HMRC gets more time

Share this article

Dawn Register and Helen Adams consider the draft legislation extending assessment time limits for offshore non-compliance

Key Points

What is the issue?

Legislation for the Finance (No. 3) Bill will, when enacted, further extend the time limits within which HMRC can issue discovery assessments. This change will apply to income tax, capital gains tax and inheritance tax where there is offshore non-compliance to which the 20-year time limit does not apply.

What does it mean to me?

The new time limits give HMRC more time to undertake enquiries and investigations relating to offshore matters and offshore transfers subject to the limited safeguards in the draft legislation.

What can I take away?

Advisers should consider whether they and their clients need to alter their record keeping procedures to retain sufficient evidence to successfully challenge incorrect discovery assessments issued using the new time limits.

HMRC’s ability to assess additional income tax and capital gains tax (CGT) is restricted by statutory assessment time limits (TMA 1970, s34, s36, s37A and s40) in the absence of open self assessment enquiries (e.g. under TMA 1970, s9A). Similar restrictions apply to inheritance tax (IHT) by virtue of IHTA 1984, s240.

Following closure of the consultation on extending these time limits for non-deliberate behaviour relating to offshore matters and offshore transfers (“offshore non-compliance”) HMRC published the Summary of Responses and draft legislation on 6 July 2018 before issuing Clauses 79 and 80 of Finance (No. 3) Bill on 7 November 2018. The legislation will come into force following Royal Assent of that Bill, although it should be noted that the House of Lords’ Economic Affairs Finance Bill sub-committee recommended that the clauses be dropped as they considered the time limit extensions to be “unnecessary and undesirable”.

Why are the rules changing?

Since 2010 successive governments have facilitated HMRC’s activities in tackling tax evasion and non-compliance involving offshore income and assets. Legislation introduced higher penalties for offshore non-compliance plus offshore asset moves penalties, asset-based penalties, strict liability criminal offences, unexplained wealth orders and the Requirement to Correct (RTC). The UK joined the Common Reporting Standard (CRS) so HMRC now automatically receives data from more than 100 countries annually, including destinations of particular interest such as Hong Kong, Israel, Monaco, Switzerland, Singapore, The Bahamas and Andorra.

Notwithstanding the development of HMRC’s abilities to analyse vast amounts of data to identify discrepancies for investigation, HMRC is concerned that it takes time to investigate taxpayers, especially to establish the facts surrounding complex offshore transactions and offshore structures. HMRC therefore wants the assessment time limits extended to give them more time to investigate and assess additional tax liabilities. However, the changes are not limited to ‘complex’ matters.

What are the existing time limits?

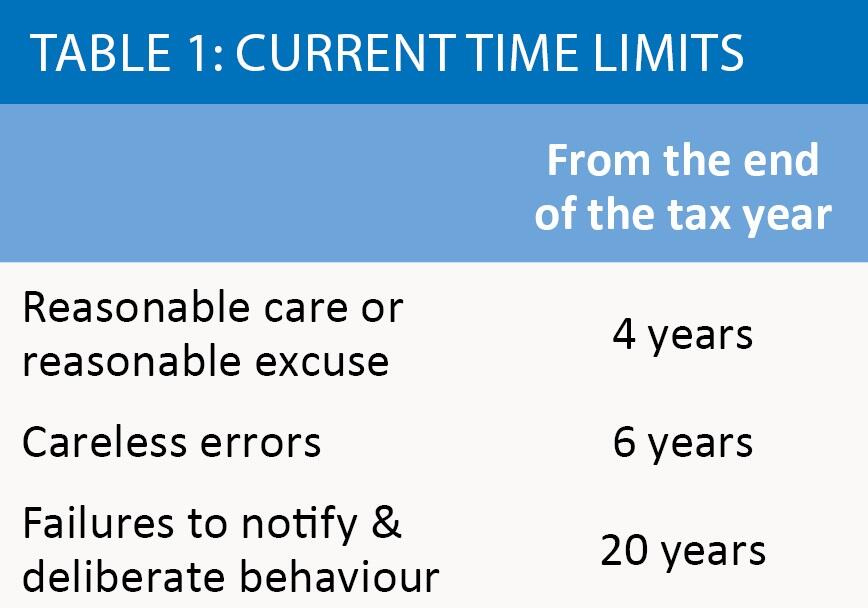

Existing assessment time limits for income tax and CGT, subject to the changes for the RTC, are shown in table 1.

The IHT time limits mirror those for income tax/CGT except that there is an unlimited time limit in cases of deliberate non-submission of an IHT account. The IHT deadlines are stated as a period of years from the later of:

- The due date for paying the tax, and

- The date on which the last payment was made and accepted.

