How multiple trusts can reduce inheritance tax

Share this article

Multiple trusts were commonly used to reduce inheritance tax by minimising ten year and exit charges. We ask whether they are still worthwhile.

Key Points

Key Points

What is the issue?

Prior to 9 December 2014, a common device to minimise inheritance tax charges was the use of ‘pilot’ or multiple trusts. This did not avoid the entry charge but could minimise future ten year and exit charges.

What does it mean for me?

Following amendments, when calculating the rate of tax charged under the relevant property regime, the value of non-relevant property in the same or a related settlement is now excluded. This probably benefits some larger trusts and wealthier taxpayers.

What can I take away?

Given that there are still many trusts around that were set up and funded with same day additions before December 2014, it is sensible to avoid additions to such trusts by the settlor now.

One effect of the inheritance tax changes to trusts in Finance Act 2006 was that trusts within the ‘relevant property regime’ became much more common. Almost all property settled into trust in a donor’s lifetime is now relevant property unless the beneficiary is disabled. Whether the trust is discretionary or interest in possession is irrelevant.

Once in the relevant property regime, the trust is subject to inheritance tax charges of up to 6% every ten years and exit charges on trust distributions of capital. In addition, assets placed in trust which exceed the donor’s unused nil rate band are subject to a 20% entry charge on the excess value unless qualifying for an exemption such as business property relief.

The position before 9 December 2014

In the light of this, people sought to minimise the ten year and exit charges under the relevant property regime. Prior to 9 December 2014, a common device was the use of ‘pilot’ or multiple trusts. This did not avoid the entry charge but older readers will recall that it could minimise future ten year and exit charges. Following the changes in Finance (No 2) Act 2015, this was stopped; however, the use of multiple trusts can still prove advantageous for a number of tax and commercial reasons. In addition, practitioners need to understand the old regime and the changes in order to avoid ‘tainting’ protected pilot trusts set up before December 2014.

Before 10 December 2014, properties added by the settlor to several existing settlements on the same day avoided aggregation with each other, so that each settlement effectively had its own nil rate band when calculating the rate of tax on the ten year anniversary and on distributions, provided that the settlor had not used up their nil rate band on previous chargeable transfers.

The savings were limited to a maximum of 6% of £325,000 multiplied by the number of trusts used and were therefore less significant for very high value property but could be useful for lesser sums.

How did it work?

Typically, a number of pilot trusts would be established on different days, each with a nominal sum of say £10. Substantial assets were then subsequently added to each trust. It was essential that all such later additions occurred on the same day.

The reason lay in the inheritance tax relevant property charging rules at Inheritance Tax Act 1984 Part III Chapter III. This provided that in calculating the tax rate, where the settlor had added property to the settlement after it commenced, instead of taking into consideration the chargeable transfers of the settlor in the seven years before he created the settlement, his total chargeable transfers in the seven years before the addition were substituted if these were greater (Inheritance Tax Act 1984 s 67(3). However, the key point was that transfers on the same day as the addition were ignored.

Often the trusts had the same trustees, beneficiaries and trust powers but they would nevertheless be separate settlements for inheritance tax and trust law purposes. In Rysaffe Trustee Co (CI) Ltd v IRC [2003] EWCA Civ 536, HMRC failed in its attempt to tax five identical settlements as a single composite settlement under Inheritance Tax Act 1984 s 64. Mr Justice Park held in the High Court that ‘it is up to the settlor who places property in trust to determine whether he wishes to create one trust or several trusts, or for that matter merely to add more property to a settlement which had already been created in the past’. Each settlement was created by a separate ‘disposition’ within Inheritance Tax Act 1984 s 43. The claim that there was one settlement by associated operations was rejected by the Court of Appeal.

There were traps to watch: the technique could not be done by settling property into separate discretionary trusts set up in the will itself or varying the will. The trusts would all commence on death and be related trusts. There were also complications if the deceased had used up the nil rate band or left property on interest in possession trusts for the spouse or civil partner. But remember that the tax savings overall are limited to 6% of the nil rate bands multiplied by the number of trusts.

For GAAR purposes, although pilot trusts are clearly tax arrangements and involve contrived steps, HMRC accepted in the guidance that they were not to be challenged under the GAAR provisions even if done on or after 17 July 2013 because they accorded with established practice accepted by HMRC:

‘The practice was litigated in the case of Rysaffe Trustee v IRC. HMRC lost the case and having chosen not to change the legislation, must be taken to have accepted the practice.’

Of course, that guidance was issued in 2013 before the 2014 changes discussed below. Anyone seeking to circumvent the same day additions provisions now might well be caught by GAAR.

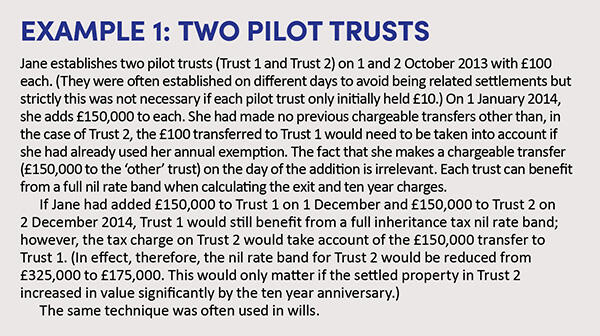

Image

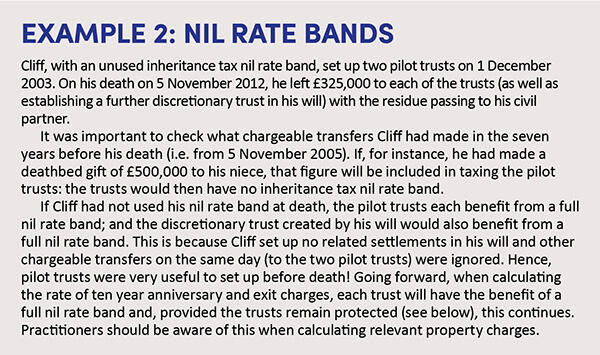

Image

The position from 10 December 2014

After three consultations between 2012 and 2014 aimed at simplifying the taxation of relevant property trusts, draft clauses were published in December 2014. These clauses (with significant revisions) became law in Finance (No.2) Act 2015 on 18 November 2015 but with anti-forestalling provisions from 10 December 2014. This consultation rather demonstrates the difficulty of reforming trusts in any meaningful way – the changes brought winners and losers!

