The in-house perspective

Share this article

Tom Churton asks how tax departments can use technology to improve their processes and prepare for the future

Key Points

What is the issue?

As well as enabling tax departments to do more with less, tax technology is also seen by governments as the best way to narrow the so-called ‘tax gap’ by eliminating avoidable errors.

What does it mean to me?

Corporate groups need to be aware not only of the legislative requirements in relation to the use of tax technology, but also the benefits that additional technology could give. The first thing to do is prepare a ‘tax technology roadmap’.

What can I take away?

When looking at the tools available – including machine learning, tax chatbots and data flow tools – it is essential to refer back to the tax technology roadmap you have developed. Make sure you pick a tool that is going to do something that your group actually values.

Tax technology is increasingly seen as the answer for how tax departments can do more with less. It is also seen by governments as the best way to narrow the so-called ‘tax gap’ by eliminating avoidable errors (which are estimated to represent 30% of that gap in the UK). However, the term itself covers a wide range of issues, and given all the talk these days about big data, robotic process automation, artificial intelligence (AI), taxologists, etc., it is no surprise that in-house tax practitioners like me can feel confused.

The increased availability of technology has led to many questions among tax practitioners. Are we not doing our job properly if we don’t have five robots in the tax team? Can we really afford a tax technology manager, given that we only have 1.5 FTEs in Group Tax? What tools are out there and are they going to actually help us? What do I need to do to better advise the business? What will my job look like in 10 years’ time? If any of these questions resonate with you, hopefully I can provide some guidance in this article.

Tax technology roadmaps

When you start to think what your company or group can do in the technology space, the first thing to do is to prepare a ‘tax technology roadmap’. This is a document setting out your group’s goals in relation to tax technology. When you know your goals, you can come up with strategies for how to get there. Then, when you convert those strategies into actions, you have created a roadmap. In preparing a roadmap there are various things you should consider, such as:

- What is the current quality of financial data that is used in your tax processes?

- What software does your group currently use in its financial and tax processes?

- What is the business doing with its finance function (e.g. is it to be outsourced, in-sourced, transferred to shared service centres, etc.)? Finance may be undergoing its own transformation, so you should align with that.

- What would the ‘perfect’ tax reporting and tax compliance processes look like?

- What are the local tax requirements (e.g. Making Tax Digital in the UK), and what do you think those requirements will be in the next, say, five years?

- What tools are available to get you from where you are now to where you want to be (or are legally required to be) in the future?

If you have not yet prepared a tax technology roadmap, do not worry. You are definitely in the majority. But now is a good time to start thinking along these lines, as the tax world is moving in this direction already.

It is important to add that you should not prepare a technology roadmap in isolation. This must be prepared in collaboration with the finance team and IT. In addition, it has to sit in line with the overall objectives for the tax team. (For example, are you going to continue to do compliance or look to outsource it?)

Quality of financial data

The first step on any roadmap is to consider and, where necessary, improve the quality of financial data. Good data is data that can be analysed straight away as it has all the information needed already.

Poor quality data includes:

- unhelpful descriptions (e.g. ‘Invoice 1012’ or even none at all);

- incorrect postings, particularly where tax-sensitive data is posted in a non-tax sensitive account; and

- numerous contras, particularly where they don’t obviously cancel out (e.g. DR 400 and DR 100 contra with CR 500).

Where a group has poor quality financial data, the tax professionals preparing the tax returns are likely to be spending most of their time processing that data before they can start analysing it. This is clearly very inefficient and can be morale sapping for the individual concerned.

A data quality review involves a detailed review of precisely where the tax data comes from. You need to determine how the finance team processes invoices, and how all other journals (particularly month-end provisions) are determined and put into the financial system. This involves a thorough review of the end-to-end financial processes. When you understand the entire process, you can work out which bits need to improve.

