Tidying your group structure to eliminate unnecessary holding structures and dormant companies

Share this article

Group structures can grow over time to include unnecessary holding structures and dormant companies. Taking the time to eliminate or move entities can bring significant savings.

Key Points

What is the issue?

The older and more acquisitive a group is, the more unwieldy its group structure is likely to be. This is likely to already be costing money and management time, but the amount of compliance coming down the tracks is only going to increase.

What does it mean for me?

Now is therefore a very opportune time to look at your structure and consider if you have the right companies and if they are in the right places.

What can I take away?

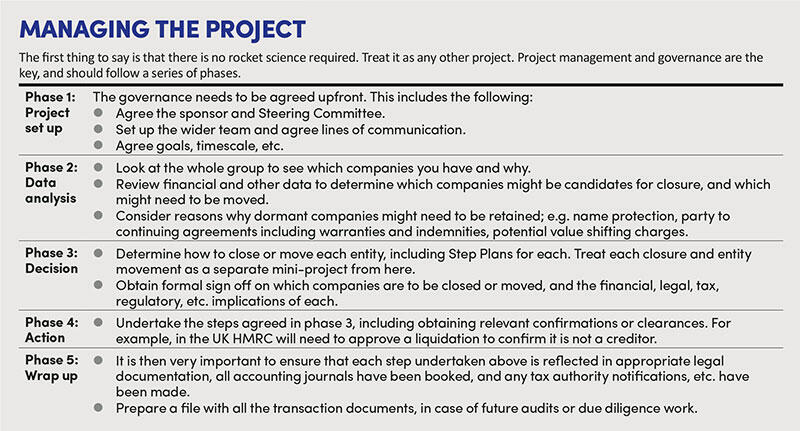

Once you know which entities you want to close and to move, you need to consider the options for doing this and how to manage the project.

Group structures grow over time, particularly in acquisitive groups. Holding structures which previously had a purpose may be inappropriate or unnecessary now. And previously trading companies may have become dormant. I liken it to the attic at home: things just accumulate over time, and every now and then you need to put some time aside to clear it out.

Many groups know when they have too many companies or inefficient holding structures. So why don’t they sort them out? Often, this type of project is put on the ‘To do’ list of a member of the Group Tax or Group Legal teams. But those lists are already full, and so this project can sink to the bottom of the ‘nice to do’ pile. After a few years, very little may have happened. From my discussions with large groups, this is a common issue: after all, who has spare capacity to pick up this project?

In this article, I will firstly discuss why now is a good time to undertake this project, and secondly offer a way for groups to do this, either themselves or with external assistance. A number of FTSE 100 groups (and equivalents) have already started on this task.

The benefit of tidying up your group

A number of cost savings can be generated from removing redundant companies or tidying up redundant holding structures – and the sooner you start the project, the sooner you will be able to lock in the annual savings. There are also important governance aspects to this. Indeed, I have heard an increasing call from CFOs to understand why their group structures are as they are. A useful rule of thumb is that a dormant company costs between £5,000 and £10,000 per year in external costs and internal management time. While this may not sound a lot, if you are removing a significant number of entities that soon becomes a noticeable annual saving. And that is before you consider the governance benefits which are harder to quantify but equally as important.

Depending on the history of each company, it is quite possible that capital losses may arise from closing dormant entities. This may or may not be of benefit to a group, given the limited number of assets that can now give rise to a chargeable gain. But it could be a further factor for some groups.

Why should groups do this now?

There are two significant potential pieces of legislation on the horizon: firstly, the EU’s Anti-Tax Avoidance Directive III (ATAD 3); and secondly BEPS 2.0, and in particular Pillar 2.

ATAD 3

Much has been written about ATAD 3 in the recent past so I won’t dwell on it here. Suffice to say that this will at a minimum have a reporting impact, and potentially a tax cost impact, for groups which have affected structures. Groups would be well advised to consider their current structures to determine if they might be impacted by the rules should they come in as proposed on 1 January 2024. This timeline also gives just over a year to restructure the group, or put in the additional substance that is needed to satisfy the tests in ATAD 3.