The winners

From 18 November 2015, when calculating the rate of tax charged under the relevant property regime, the value of non-relevant property in the same or a related settlement is now excluded. Curiously, this probably benefits some larger trusts and wealthier taxpayers rather than those who were looking for relatively modest tax savings using multiple nil rate bands.

For example, the change is helpful for excluded property trusts (trusts set up by foreign domiciled settlors holding foreign situs property) where there is only a small amount of UK situated property which is relevant property. The rest of the property in the trust can now be ignored in calculating the rate of tax at the ten year anniversary and the UK property receives the full nil rate band.

It can also be useful where a pre-2006 trust has a mix of funds with qualifying (pre-22 March 2006) and non-qualifying (post-21 March 2006) interest in possession beneficiaries. The value of the former when it became comprised in the trust can now be ignored in calculating the rate of tax on the latter.

The losers

Those using pilot trusts to multiply nil rate bands were the losers. The value of same day additions is now included in calculating the rate of tax (Inheritance Tax Act 1984 s 68(5)(e).

Same day additions are defined in s 62A. Broadly, there is a same day addition where property is added to two or more relevant property trusts on the same day or the value of either is increased on the same day. (Thus an addition to a disabled trust is ignored even if it occurs on the same day as an addition to the relevant property trust as it is not relevant property.)

In calculating the hypothetical transfer used to calculate the tax rate on Trust 1, you must now include:

- the value of the same day addition in Trust 2 at the date the addition was made (s 66(4)(d)); and

- the value of whatever relevant property was comprised in that other settlement on the date it commenced (s 66(4)(e)).

There are certain exceptions to same day additions: small increases in value of £5,000 or less after 9 December 2014 are not same day additions if the transfers of value are by lifetime disposition (i.e. not on death). Same day additions to charitable trusts are also excluded.

What about the position for trusts where property was added on the same day before 10 December 2014? These are protected provided that there have been no additions to the trust by the settlor subsequently (under s 62B, additions to existing trusts made by will on deaths before April 6 2017 are also excluded as same day additions). The smallest lifetime addition by the settlor after 9 December 2014 to existing trusts, even if within the annual exemption or under £5,000, will potentially take a pre-2014 settlement out of protected status and the earlier same day additions are included.

A pre-2014 settlement which is still a protected settlement at the expiry of the period of two years after the settlor’s death (the period in which the testator’s testamentary dispositions might be altered by a deed of variation) is no longer at any risk of losing its protected status.

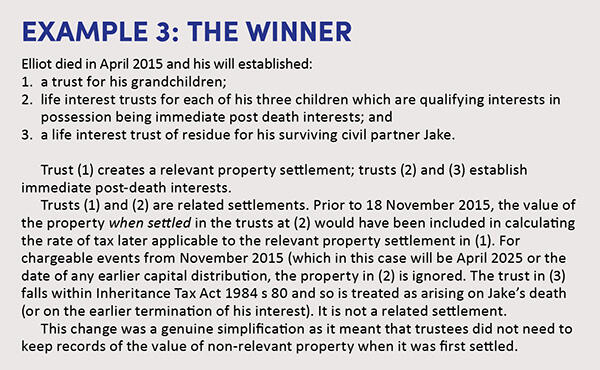

Image

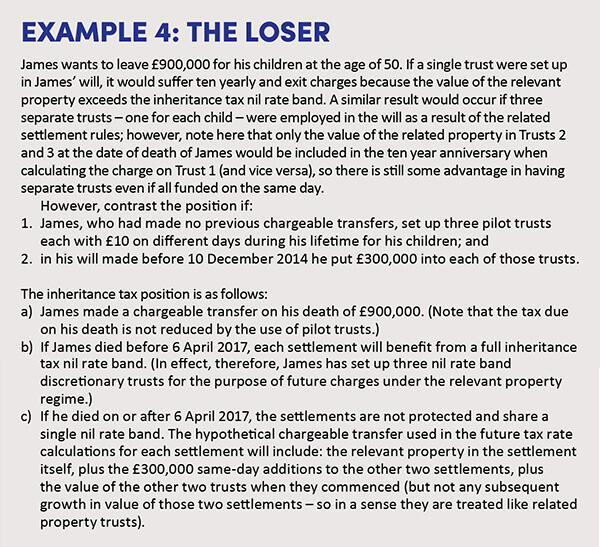

Image

In summary

Given that there are still many trusts around that were set up and funded with same day additions before December 2014, it is sensible to avoid additions to such trusts by the settlor now. If the settlement needs cash, arrange for someone other than the settlor to do it. If the settlor then dies leaving a will which adds property to the pre-December 2014 settlement, give careful thought to appointing the property away from the settlement within two years of the death, taking advantage of Inheritance Tax 1984 s 144.

It is possible to ‘undo’ the property added by will to the trust by an absolute appointment out of the trust or an appointment onto immediate post-death interest in possession trusts within two years of death.

A second article by Emma Chamberlain on the future use of multiple trusts will be published in March 2022.