Integral to investment

Share this article

Alun Oliver provides an overview of the capital allowances changes in the recent Budget

Key Points

What is the issue?

Capital allowances (CAs) have changed considerably with the introduction of SBAs and changes to Annual Investment Allowances (AIAs), Special Rate Pool and Electric Vehicle Charge Points and the withdrawal of Enhanced Capital Allowances (ECAs).

What does it mean to me?

These changes are designed to encourage immediate investment – perhaps seeking a ‘BREXIT bounce’ in growth and productivity, particularly over the next two years where the boosted AIAs will result in immediate 100% relief on most expenditure up to approximately £5m in the year incurred.

What can I take away?

Businesses that are planning new capital expenditure over the next few years may wish to consider altering the project timing (where possible) to seek to optimise the tax savings generated from allowances – in light of these recent changes.

Further to the Office of Tax Simplification review of Capital Allowances and the recent Budget statement by Philip Hammond MP, capital allowances are clearly considered an integral component of UK tax. Finance (No.3) Bill 2018 (FBNo3) and draft legislation, only sets out the basics of these measures with further consultation on the new Structures & Buildings Allowance (SBAs) to refine the announcements into fully operational tax legislation. This was a ‘giving’ budget setting out the Chancellor’s ambition to encourage businesses to spend, and spend now!

Capital allowances (CAs) have changed considerably with the introduction of SBAs and changes to Annual Investment Allowances (AIAs), Special Rate Pool and Electric Vehicle Charge Points and the withdrawal of Enhanced Capital Allowances (ECAs).

Businesses that are planning new capital expenditure over the next few years may wish to consider altering the project timing (where possible) to seek to optimise the tax savings generated from allowances – in light of these recent changes.

Annual investment allowances (AIAs)

