Hidden traps?

Share this article

Making Tax Digital for VAT will be extended to voluntary registrations for VAT periods beginning on 1 April 2022 or later. Neil Warren considers whether it makes sense for a business to deregister before this date

Key Points

What is the issue?

An entity that is voluntarily registered for VAT must keep digital records and submit digital VAT returns for periods beginning in April 2022 and later.

What does it mean for me?

Deregistration is an option for voluntary registrations, but there are pitfalls to consider before going down this route; e.g. a potential output tax liability on some stock and assets on the final return submitted by the business, and possibly capital goods scheme adjustments.

What can I take away?

Deregistration will avoid the need to comply with MTD but it will mean a loss of input tax for a business and increased overhead costs. It is a case of evaluating the numbers to decide on the best strategy.

Many UK businesses have either ceased to trade or suffered reduced turnover due to the Covid-19 pandemic. In some cases, this lost turnover will be permanent and therefore offer the opportunity for deregistration. Many other businesses are VAT registered on a voluntary basis anyway, having always traded below the compulsory registration threshold.

However, the goalposts will move in April 2022, when Making Tax Digital (MTD) will be extended to all VAT registered businesses, including voluntary registrations. Deregistration will be actively considered by many business owners to avoid the challenges of MTD but they must be aware of some of the pitfalls. Although deregistration might seem to be an easy option, there are some hidden traps in the legislation that are sometimes forgotten.

Deregistration limit

A business can deregister if it expects its taxable sales in the next 12 months will be less than £83,000. The deregistration threshold has traditionally been £2,000 less than the registration threshold, which is currently £85,000. These figures will be frozen until at least 2024, possibly longer.

A request for deregistration based on expected sales can only be made from a current or future date. In other words, you are a member of the VAT club until the date when you decide to leave and there is no scope to deregister retrospectively if you are still trading.

Note: the £83,000 threshold includes zero-rated and reduced-rated income but excludes exempt sales or those that are outside the scope of VAT.

Pricing trap

Imagine that one of your clients runs a hairdressing salon and her annual sales are £90,000 including VAT. The turnover figure recorded on the annual accounts will be £75,000; i.e. excluding VAT. Your initial view will be that she can deregister for VAT because sales excluding VAT are well below the £83,000 threshold. This is partly correct. But what happens if your client does not reduce her prices when she deregisters?

In other words, she does not pass on the VAT savings to her clients. Her expected sales in the next 12 months will still be £90,000, above the deregistration threshold. She should not deregister.

This challenge is relevant to many retailers and entities that price their goods or services on a VAT inclusive basis. If we reconsider the maths, the hairdressing salon will need to reduce its prices by, say, 10% when it deregisters; i.e. its expected annual sales will be £81,000.

Stock and assets

Clients can deregister online by completing form VAT7 and it is a straightforward process. However, they must firstly consider if there are hidden pitfalls with the output tax rules about stock and assets still owned at the time of deregistration. Any VAT due under these rules must be declared on the final return but there is potential good news:

- A business can ignore any stock or assets where no input tax was claimed when it was purchased; e.g. a computer bought from a friend.

- Output tax is calculated according to the market value of the item on the deregistration date. As most items depreciate, this will be a lower figure than the original cost price. Valuations can take account of obsolescence, wear and tear, physical damage and a reduced value if an item is out of date.

- No output tax is payable on zero-rated or exempt items; e.g. food stock for a grocer.