Pillar 2

BEPS 2.0 is also a much discussed phenomenon, so all I will say on the subject is that Pillar 2 is going to cause a massive compliance headache for all groups, and a tax cost for some groups. Minimising the number of entities in the group will help reduce the compliance burden. Having the retained companies in the right place in the structure may also reduce tax arising under Pillar 2.

Like ATAD 3, Pillar 2 is a proposed piece of legislation with an uncertain global timeline, but a 1 January 2024 start date seems a realistic proposition at least in the UK and EU. In some ways, however, the rules are already active, as some intragroup reorganisations (such as may be involved in your legal entity reorganisation project) will have a Pillar 2 impact due to the transition rules. This needs to be factored into your thoughts for the project.

Ways to eliminate or move entities

A project like this can be run internally, and I am aware of two groups which have done so very successfully. The key is to have a dedicated resource to manage the project. They can then build a team involving legal, company secretarial, finance, tax and others as necessary.

Alternatively, if a project manager cannot be found internally, this resource can be hired externally. When looking externally, an important factor is cost: does the cost of the project exceed the annual savings? In my experience, a one-year pay back is normally acceptable. If the goal is to close 50 entities, the annual saving is approximately £250,000 to £500,000, so a project cost of £250,000 would often be acceptable. Once you know which entities you want to close and to move, you need to consider the options for doing this. Each country has its own rules but essentially there are a few main options for closing an entity.

1. Deregistration

Deregistering (or dissolving) a company terminates its registration so it ceases to exist. In the UK, this requires a simple form (DS01) to be lodged with Companies House and is relatively quick. However, it does not give the directors the protection that a liquidation does (see below). Therefore, I have historically only deregistered a company which had never traded or been listed. Any assets held by a company that is deregistered in the UK become assets of the Crown (under the bona vacantia legal principle) so you will need to empty the balance sheet before deregistering the company.

As deregistering a company is often a simple process, it is a good way to start a larger project by banking a few ‘easy wins’ by deregistering already dormant entities. If you look at your group structure, you may find some companies with balance sheets showing net assets of, say, £1, representing an intercompany receivable. Such an entity does not require any pre-closure restructuring so could be an easy one to deregister (once you have checked its history to make sure there is no reason to keep it).

2. Liquidation

This is a more formal process than deregistering a company. In the UK, you need to appoint formal liquidators so there is a cost element, although the cost need not be high for a simple liquidation. Due to the formalities of the process, the company directors are protected from subsequent claims against them or the company, so it is a good idea to liquidate a company which has previously traded (or its shares or debt were publicly traded).

3. Merger

Some countries, but not the UK, allow a formal merger between two companies such that only one company exists afterwards. This can be a very quick and effective way to close entities.

4. Redomiciliation

Some countries allow a company to change its formal seat of incorporation. For example, a company set up in Country A can change its country of incorporation to Country B from a certain date. It then ceases to have any further legal or tax requirements in Country A. The UK is considering bringing in rules to allow companies to redomicile to the UK.

5. Changing tax residency

The tax residency of a company is determined by local tax law and can depend on the place of incorporation, the place of central management and control (i.e. where the board of directors meet) or the place of effective management and control (i.e. where local management works). While the place of incorporation is generally set (subject to redomiciliation), places of management and control are more fluid, particularly in the modern world. This could therefore be a good option to quickly, and potentially cheaply, remove a ‘tax haven’ company from a structure; i.e. by changing its directors to UK individuals and having them meet in the UK. While the tax haven entity would still exist, from a tax perspective it is now a UK resident company.

Summary

There are benefits to ensuring that a group structure has the right entities, and that they are in the right place. Project management and governance are the keys to a successful project. The project can be undertaken just like any other large project, and there are a number of legal processes that can assist in the project. The best advice is to start now so that you can bank the savings earlier. It is also often a good idea to pick some ‘easy wins’ first to gather momentum for the project.