However, the above deadlines differ for deceased taxpayers (TMA 1970, s 40). Also, for offshore tax non-compliance involving income tax, CGT and IHT, the RTC stops time limits expiring between 6 April 2017 and 4 April 2021 so that they expire on 5 April 2021 instead (F(No2)A 2017, Sch 18, Para 26).

What doesn’t change?

The draft legislation does not extend the assessment time limits for:

- corporation tax;

- transfer pricing adjustments;

- assessments on personal representatives;

- income received after the year for which it is assessable (TMA 1970, 35);

- the existing 20 year and unlimited time limits;

- UK situs issues.

What is changing?

HMRC is extending the current four and six year assessment time limits to 12 years for income tax, CGT and IHT relating to ‘offshore matters’. Taxpayers who took reasonable care will therefore be treated in the same way as those who were careless, if these clauses are enacted as drafted. The test for offshore matters in other parts of the legislation (e.g. FA 2008, Sch 24, Para 4A(4)) is used in the Bill although an extra element is added, namely “income or assets received in a territory outside the United Kingdom”.

The change to the time limits also applies to ‘offshore transfers’ “which make the lost tax significantly harder to identify”. This restriction is new and does not appear in other legislation such as that for penalties. The legislation say that situations where tax is significantly harder to identify include:

“…any case where, because of the transfer—

(a) HMRC was significantly less likely to become aware of the lost tax, or

(b) HMRC was likely to become aware of the lost tax only at a significantly later time.”

The draft legislation does not explain what ‘significantly’ means in this context. Will it, for example, relate to the relative level of transparency or information sharing between the jurisdictions and HMRC? Consequently, it is likely that the Tribunals will need to shed light on this concept in due course.

However, the 12-year time limit will not apply where:

a. information is received by HMRC from an overseas jurisdiction (whether by automatic information exchange or under another information exchange agreement);

b. On the basis of this information HMRC could reasonably have been expected to be aware of the loss of tax; and

c. It was reasonable to expect the assessment to be issued before the current assessment time limits expired.

This safeguard recognizes the impact that overseas’ data is predicted to have on future enquiries and investigations. However, the ease of its application is uncertain given the use of ‘reasonable’ in two parts of the test. Perhaps it will prove a greater safeguard in simple cases (e.g. a UK resident and domiciled person with undisclosed offshore bank interest) compared to complex cases involving domicile, remittances and anti-avoidance legislation that typically take HMRC longer to gather evidence and resolve. It should also be noted that there is no equivalent limitation on HMRC’s use of the new time limits where HMRC is given information by a taxpayer or the taxpayer’s adviser in time to assess any additional tax due within the standard 4 or 6 year time limits.

The new time limit will apply to periods that remain in date for assessment at 6 April 2019, according to the government’s consultation responses, giving a retroactive aspect to this new legislation.

This will affect income tax and CGT within scope of these changes for:

- 2013/14 and subsequent years where careless errors occur; or

- 2015/16 in all other cases.

For IHT the new time limits will apply to chargeable transfers on or after:

- 1 April 2013 where careless errors occurred; or

- 1 April 2015 in all other cases.

