How to achieve net zero: the practical issues faced by UK businesses and households

Share this article

We consider the practical issues that must be addressed to truly incentivise UK businesses and households to strive for net zero.

Key Points

What is the issue?

By Autumn 2023, HM Treasury should have a clear policy of how the tax system, its incentives and reliefs should be utilised to steer UK industry down the ‘green’, energy efficient and low carbon route.

What does it mean for me?

Both industry and the government regard tax policy, specifically capital allowances, as a key tool in achieving a low carbon Britain. Through freeports, and before them enterprise zones and enhanced capital allowances, the government has sought to enhance investment and change behaviours.

What can I take away?

A truly joined up approach to tax, energy and housing policy, consistently applied and set out over a long-term horizon, would surely help deliver a low carbon future for the UK by 2050, or preferably sooner.

The recently published Skidmore report, ‘Mission Zero’ – an independent review of net zero chaired by Rt Hon Chris Skidmore OBE MP – sets out the recommended actions for the UK to transition to its long stated aim of net zero greenhouse emissions by 2050 (see bit.ly/3o0yQO5).

The report repeatedly recommends reviewing the incentives for investment – both how HM Treasury incentivises decarbonisation via the tax system, and the range of capital allowances. By Autumn 2023, HM Treasury should have a clear policy of how the tax system, its incentives and reliefs should be utilised to steer UK industry down the ‘green’, energy efficient and low carbon route.

But it’s not just about being ‘green’. The report highlights the wider opportunities for growth, employment and economic prosperity that a low carbon UK could enjoy. The Office for National Statistics estimates the low carbon economy to have been worth £41.2 billion in 2020 (see bit.ly/3mH5EuN). There is a clear fiscal payback to the UK in leading the world through low carbon innovation and digital transformation.

Both industry and the government regard tax policy, specifically capital allowances, as a key tool in achieving a low carbon Britain. Through freeports, and before them enterprise zones and enhanced capital allowances, the government has sought to enhance investment and change behaviours.

The report also references a study from the National Institute of Economic and Social Research, which found that ‘corporate taxes reduce investment in tangible assets and R&D. Mission Zero states that it is important that the government ‘uses a balanced approach of tax incentives and disincentives to encourage economic activity that meets the dual objectives of growth and decarbonisation’.

Super-deductions

Skidmore considers the 130% accelerated capital allowances (and 50% special rate first year allowances) introduced from 1 April 2021 to 31 March 2023 for companies investing in qualifying new plant and machinery assets to have been about ‘driving investment’, as opposed to discouraging corporate delay in investment due to the then anticipated (and now confirmed) corporation tax main rate of 25%. Albeit first year allowances clearly reward greater investment with immediate and accelerated tax relief.

However, super-deductions finished on 31 March 2023 and were only available to UK corporate taxpayers, with the result that those operating as individuals or through partnerships – such as GP surgeries, architects or even tax advisers – were unable to benefit.

In the Budget, the Chancellor announced full expensing for three years. Companies incurring qualifying expenditure on new plant and machinery before 1 April 2026 will be able to claim either a 100% first year allowance for main rate expenditure (known as full expensing) or 50% for special rate expenditure, including lifelong assets. The Chancellor stated an ambition to make full expensing permanent. He also confirmed that the annual investment allowance would be set permanently at £1 million per year.

Enhanced or 100% capital allowances should clearly encourage greater investment by businesses, and the OBR forecasts that this might encourage some 3% year on year growth in investment by UK business. However, the timescales for these changes remain a factor for consideration. With the ambition to achieve the ‘green’ goal of net zero by 2050, a coherent programme of enhanced tax reliefs that will be in place until (or beyond) that date remains something we can only wish for.

Large investment and capital projects – such as building a new factory, logistics centre or power station – take years to achieve. Businesses fail to factor short-term incentives into their business planning without longer-term certainty. The changes or improvements needed for net zero – energy efficiency, carbon reduction and sequestration, water and waste reduction – are largely driven by global multinational companies. Uncapped allowances, carefully targeted, would accelerate the impact these businesses have in the UK and elsewhere.

