often be asked to look at capital tax issues for property investors and owners and they will need to be confident in their knowledge.

What does it mean to me?

This is a fascinating but practical area of tax, with lots of rules, that is constantly in demand from clients.

What can I take away?

Legislation is the key and a good grip on the law is essential to give good advice.

This is the second of a two-part, back to basics, article on property matters for individuals. The first article looked at income tax issues and this second will concentrate on the capital tax aspects of investing in residential property (including for own occupation). All legislative references are to Taxation of Chargeable Gains Act 1992 unless otherwise stated.

The basic capital gains tax issues

Property investors will at some stage contemplate selling or gifting residential properties out of their portfolios.

Sales to a genuine third party are straightforward. The gain is the net sales price (after incidental costs of sale) less the base cost (after incidental costs of purchase) or the March 1982 value if greater (s 35). Capital improvement costs during the period of ownership are also allowed (s 38), but there is no indexation allowance on the gain and rollover relief into new residential property is not permitted unless the properties are both furnished holiday lets. Reporting such sales is covered below.

The capital gains tax annual exemption allowance (£12,300) is normally available to an individual to set against the gains.

Gifting and selling at an undervalue

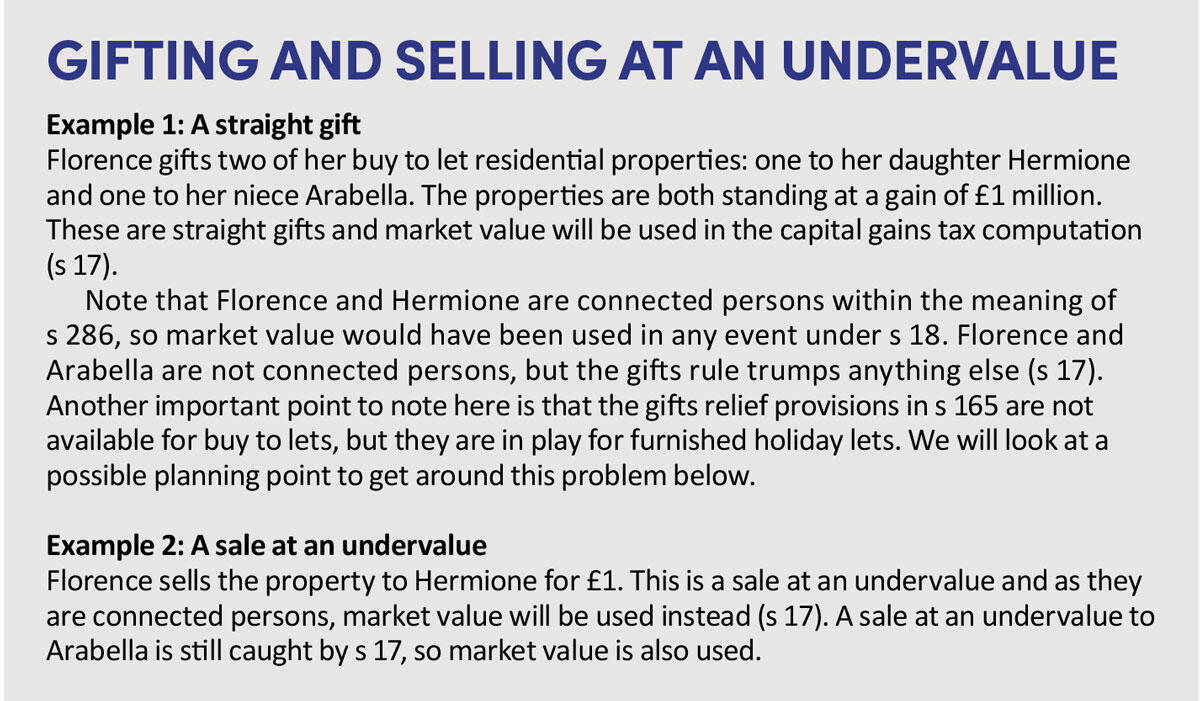

In family scenarios, gifting properties (or sales at an undervalue) regularly come across our desks. The basic capital gains tax rule is that a gift will be ignored and market value will be substituted (s 17). The only time a gift is allowed to stand for capital gains tax is on a gift to a spouse or civil partner (so a no loss, no gain basis).

Sales at an undervalue for capital gains tax purposes are also displaced and market value inserted instead (s 17). The donor is liable for the capital gains tax, but this can pass to the donee if unpaid within 12 months (s 282).

This leads us to broadly conclude that gifts of residential property for capital gains tax purposes carry unwanted capital gains tax liabilities that principally fall on the donor. This will need to be firmly placed in front of clients.