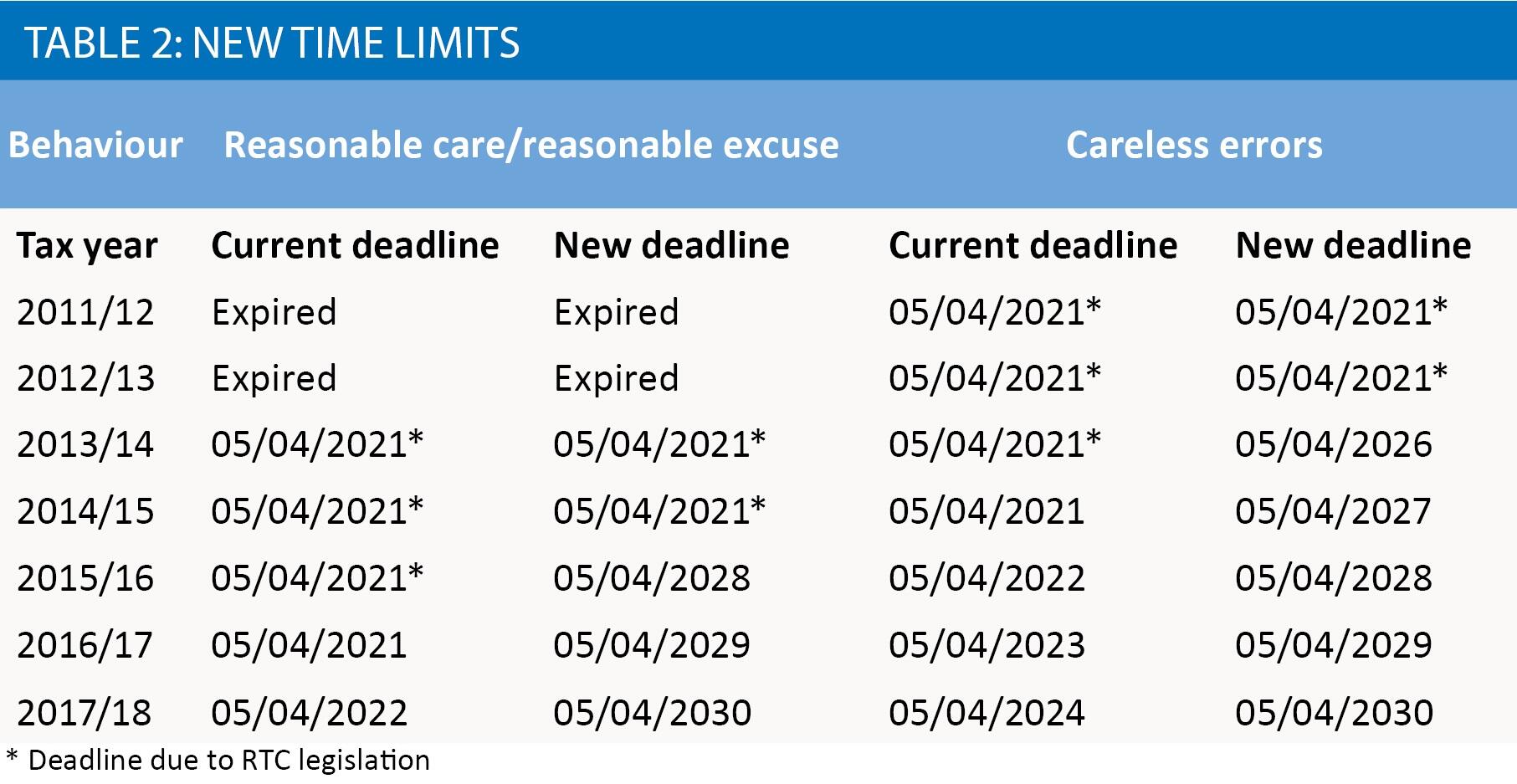

The draft legislation overlaps with the frozen time limits caused by the RTC as explained above. Table 2 shows how current income tax and CGT assessment time limits may be extended if the criteria in the draft legislation are met.

As you can see, some taxpayers who behaved ‘innocently’ (i.e. took reasonable care) in relation to their tax affairs are likely to feel particularly hard done by after 5 April 2021, when they could be assessed to additional tax up to 12 years after the end of the tax year, instead of the current four year limit: a significant change.

After 5 April 2021 HMRC and advisers will need to carefully check to ensure the appropriate time limit is being used where discovery assessments are issued.

This will involve checking whether the criteria for discovery assessments are met and establishing:

- the behaviour causing the under-assessment or excessive claim;

-

whether the ‘offshore matters’ or ‘offshore transfers’ test set out in this legislation are met;

- whether the criteria for using the 12 year time limit were satisfied.

Evidence will be important as it is probable that some cases will be considered by the Tribunals.

What else should be considered?

Despite the extension of assessment time limits for cases where taxpayers took reasonable care or had a reasonable excuse, HMRC is not planning to alter the existing six-year record keeping requirements.

Consequently, advisers will need to consider retaining their records for at least 12 years (possibly longer if enquiries or investigations are ongoing at expiry of the 12-year assessment time limit) and encouraging clients to do likewise. This may be crucial in order to retain sufficient evidence to defend against incorrect discovery assessments, given the burden of proof and the new time limits.

Failure to Correct (FTC) sanctions

Those taxpayers who failed to correct their UK tax position in relation to offshore non-compliance for the years to 5 April 2016 under the RTC, regardless of unresolved ongoing enquiries, may face FTC sanctions. FTC sanctions apply where the person did not have a reasonable excuse for failing to correct. FTC penalties are 100-300% of the tax. In addition, if a person did not meet the RTC’s requirements despite being aware that they had offshore tax non-compliance, HMRC may impose an additional penalty of up to 10% of the value of assets connected to the failure and publicly name the person as a tax defaulter. If a person has a reasonable excuse for FTC then HMRC will consider imposing tax-geared penalties (e.g. Sch 24 FA 2007, Sch 41 FA 2008 and Sch 55 FA 2009) instead.

HMRC sees the RTC as short-term encouragement to disclose and the 12 year extended time limit as providing long-term assistance for complex offshore investigations. The question is whether the additional tax being due because of this extended time limit coupled with tax-geared penalties will deter some unprompted disclosures. The answer probably depends on taxpayers’ personal views of factors such as whether HMRC is likely to find them or the likelihood of bankruptcy. However, the strict liability criminal offences do not require HMRC to demonstrate intent to evade tax so these and individuals’ general desire to not leave unresolved issues ‘hanging’ may provide the impetus for voluntary disclosures to continue.