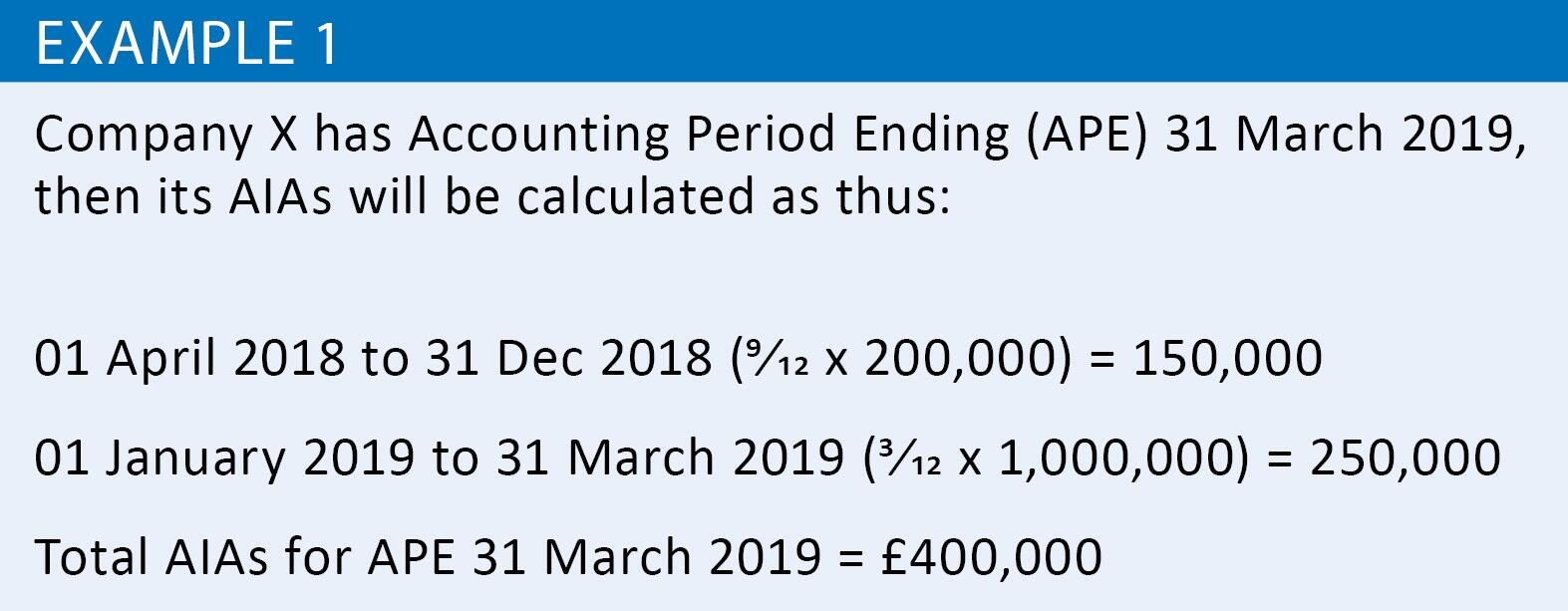

Nicknamed the ‘yoyo allowance’, the Government is increasing the cap on AIAs to £1m of qualifying expenditure from 01 January 2019 for two years. As before, calculators will be required for all those with accounting periods spanning the step up, or reversion to £200,000 after 31 December 2020. See example 1.

Structures & buildings allowances (SBAs)

SBAs are to be given at 2% for 50 years on eligible construction costs incurred on or after 29 October 2018 (effective date) for new non-residential structures and buildings. The HMRC Budget Technical Note describes SBAs as ‘a long term commitment to improving the competitiveness of the UK as a destination for investment’. The Red Book stated that the introduction ‘addresses a significant gap in the UK’s current capital allowances regime’. The rules are not yet fully formed and some aspects still need fathoming out – the consultation runs to 31 January 2019.

Commencement

The Government is to use Statutory Instruments to introduce legislation, claiming this facilitates rapid introduction ‘to provide taxpayers with certainty’. The cynic in me wonders if the increasing trend of SIs, is more because there is considerably less consultation and scrutiny than the traditional path of primary tax legislation.

SBAs apply to new expenditure on commercial structures and buildings where all the contracts for the physical construction works (including any preparatory works) are made in writing and are entered into by the parties on or after the effective date. Renovation and alteration of existing buildings will also be included, as will purchases of a new structures or buildings directly from the developer – subject to the contracts and physical construction works having been entered into on or after Budget day. There are certainly similarities to the ‘old IBA’ regime; but certain changes and restrictions may counteract any simplification!

Taxpayers undertaking their own construction activity can also claim SBAs, but will need to keep documentary evidence of the physical construction and contract dates being compliant.

Anti-avoidance

Those embarking on recently commenced projects may feel aggrieved by this radical change – there would always be winners and losers whatever active date were used. However it should be noted, the Government intends to include punitive anti-avoidance measures that will deny all SBAs where contracts are withdrawn, revoked or replaced by a later dated contract. Although one wonders how easily HMRC can adequately police this?

Large regeneration schemes undertaken under frameworks or call-off arrangements may need to carefully review the SBA legislation to ensure they are not denied SBAs under an existing contract.

As with VAT, the scheduling of the works may also become more important – demolition and site clearance undertaken together with the main build contract will be eligible for SBAs, but if divided by considerable time or even discrete contracts then these preparatory works will not qualify.

Key elements

The old IBA basis (4% for 25 years) may have been more helpful, both in terms of cash flow, but also record keeping – given the majority of typical lease terms are 25 years or less. However, SBAs will be given on new commercial structures and buildings expenditure, including costs for new conversions or renovations from the date the asset is brought into use for a qualifying activity.

What qualifies? All the costs associated with the physical creation of the asset – including costs of demolition or land alterations necessary for construction, and direct costs required to bring the asset into existence. Expenditure on acquisition of, or rights over, land (including SDLT and legal fees) in common with all other allowances is not eligible, nor are the costs of obtaining planning permission. The claimant must have an interest in the land upon which the structure or building is constructed. There will be rules to prevent leases being used to give more than one party separate interests in the same structure or building.