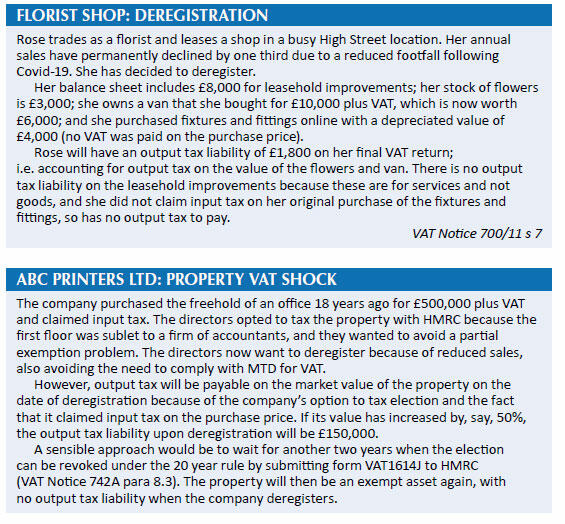

- If the total VAT payable after all of the above exclusions is less than £1,000, then no output tax is due; it is de minimis. See Florist shop: Deregistration.

Property warning

The biggest pitfall with deregistration is to forget about a non-residential property owned by a business seeking to deregister, and specifically property where a past option to tax election has been made with HMRC. As with much of the land and property legislation, there are some important questions to consider:

- Did the business pay VAT and claim input tax on the purchase of the property, either because it was less than three years old, or because the seller had opted to tax? If the answer is ‘no’, there is no output tax liability on the final return when it deregisters.

- Has the business opted to tax its interest in the property?

- If the answer is ‘yes’ to these two questions, output tax is due on the market value of the property in question when the business deregisters.

There have been many horror stories – see ABC Printers Ltd: Property VAT shock.

Capital goods scheme

Here is another scenario: imagine that a fully taxable trading partnership purchased a property five years ago costing £500,000 plus £100,000 VAT. The partners didn’t opt to tax their interest in the building because it was only used for taxable business purposes; i.e. no renting activities were involved. The partners now want to deregister because of reduced turnover.

In this situation, there will be no output tax liability on their final VAT return with the stock and assets rules. This is because they never opted to tax the property so it is an exempt asset. However, because the property cost more than £250,000 excluding VAT, the original input tax claim of £100,000 is subject to a ten year adjustment period under the capital goods scheme (HMRC VAT Notice 706/2 s 3).

These adjustments would have been nil in the first five years of ownership because the property was wholly used for their taxable business activities. However, deregistration means that 50% of the input tax will need to be repaid on their final VAT return because the asset is exempt from VAT under the stock and assets rule. Years six to ten are therefore linked to exempt rather than taxable use, producing an input tax repayment of £50,000. They might decide to remain VAT registered for another five years when the scheme adjustments will end.

B2C services post Brexit

If you advise clients who sell business to consumer (B2C) services to EU customers, there might be a post-Brexit opportunity to deregister. The process is as follows:

- The starting point with the place of supply rules is that the VAT liability depends on where a supplier is based for B2C services; i.e. the UK.

- However, there is a list of professional services in the legislation where no VAT is charged if the customer is based ‘outside UK’ and the place of supply becomes the customer’s country; i. e. outside the scope of UK VAT. Until 31 December 2020, this legislation only applied if the customer was ‘outside EU’.

- For a list of qualifying services, see HMRC VAT Notice 741A s 12.

- The change from ‘outside EU’ to ‘outside UK’ since 1 January 2021 means that many more supplies of services are no longer subject to UK VAT, which creates a potential opportunity for deregistration in some cases.

Without diverting to a completely different topic, if you act for clients who provide B2C services to EU customers, they must check that there is no requirement to register for VAT in the EU country where the customers live under the EU’s ‘use and enjoyment’ legislation. These rules vary in different member states, but care is needed; it is beyond the scope of this article.

Conclusion

If a voluntarily registered business has no VAT horrors with the issues I have considered, it might decide to deregister on 31 March 2022 to avoid having to join the MTD club. This will largely depend on whether the input tax gains of being registered, or perhaps the prestige benefit of registration, outweigh the costs of MTD compliance.

Don’t forget that bridging software is still an option with MTD, which will be useful to many entities that use spreadsheets. According to HMRC, about one third of voluntary registrations are already MTD compliant; it will be interesting to see how things evolve with the others.