This cannot be a tax-only work stream. The finance function will need to implement the process change. They too will benefit from better quality data, as they will have fewer queries from the tax team and have better information for making business decisions. This is not a ‘nice to have’ but will be a legal requirement in the not too distant future. Given that it may be a big task to improve the data, it is worth starting now rather than waiting for when the legislation comes in. In some countries, such as Spain, that legislation has come in extremely quickly, so it is better to be prepared in advance.

You may well find that the tax data is already available in other parts of the financial or purchase systems or in other databases used by the group. By linking systems together, you will quickly see an improvement in the data. But where you are not so lucky, there is a three-step process to go through once you know how you want to change the financial processes:

- Train the data inputters. A process of constant education is required to ensure the necessary culture change is embedded.

- Monitor the processes involved.

- Give feedback as necessary to improve performance.

The goal here is to get the data ‘right first time’. You must remember that real-time reporting will not allow any time to process the data.

One final thought for this area – keep it simple. If you can simplify the financial processes, it is far more likely that people will follow them, and keep following them after staff changes. If you design a process with the end user in mind, you cannot go far wrong.

Tax technology tools available

Armed with good quality financial data, you can start using the various tools available:

- Traditional tools: These include spreadsheets or software that prepares tax computations and returns. While these may be well-known and use existing technology, they should not be forgotten.

- Machine learning (ML) and AI: These tools analyse and categorise data. For example, they will take a spreadsheet of legal and professional fees with thousands of lines and analyse the descriptions to say whether the fees are deductible.

- Robotic process automation (RPA): These are tools that will perform any repetitive task. If you can write down a process as a series of steps (which can involve multiple programmes), then this is a good candidate for RPA. One example might be checking the VAT reference of a supplier by going to the relevant website.

- Analyse your data and produce dashboards: Tools that do this will show key metrics you are interested in, such as the effective tax rate for each country.

- Tax ‘chatbots’: Chatbots offer assistance to website users. A tax chatbot should provide answers to tax questions. For example, the chatbot could help finance teams to determine the correct VAT coding for an invoice, or help employees to code expenses correctly. This can save hundreds of phone calls to the tax team asking for the same information.

- Data flow tools: These can be used to collate responses received from around the group. They could be used for CbCR data collection, cash tax reporting, etc.