A subsequent disposal will not trigger a balancing allowance – instead, the purchaser simply takes over the remaining allowances and continues to write them down over the remaining part of the original 50 year period. Thus there is no requirement to recalculate for a new period, other than apportionment for part periods.

Purchases new and unused from a developer will require a ‘just and reasonable apportionment’ to segregate the value of land from the acquisition costs, that would otherwise be eligible for SBAs, and presumably other eligible capital allowances as may be appropriate to the asset – highlighting the need for specialist assessment of project costs.

Interaction with other CAs

Expenditure eligible for Plant & Machinery Allowances (PMAs) and Integral Feature Allowances (IFAs) will continue to be eligible for these reliefs and thus are ineligible for SBAs. Previous IBA rules, gave taxpayers the choice on which to claim. Additionally SBAs expenditure will not qualify for AIAs. Hence for tax payers to benefit from all of the available capital allowances relief and truly optimise their tax savings, they will need to undertake segregation analysis of the project expenditure into the various forms of allowances relevant – PMAs, IFAs, AIAs, Long Life Assets (LLAs), SBAs and, until their abolition, ECAs.

However, an example purchase from a developer in the Technical Note makes no reference to PMAs or IFAs and assesses SBAs as available on the purchase costs less land value. I expect that this illustrative position ignores PMA/IFAs and AIAs for simplicity’s sake only and does not represent a more radical denial of these other allowances on second-hand transactions?

Furthermore, SBAs are not available against any costs deductible in calculating profits chargeable to tax, such as land remediation relief, or repairs and maintenance expenditure.

Structures are explicitly stated as including ‘walls, bridges, tunnels’ and FBNo3 references ‘highways’ but there is no mention of railways, piers, dams or similar utility and infrastructure assets. With any luck the legislation will not seek to limit structures or buildings from these sectors by some anachronistic schedule of qualifying assets/uses.

Dwellings

HMRC’s Technical Note advises that ‘expenditure on residential property and other buildings that function as dwellings’ will not qualify for SBAs. It further defines ‘dwellings’ as buildings primarily intended or used for long-term residence; including university or school accommodation, military accommodation and prisons. Given the requirement to increase the UK housing levels and encourage greater participation in the Private Rented Sector these restrictions seem outdated to current housing needs and trends. Hopefully the consultation will help find a balance to facilitate relief on residential dwellings on a ‘commercial scale’ – as why should this sector be any different from a care home, or hotel?

The current schedule of ‘Qualifying Activities’ has been pared down from those set out in s.15 CAA2001 and the FBNo3 excludes certain prescribed ‘holiday or overnight accommodation’. Thus it would appear that Furnished Holiday Letting (FHLs) are to be denied SBAs – whilst still eligible for other forms of allowances. True simplification would not seek to ‘carve out’ different qualifying activities, forcing more segregation of different uses and allowances!

Live/work premises are to be excluded and mixed use properties will also require a ‘just and reasonable apportionment’ albeit shared/dual use will be treated as non-qualifying – again in contrast to the treatment for PMAs, IFAs and AIAs within common areas. Lastly where the proportion of a mixed use property has 10% or less of the costs that could potentially be eligible for SBAs then none would be permitted.

Non qualifying activity

Where the property/asset has a non-qualifying change of use – say it becomes a dwelling, or is acquired by a non-taxpayer, such as a pension fund – then the associated 2% reliefs each year are lost, and not carried forward or recalculated.

Crown, Local Authority or properties developed by charities/pension funds after the effective date will not benefit from SBAs directly, but must retain some evidential records as to the start date etc. of the notional 50 year period – if subsequent taxpayer purchasers are to benefit from SBAs on the remaining period. Given our experience in operating the ‘New Fixtures Rules’ on second hand purchases this ‘record keeping’ could be a problematic area; effectively denying claims to buyers if there are not sufficient records.