Principal residence relief

This is one of most widely used and admired capital gains tax reliefs in the UK tax canon. Its basic shape is well-known, in that it relieves gains on ‘an only or main residence’ (s 222). It actually covers two elements: house; and land, with the land comprising garden and grounds up to the ‘permitted area’ of 0.5 hectares (that’s about an acre in old money).

As advisers we are commonly asked about cases where the land is more than 0.5 hectares. Section 222(3) provides that the permitted area can be exceeded where the area required for the reasonable enjoyment of the dwelling house (or of the part in question) as a residence, having regard to the size and character of the dwelling house, is larger than 0.5 of a hectare. In that situation, the larger area shall be the permitted area. This occasionally comes up in tribunal cases and a recent example is Phillips v HMRC [2020] UKFTT 381 (TC).

Another question commonly asked by clients is: ‘How long do I have to be in a house for it to become my principal private residence?’ There is no straightforward answer to this and we have to use case law and a measure of common sense to solve the question.

The case law essentially turns on ‘the nature, quality, length and circumstances of the occupation’ (Goodwin v Curtis [1998] STC 475). I want to pause here, because it is not just the length of occupation as you would intuitively expect. A recent case that explored this is Stephen and Lisa Core v HMRC [2020] UKFTT 440, where a family’s occupation of a house was between six and eight weeks; the property was held to be a principal private residence as they could demonstrate that it had been their intention to reside longer, but circumstances changed.

A couple who are married or in a civil partnership and living together can only have one principal private residence between them. A couple is treated as living together unless they are separated. A couple who are married or in a civil partnership but just happen to live apart (perhaps seen in later-life relationships) can still only have one principal private residence at any given time (s 222(6)).

Another principal private residence angle that we are likely to encounter is where a client has more than one property used as a residence. The question is which of these will be that person’s main residence? It is essential that we clearly lead our clients through the legislation and to help them frame their principal private residence decisions.

Essentially, the client is able to choose which of the residences is their main residence and can settle this by an election under s 222(5)(a) within two years of the purchase. If that person does not settle the matter by election, then HMRC is entitled to draw its own conclusion on the facts and that may well not go in the direction that the client would wish (see Hussain v HMRC [2022] UKFTT 13, as an example).

Note that there is some basic anti-avoidance legislation in the principal private residence legislation to stop non-residents (say, who are living and working abroad) to nominate their UK house as their principal private residence by election whilst they are out of the UK. To attain UK principal private residence status, the individual must have spent at least 90 midnights in the property and be tax resident in the UK (s 222B).

