Implied trusts and beneficial ownership: who is the real owner?

Share this article

Whilst express trusts are deliberate arrangements, the all-important beneficial ownership of an asset or income stream can be unknowingly split from legal ownership. We examine how beneficial ownership works in practice.

Key Points

What is the issue?

Beneficial ownership of an asset or income stream is determinative for income tax, capital gains tax and inheritance tax. It is not always with the legal owner.

What does it mean for me?

Whilst most transactions between individuals are straightforward and involve the transfer of both legal and beneficial titles, it’s just possible they may not. It may transpire that the beneficial ownership never left the donor, in which case there would be no tax implications and an implied trust merely bestows the recipient with trusteeship (unwittingly).

What can I take away?

Make sure all transactions are properly documented so that everyone party to a transaction knows the position and intention is clearly evidenced. This avoids the need for the law to make presumptions.

© Getty images/iStockphoto

‘Taxation of income is based on beneficial ownership, not legal ownership. For income tax purposes, you need to know who is the beneficial owner of the income, that is, who is “entitled to” the income.’ This is the word according HMRC in the Trusts, Settlements and Estates Manual (TSEM9305). It summarises the position taken by the courts for hundreds of years; i.e. that it is the real or ‘beneficial’ owner who is deemed to own an asset or stream of income, even though the legal ownership might lie elsewhere.

Common law only ever recognised legal ownership but this was always subject to law of good conscience (i.e. equity), which recognised that the real owner might be someone whose name is not on the title deed. This law of equity grew alongside common law and ultimately became its master (see Senior Courts Act 1981 s 49(1), in turn stemming from the Judicature Act 1873, which merged the equity and common law courts).

This applies to the tax authorities, which recognise the prominence of beneficial ownership over legal. One way in which the law could do this is to impose an ‘implied trust’, so that the legal owner becomes a mere trustee holding the asset/income stream for a beneficial owner. Whilst that beneficial owner would have the law on their side as far as property law is concerned, they would also bear the burden of taxation. These implied trusts are essentially implied ‘bare’ trusts, as HMRC will look past the legal owner and tax the beneficial owner.

Express and implied trusts

An express trust is one which is deliberately created, usually in writing (in the form of a deed or a will) with the parties being aware of their positions and duties; also, the trustees are usually those who pay tax.

With an implied trust, however, mere trusteeship may be imposed upon someone who thinks they are the outright owner; meanwhile an individual who thought they had no interest in an asset may, according to the law of equity, be the beneficial owner and who is subject to tax.

Because trusts are a produce of equity, it is the law of conscience which governs the imposition of implied trusts.

Types of implied trusts

There are broadly two categories of implied trusts:

- ‘constructive’ trusts; and

- ‘resulting’ trusts: these are sub‑divided into ‘presumed intention’ and ‘automatic’.

Constructive trusts

A (traditional) constructive trust is arguably a form of restitution. When someone has knowingly appropriated property illegally, by abusing a position of fiduciary trust, then a constructive trust rights that wrong by removing the beneficial ownership from the culprit and placing it into the hands of the wronged person.

An example given by HMRC in the Company Taxation Manual (at CTM20090) is where a shareholder receives a dividend from their company, knowing (or reasonably suspecting) it to be illegal (e.g. due to a lack of distributable reserves). In this instance, the shareholder will hold those monies on constructive trust for the company; i.e. the beneficial ownership of that dividend will revert back to the company. It is much easier to simply assign the beneficial ownership, rather than the legal title of the ill-gotten gain.

Note that it is the shareholder’s knowledge (or reasonable suspicion) of the illegality that is key. If the shareholder genuinely did not realise that the dividend was unlawful and acted in good faith, then the law of conscience would not impose trusteeship upon them. However, as HMRC points out in that same guidance, where the shareholder is also a director, then knowledge of the ‘ultra vires’ payment would be presumed.

Resulting trusts

Resulting trusts arise when a gift is incomplete and the beneficial ownership returns to the donor; this would be an ‘automatic’ resulting trust. More commonly, the gift has failed due to a technicality. An asset cannot remain ownerless, so it defaults back to the original owner.

Certain ‘gifts’ are indeed presumed to be outright gifts with the legal and beneficial owner passing to the recipient for no consideration. Gifts of land are presumed to be just that (Law of Property Act 1925 s 60(3)).

However, gifts of other assets will create a resulting trust with only the legal ownership passing to the recipient and the beneficial ownership remaining with the donor. The presumption is that the donor could not have meant to gift the asset absolutely, unless there is any evidence to the contrary.

There is a ‘presumption of advancement’ (i.e. of an outright gift) when a husband makes a gift of any asset to his wife and/or children; however, gifts from a wife to her husband would cause a resulting trust to arise in the first instance. This outdated presumption was supposed to have been abolished with the passing of the Equalities Act 2010 (in s 199) but the legislation was never fully enacted.