SBAs will continue where the asset is damaged by fire or otherwise becomes incapable of qualifying use. Temporary disuse for two (five in exceptional circumstances) years, will not deny SBAs to the owner, until the building or structure is brought back into use. The new construction expenditure (net of any insurance proceeds etc.) will qualify for SBAs in its own right with a new 50 year period.

Leasing & CGT

Tax simplifications are rarely that. Here this simplified capital allowance on a straight line for 50 years without balancing adjustments – introduces new Capital Gains Tax (CGT) changes and complex measures for leasing – attempting to deny relief in abusive avoidance situations.

In simple terms, normal assessment of each taxpayer’s respective positions will prevail; so a lease on full market rent, with no premium, would leave the SBAs with the lessor’s property investment business. Whilst a very long lease (say 999 years) at a token ‘peppercorn’ rent and with a significant capital, a premium will be treated as akin to a sale and the lessee becomes entitled to the SBAs.

Between these two ‘end markers’ the complexity of lease transactions and potential for abuse has led to the Government setting out two tests – firstly where the premium paid is 75% or more of the sum of the capital amount and the value of the retained interest, then the lessee will have the SBAs as a deemed sale. A capital sum of less than 75% and the SBAs will be retained by the lessor. Secondly, where the term of the lease is not more than 35 years, then the SBAs are to stay with the lessor.

Capital allowances rarely interact with CGT other than disposals in a loss situation. However, the new SBAs rules propose that the taxpayer’s base cost will be reduced by the total value of SBAs claimed up to the point of sale. Given only a 2% per annum some investors may decide not to claim SBAs, rather than have to reduce their base costs on a later sale.

Special rate pool

FBNo3 clause 30 reduces the writing down allowances (WDAs) rate for the Special Rate Pool – covering IFAs, LLAs and Thermal Insulation works under s.28 CAA2001. This changes from 8% per annum on a reducing balance basis to 6% p.a. effective from 1/ 6 April 2019, except for ‘ring fenced trades’ which will remain at 10% WDAs.

Whilst clearly this reduction will slow the benefit of claiming IFAs, it is considered the AIA increase (and potential SBAs on wider project costs) will offset this for the majority of claimants.

Enhanced capital allowances (ECAs)

One of the more unexpected changes, was the announcement to end ECAs from April 2020. ECAs provide 100% First Year Allowances (FYAs) against assets that were on the Energy or Water Technology Lists, or otherwise meet the qualifying criteria.

ECAs work in tandem with the Minimum Energy Efficiency Standards (MEES Regulations) as part of the ‘carrot & stick’ approach of Government to get landlords to improve the energy efficiency of UK property stock. Whilst ECAs rules are not perfect, linking or adjusting the rate of WDA – by reference to either the property’s Energy Performance Certificate or BREEAM® rating (BRE’s Energy Assessment Methodology) – whereby the rate of WDAs could have been set at 100%, 75% or 50% depending upon the rating of the property – would have maintained a clear link to ensuring buildings became more energy/water efficient. In light of both the SBAs and £1m AIAs, this withdrawal will only impact a relatively modest group of taxpayers.

Electric vehicle charge points were given 100% FYA under s.38 FA(No2)2017 and effective from 23 November 2016 have also been extended to 31 March/5 April 2023.

Conclusion

These changes are designed to encourage immediate investment – perhaps seeking a ‘BREXIT bounce’ in growth and productivity, particularly over the next two years where the boosted AIAs will result in immediate 100% relief on most expenditure up to approximately £5m in the year incurred.

The new SBAs will further boost the tax savings from new commercial development, but the CGT changes and evidential requirements to maintain accurate records for up to 50 years on the construction costs and start date may prove to be too restrictive for many taxpayers to take seriously? These points need to be forcefully made during the consultations to see if a better balance could be struck – so as to achieve the Government ambition of continued investment in UK, without becoming too onerous and ultimately ineffectual – in their ambition to drive growth and economic prosperity.