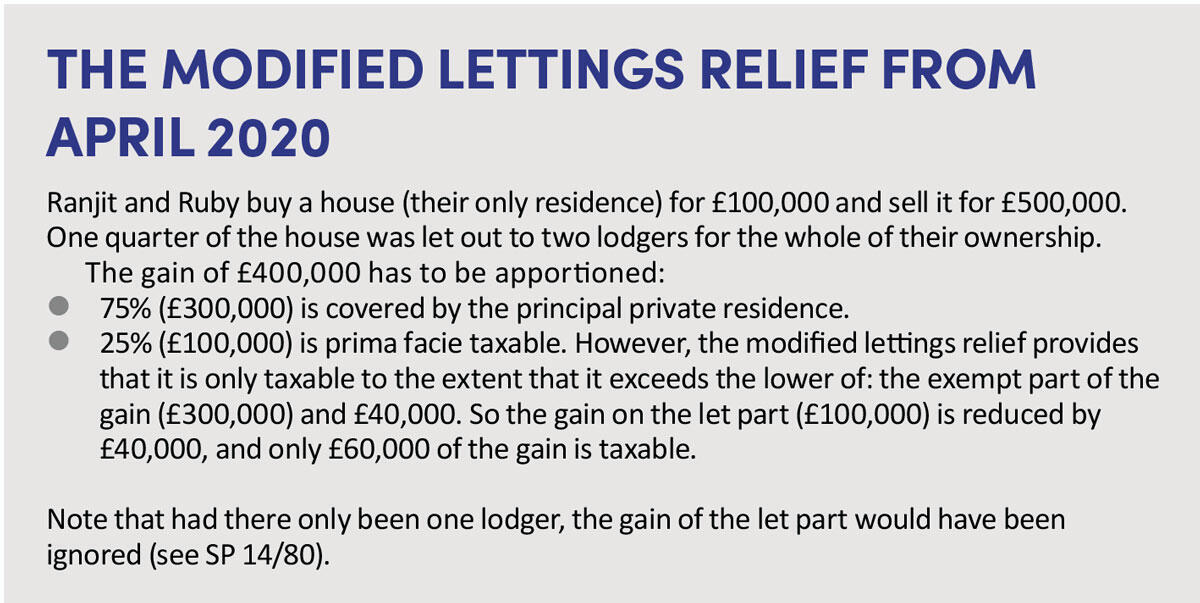

Lettings relief

The principal private residence subsidiary relief, lettings relief, underwent some radical surgery in April 2020, such that it is now a pale copy of the original (which gave additional deemed principal private residence relief on whole house lets). The long and the short of this is that it is now effectively a lodgers’ relief, where the owner is in shared occupation with the lodgers – and is best viewed as the capital gains tax version of rent a room relief (s 223B).

Disposals of UK property by UK residents and non-residents

As part of the capital gains tax mechanics of disposal, taxpayers will need to be clear about the capital gains tax reporting and payment deadlines that are required in the legislation in respect of disposals of residential property. Non-UK resident individuals have been required to report disposals of UK residential property online to HMRC since April 2015 (extending to commercial property, land and disposals of property rich companies since April 2019) within 30 days of completion (extended to 60 days from 27 October 2021).

UK residents were drawn into the net from April 2020, such that disposals which result in actual capital gains tax liabilities were reportable within 30 days of completion (also extended to 60 days on 27 October 2021). If there is no actual capital gains tax liability for a UK resident (say because of principal private residence relief or a gain within the capital gains tax annual exemption), then no 60 day report is required (Finance Act 2019 Sch 2).

For both non-residents and residents, the broad rule is that any tax due must be paid within the same period, but for non-residents this has only been true since April 2019.

The basic inheritance tax issues

Sales of properties to third parties will not create inheritance tax liabilities. Gifts most certainly will (unless it’s a spousal/civil partnership gift, which is covered by the inheritance tax spousal exemption) (Inheritance Tax Act (IHTA) 1984 s 18).

A gift by an individual to another individual is a potentially exempt transfer under IHTA 1984 s 3A, so gifts by Florence to Hermione and Arabella (as in the example above) will not be taxed at that point. Indeed, they will escape inheritance tax altogether if Florence survives the required seven years in IHTA 1984 s 3A(4).

This important point reminds us that conversations with clients about making gifts earlier, rather than later, is a part of what we do as competent tax advisers. If the donor fails to survive seven years, then inheritance tax is prima facie payable (and is payable by the donees in the absence of any other provision), although there are tapering provisions for the tax due if the donor survives at least three years (IHTA 1984 s 7(4)).

Gifts and tax planning: the use of a discretionary trust

We noted above that gifts of buy to lets to, say, a family member will bring unwanted capital gains tax liabilities on the donor and that rollover relief is not available for such gifts (but it is available for furnished holiday lets).

A way around this is to consider putting the buy to let into a discretionary trust, keeping it in the trust for a while and then passing it to the intended beneficiary. The reason that this works (especially in properties that are within the donor’s available nil rate band) is in s 260. The mechanism is that the gift into the trust is a disposal for capital gains tax purposes, but s 260 allows the donor to swap a capital gains tax liability for an immediate inheritance tax liability. (The transfer into the trust would be a chargeable lifetime transfer, so taxable to inheritance tax at 20% to the extent that the value of the gift exceeds the available nil rate band.) If the value of the gift into the trust is below the available nil rate band, then the inheritance tax charge is zero. If it’s above, then some inheritance tax will be due.

When the buy to let is transferred to the intended beneficiary, s 260 is invoked again and no capital gains tax accrues to the trustees, but there is an inheritance tax charge – the standard exit charge. The value of this has to be taken into account in the exercise. This mechanism can be useful though, especially in lower value properties, and the end result is that the beneficiary takes on the base cost of the original donor. Legal advice on the trust would be needed.

Inheritance tax business property relief

Business property relief is a valuable relief. The key point here is that it is not normally available for residential properties, including furnished holiday lets (even though they often qualify for better tax reliefs).

HMRC will normally take the view that buy to lets and furnished holiday lets are investment properties and not business property within IHTA 1984 s 105(3). Case law generally supports this view (see HMRC v Pawson [2013] UKUT 50 (TCC)). Very occasionally, a furnished holiday let will qualify, but this is very much the exception rather than the rule (see Graham v HMRC [2018] UKFTT 306.

Conclusion

As ever in tax, as advisers, we need to be aware of the whole landscape. In residential property transactions, we need to be able to use and understand both the capital gains tax and the inheritance tax aspects of transactions.