All too often in the recent past, polluting and environmentally dangerous activities have simply been ‘offshored’ to other countries that are less willing or able to enforce the necessary standards. Policy decisions on tax incentives should try to ensure that global targets are achieved and not simply relocated. Any accelerated tax relief to UK businesses (whether domestic or part of multinational corporations) should consider their wider supply chain and global actions so as to ‘ratify’ their eligibility for enhanced tax savings by consistent carbon improvements – wherever they operate. Additionally, the government has launched a consultation on a UK ‘carbon border adjustment mechanism’ as part of its net zero strategy to ensure fair competition across international standards and pricing of decarbonisation requirements.

Enhanced capital allowances

Between April 2001 and March 2020, 100% enhanced capital allowances were used to encourage taxpayers to invest initially in energy efficient assets, and later also in water efficient technologies, including heating, ventilation and air conditioning (HVAC) systems, lighting and pumps. However, the complicated requirements for manufacturers to pre-register and prove their efficiency credentials against constantly evolving criteria made for a confusing and difficult regime that significantly under achieved its potential.

Linking tax incentives to independent gradings

A new programme of enhanced capital allowances targeted at ‘low carbon’ or ‘net zero’ technologies should have a recognisable metric linked to the outcome achieved. As I have previously written about in Tax Adviser (see ‘Integral to investment’ (December 2018)), linking the rate of writing down allowances to the building’s energy rating or design performance should result in a clearer and ‘independent’ classification or rating.

Within the real estate sector, a number of different standards have sought to drive ever-increasing energy efficiency, including the Minimum Energy Efficiency Standards (MEES), British/European and International Standards (BS:EN:ISO), Energy Performance Certificates (EPC) and Display Energy Certificates. Building Regulations Part L has been a stalwart of UK building design but many consider that it has not kept pace with technology, and was never really designed to measure building performance.

However, other programmes use a system of ratings. BREEAM (the Building Research Establishment Environmental Assessment Method) (see bit.ly/3zSCnB2) ranks buildings from Pass (one star) to Outstanding (five stars) and provides an interim certificate against design criteria and full certification following a post construction review. NABERS (the National Australian Built Environment Rating System) is gaining significant momentum in the UK for commercial offices, using a ranking system from one star ‘making a start’ to six stars for ‘market leading’. NABERS also requires annual monitoring to maintain and facilitate incremental improvement as subsequent works are undertaken.

The rating systems could be linked to accelerated writing down allowances. Projects that achieve assessments four stars with BREEAM or five stars with NABERS could be given, say, a 40% first year allowance, while those achieving top ranking could be given 60%.

Independent gradings could also be utilised to grant business rates relief; for example, giving enhanced reductions to buildings that improve their rating following a refurbishment project. Tax incentives would encourage both landlords and occupiers to ensure that old legacy properties are modernised with the most efficient and low carbon technologies.

Tightening regulations

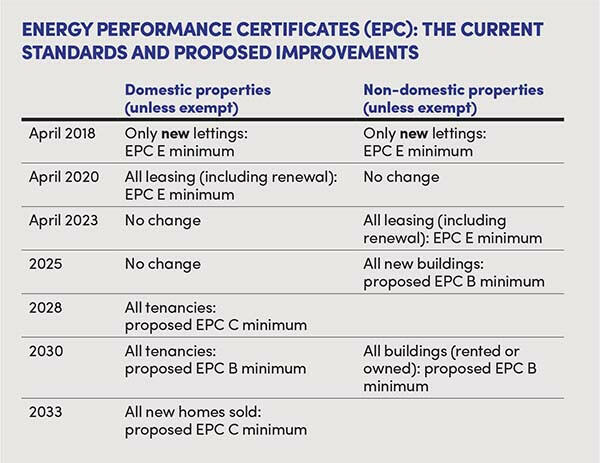

The MEES regulations are continually tightening the requirements for the minimum energy efficiency ratings for both domestic (residential) and non-domestic (commercial) properties.

Since 2018, restrictions have applied to new leases if an EPC certificate is graded F or G (although landlords have been able to extend existing leases). However, Skidmore is encouraging the government to legislate by 2025 for all existing (legacy) non-domestic buildings, both rented and owned, to be EPC B by 2030. It should also require all new buildings from 2025 to have a minimum EPC B rating. As a surveyor, part of me wonders at the practicality of all buildings achieving ever improved energy ratings, irrespective of use.