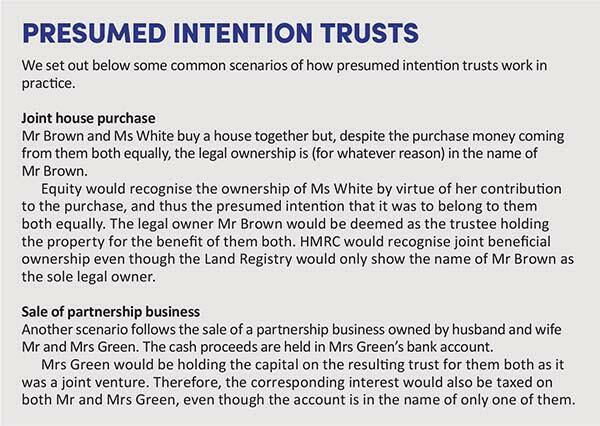

The distinction between the automatic and ‘presumed intention’ trusts was outlined by Megarry J in Vandervell Trustees (No.2) [1974] EWCA Civ 7 at 294. A ‘presumed intention’ resulting trust will, as the name suggests, bring to fruition the parties’ presumed intentions, which can be inferred by who put forward the capital to purchase the underlying asset. See Presumed intention trusts above.

Income tax and the settlements legislation

Besides being re-designated through the law of equity, beneficial ownership of income streams can also be redirected to the real owner via a legislation-based implied trust, should any attempts be made to place it in the hands of someone paying lower rate income tax.

The settlements legislation was first introduced by the Finance Act 1922, but subject to slightly more restrictive changes through the following decades. The modern legislation is now to be found in the Income Tax (Trading and Other Income) Act (ITTOIA) 2005 ss 624-648.

The definition of a ‘settlement’ is, and always has been, very wide. ITTOIA 2005 s 620(1) now defines it as: ‘any disposition, trust, covenant, agreement, arrangement or transfer of assets (except that it does not include a charitable loan arrangement)’. It is an example of implied trusts being created by tax legislation as a ‘corrective’ measure to counter a bounteous (i.e. non-commercial) settlement.

The person who created a settlement and provided the funds (directly or indirectly) is the settlor; and if that person, their spouse or minor unmarried children can still benefit from a settlement or arrangement, then that settlor is taxed upon the income of those beneficiaries. Oddly, HMRC includes ‘friends’ (however one defines this) in its Trusts, Settlements and Estates Manual (TSEM4320) as coming within this remit alongside spouses and minor children, despite this not being mentioned in the legislation. That income is essentially redirected back to the settlor who earned/generated it via a settlor-interested implied trust.

Spousal ‘get-out’

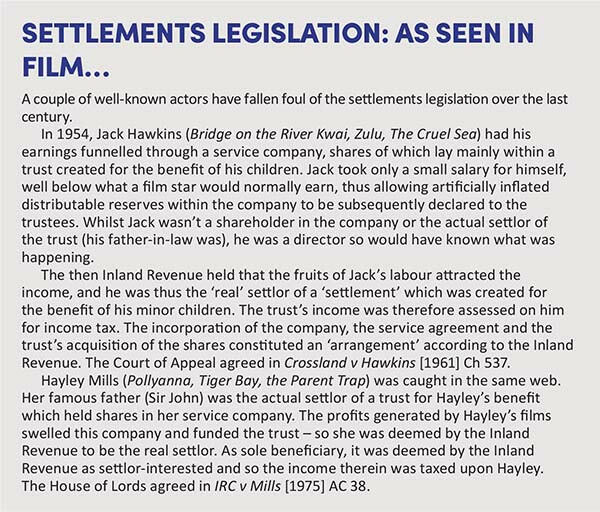

Whilst income above £100 gifted to one’s children would be taxed upon the settlor, there is a statutory exemption (Income and Corporation Taxes Act 1988 s 626, formerly s 660(6)) for gifts to settlor’s spouses which are not wholly gifts of income; i.e. they also consist of the underlying capital asset. Prior to 1990, a wife’s income was taxed on the husband (‘aggregated’) anyway, so the settlements legislation was primarily aimed at minor children. It was only after 1990 that a husband’s diverting income to his wife became as issue for the Inland Revenue.

This was tested in Jones v Garnett [2007] 1 WLR 2030 (better known as the ‘Arctic Systems’). This case also involved a limited company receiving monies from an individual’s trade. The individual was taking a much smaller salary than he should, thus artificially inflating the distributable reserves which were then paid out to his wife. Mr Jones was an IT specialist who owned Arctic Systems Ltd equally with Mrs Jones; whilst he was doing all the client work, Mrs Jones was company secretary and focused on administration. Despite this, both received equal dividends which the Inland Revenue believed formed part of an arrangement.

The House of Lords agreed that a settlement had been created; however, because Mrs Jones owned 50% of the company shares commensurate with the income, the ‘gift’ was not one purely of income but was also accompanied by underlying shares. There was some disagreement between the Law Lords about whether bounty was present in this case, but it was held that the settlement came within the s 660(6) exemption. There were subsequent plans by the government to legislate to overturn this ruling, but they were eventually dropped.

Why does this matter?

Tax advisers need to keep their eye on the beneficial ownership ball, which is what matters as far as tax is concerned. Don’t assume this lies with the legal owner. If another person has contributed capital to the purchase of an asset, the equitable presumption is that it is jointly-beneficially owned. If a gift is made, don’t assume that the beneficial ownership has necessarily followed the legal title (it may not have been intended as a gift and equity may doubt that too). If income is being diverted to family members then the settlements legislation may divert it back to the ‘settlor’; i.e. the person who actually generated it and to whom it really belongs.