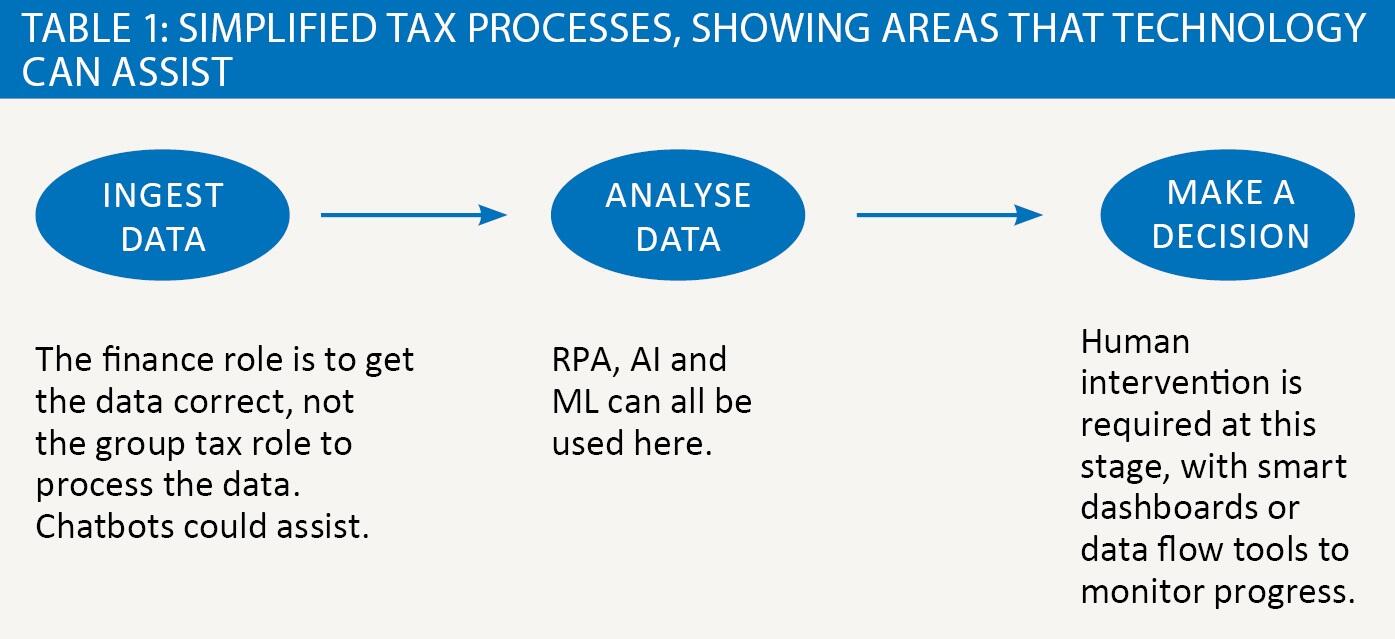

Table 1 below shows a much simplified tax compliance process, outlining the areas where tax technology might be able to assist. Some good advice I have received in this area is that if you are struggling to prove a business case for a significant technology cost, then pick a small task that can be automated. Estimating in advance the cost savings arising from using tools is hard but it’s much easier to show the results from something actually implemented. Doing something small (and easier to get approval for), can demonstrate the benefit and enable you to extrapolate to the potential benefit from the larger project.

When looking at software tools it is essential to refer back to the tax technology roadmap. Make sure you pick a tool that is going to do something that your group actually values. In other words, start with the problem you are trying to solve and work backwards to see what tools there are. Do not buy a piece of software because it looks good and then start looking for things you can do with it!

My usual caveat applies here too – you should not be looking at tax technology tools in isolation. At a minimum, your IT team should be consulted and, if you are looking to plug new software into your group’s ERP system, you should be working with the finance team.

And finally, if you are using ML or AI tools, make sure you document how the tool gets to the answer it does. If HMRC query the tax treatment of an expense, it is not sufficient to tell them ‘the computer said so’. You need some governance in this area.

Keeping up with international developments

If your group operates in a number of different countries, one of the hardest aspects of tax technology is keeping up to date with the requirements of different tax jurisdictions, i.e. the local equivalents of MTD in the UK. Each country is doing different things in this area, so no one standard set of rules can be used to design the group’s ERP system. Groups have to work on a country by country basis and implement local ERP solutions. This is obviously more costly but is unfortunately the only way groups can make sure they comply with the rules in each country they operate in.

Knowing what the different rules are is another tricky aspect. I have found that talking to peers in industry (who work in similarly large groups) is one of the best ways to do this. In addition, you need to make sure that each local finance team is aware of this issue and is seeking to independently keep up to date with this requirement (as well as all other local tax law changes).