Various surveys have found that many commercial landlords are unaware of these changes, while others are simply slow to improve their properties. However, all those with EPC grades of F or G (estimated to be 18% of all commercial properties) are no longer legally lettable since 1 April 2023, unless the property is exempt. They will either have to sell or undertake energy and insulation improvements to obtain a higher EPC certificate before any continued rental is possible. Where the landlord is a UK taxpayer, much of the necessary improvement works will typically benefit from capital allowances relief, helping to ease the overall cost.

Freeports

Freeports (known as ‘green freeports’ in Scotland) are designated geographic areas that have a range of fiscal incentives to encourage development and growth within the freeport and its immediate vicinity.

The English freeports came into full effect between November 2021 and July 2022, following extensive consultation. They benefit from reduced employment costs through employer national insurance savings, lower business rates and stamp duty land tax, and simplified customs and planning requirements.

They also receive boosted capital allowances. Structures and buildings allowances are accelerated to 10% per annum (instead of the default 3%), and plant and machinery benefits from a 100% first year allowance (a new interation of enhanced capital allowances!). These are intended to give the owner or investors a faster return against their investment in developing these zones. Few ‘green’ criteria have been explicitly factored into the legislation, though was a condition of the relevant Scottish applications.

Unfortunately, the biggest issue freeports face – including, currently, the Scottish green freeports and the two new freeports in Wales (announced in March 2023) – is that these boosted allowances are dependent upon the buildings being brought into use before, or expenditure incurred by, 30 September 2026 respectively.

Investment zones

Also confirmed in the Spring Budget was the creation of 12 new investment zones across the UK – with eight to be England and the remaining four in Scotland, Wales and Northern Ireland.

These investment zones are designed to harness local strengths to drive productivity and leverage the bottom-up local talent, knowledge and networks to deliver sustainable growth that benefits local communities. They are to be rooted in partnership between central and local government, research institutions (universities) and the private sector, in order to realise the potential of our cities and regions. Additionally, the government’s prospectus identifies five priority sectors: digital and technology; green industries; life sciences; advanced manufacturing; and creative industries.

Whilst most of the fiscal incentives are similar to freeports, the individual investment zones will receive total funding of £80 million over five years. The investment zones can use this funding flexibly between spending and a single five-year tax offer, scalable based on number of sites. This would consist of:

- £35 million flexible spend, split 40:60 between resource spending (RDEL) and capital spending (CDEL), to use across a portfolio of interventions based on the opportunities of each cluster; and

- tax incentives, which can cover up to 600 hectares across up to three sites, lasting for five years. Where places do not opt for the maximum tax offer of 600 hectares, tax incentives can be exchanged for a greater amount of spend.

Legacy housing stock

New design standards must drive through changes to new buildings being constructed to reduce both their own carbon footprint and the embodied carbon throughout the relevant manufacturing and supply chains. However, the MEES regulations and EPC requirements (as set out above) also aim to address the vast legacy portfolio of existing properties (both residential and commercial).

The Construction Products Association stated in their evidence to Skidmore it supports the proposal for the creation of a Retrofit Hub to be supported by industry and government and Innovate UK, hoping that this could provide technical, scientific and business focus.

Suez R&R UK Limited commented that ‘policy and regulation in this area is incomplete, and often has a record of inconsistent application and maintenance which undermines both investment … and fails to consistently reinforce communications and messages that are required to change behaviour in general’.

One example of this is the current VAT regime on energy saving materials (ESM). Since April 2022, a temporary zero VAT rate applies to a wide range of energy and insulation improvements. However, there is no just and reasonable apportionment where the ESM works are undertaken within a wider refurbishment project as a ‘single supply’. This restrictive approach completely undermines the stated policy ambition to incentivise the take-up of ESMs in line with the government’s net zero objectives.

However, the recent Budget publications included a consultation on ESM and how these could be improved ending 31 May 2023.

In conclusion

Bold and long-term tax incentives, clear unequivocal capital allowances and targeted first year allowances could help change our attitudes and behaviours to achieve net zero carbon emissions. A truly joined up approach to tax, energy and housing policy, consistently applied and set out over a long-term horizon, would surely help deliver a low carbon future for the UK by 2050, or preferably sooner.