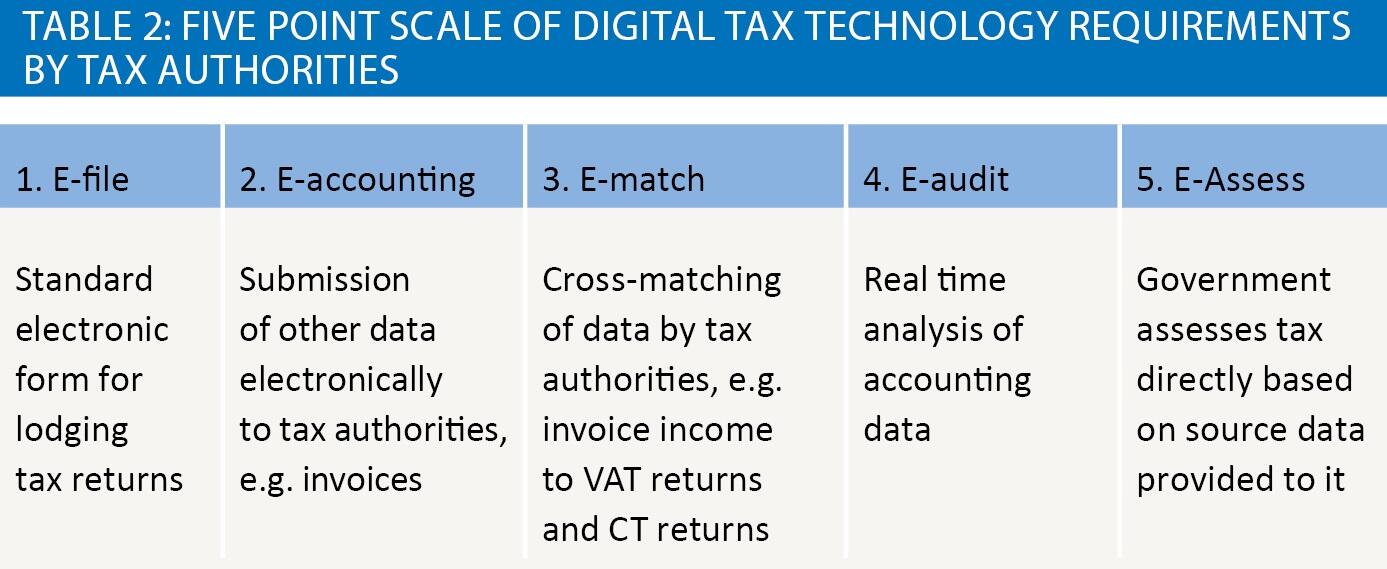

The developments internationally broadly fall into a five point scale as represented in Table 2. Countries are moving up the scale from E-file to E-assess at differing speeds, but the direction is always from left to right. I am not aware of a country that has gone the other way.

Using the UK as an example, MDT for VAT is at stage 1 as it is currently merely the electronic lodgement of a VAT return. A number of other countries, more recently India and China, have gone to level 2 with their recent requirements in relation to invoices. Russia is already at level 5 and reaping significant benefits in reducing tax evasion. The general rule here is that the older the tax system, the longer it will take to change the systems for both the tax authorities and the taxpayers, so the longer it will take to move along the scale. It is clearly much easier for a country which brings in a tax system to ensure it is a technologically-advanced system from the start.

What will we be doing in 10 years’ time?

I don’t have a crystal ball. However, the direction of travel does seem to lead to a consistent future. In the UK, we now have MTD for VAT. HMRC has repeatedly said that MTD for CT (and other taxes) will follow. It seems reasonable to assume at some stage in the not too distant future that HMRC (and all other tax authorities) will have access to groups’ underlying financial systems (level 4 in my chart). The tax authorities may even prepare our tax returns for us (level 5), leaving the in-house tax team to audit the tax returns prepared by the tax authorities.

I think that technology is not going to replace the in-house tax team, but will instead change our roles. We will need to be closer to the business than ever before, providing real-time advice. This will include checking the financial systems and making sure that invoices (on the accounts receivable and accounts payable side) are coded correctly. There will be no time to correct a miscoding or to add better descriptions to a journal entry, as the tax authorities will have access to the systems immediately. Getting the financial data ‘right first time’ will be an essential part of our role.

The advance of tax technology is already having an impact on the composition of tax departments of the largest corporate groups. These groups are tending to include a tax technology director. This may not mean an increase in the size of the tax department, as efficiency savings from the use of the technology may have enabled a reduction in the size of the compliance team.

Smaller teams are less likely to have the budget for an employee wholly devoted to technology, so need to consider training up one (or more) of their team in this area. This addition to their workload would be compensated for by the saving in time on compliance, as their processes get more efficient.

Group tax will be a proactive facilitator of the businesses that we work for, rather than a reactive in-house service provider. To me, this is an exciting future and one to be embraced not feared. Technology will be enhancing our roles, not replacing them.