Income tax issues in commercial letting

Share this article

The income tax issues involved when individuals buy property with a view to commercial letting.

Key Points

Key Points

What is the issue?

Tax advisers will often be asked to look at property issues and they will need to be confident in their knowledge.

What does it mean for me?

This is a fascinating but practical area of tax, with lots of rules, that is constantly in demand from clients.

What can I take away?

That legislation is the key and a good grip on the law is essential to give good advice.

This is a the first of a two part back to basics article on property matters for individuals. It does not specifically cover property matters for corporates, although some of the issues are the same. This first article will look at income tax issues and the second will concentrate on the capital tax aspects of investing in property.

Some individuals will buy property as a commercial venture and some will buy as a place to live (nesting rather than investing). Here, we are predominantly concerned with property as a commercial venture and we will be looking mainly at investments in residential property.

The income tax aspects

When an individual buys property with a view to commercial letting, the Income Tax (Trading and Other Income) Act 2005 (ITTOIA 2005) distinguishes between two portfolios:

- a UK property business (s 264); and

- an overseas property business (s 265).

They are both taxed on a tax year basis. There are some important outcomes from this distinction. I have picked two of these.

1. The territorial scope in s 269

- Profits of a UK property business are chargeable to UK tax, whether the business is carried on by a UK resident or a non-UK resident.

- Profits of an overseas property business are chargeable to UK tax, only if the business is carried on by a UK resident.

This obviously makes it essential to know your client’s residence status in a particular year.

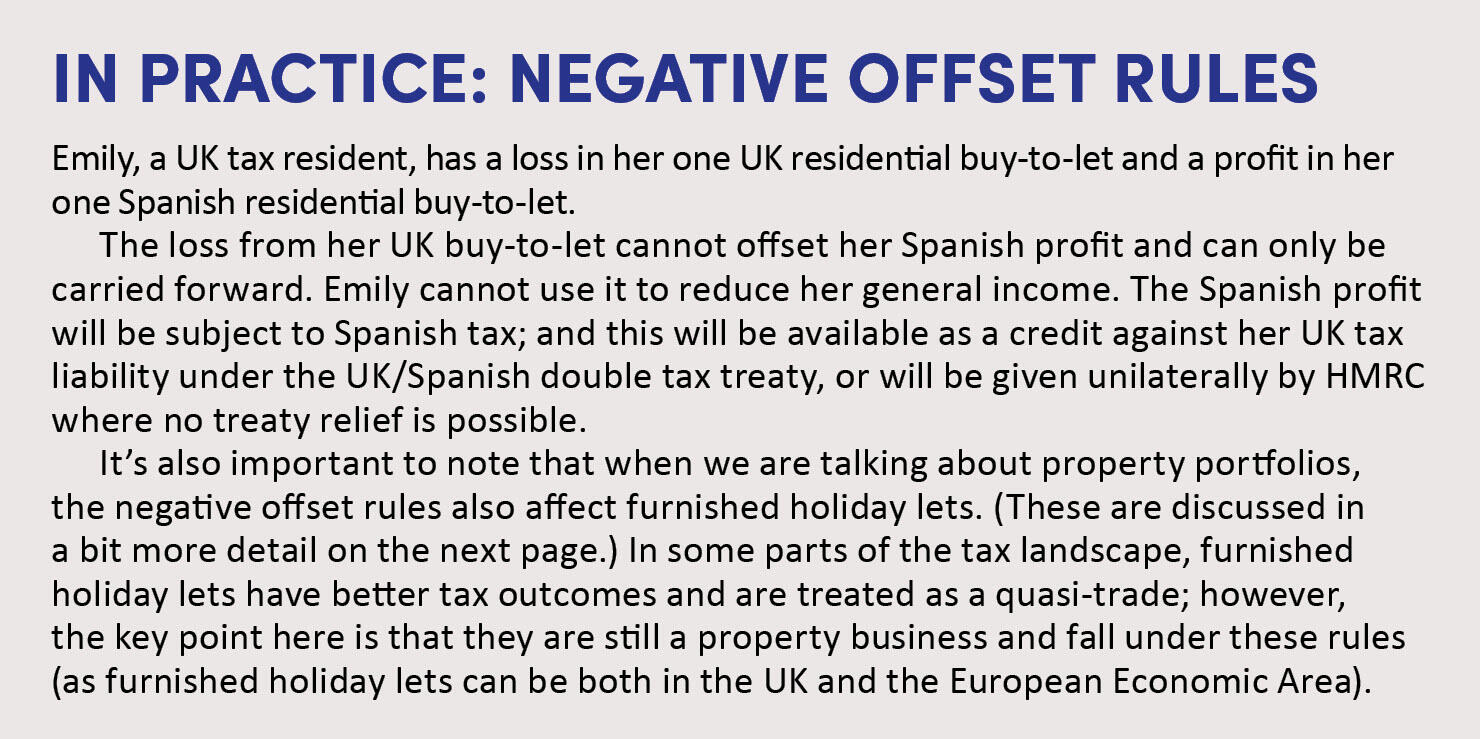

2. Offsetting of property tax losses

The principal issue here is that the two portfolios (‘boxes’) do not intermix when it comes to offsetting income tax losses. A loss from one ‘box’ cannot be carried across and used to offset a profit in the other box. This is a two-way rule.

Broadly, property tax losses from either or both of the boxes can only be carried forward against future profits from the same box (Income Tax Act 2007 s 117) ), although there are some limited exceptions to this. Common to losses in both boxes is that they cannot be relieved against general income.

Trading losses

So far we’ve been talking about the offset of property losses. It’s also worth putting this into context in respect of the offset of trading losses.

If a person sustains a trading loss, there is no general impediment to offsetting these losses against other income, which can include property income in the current tax year of the loss and/or the previous tax year (Income Tax Act 2007 s 64). Note too, that the Finance Act 2021 provisions temporarily extend the trading loss carry back provisions to two further years, subject to the provisions in Finance Act 2021 Sch 2.

The clear conclusion is that property losses are treated much more harshly than trading losses.

The income tax rules

The basic income tax rules for taxing property business profits are in ITTOIA 2005. Property accounts must be prepared under GAAP and in the same way as trading profits, unless this is trumped by another rule (see s 271E) – for example, the cash basis, which is required in a tax year where receipts do not exceed £150,000 unless the individual has elected back into GAAP.

Whether a client should be on the cash basis is a matter for discussion between them and their advisers. Many small landlords will use the cash basis.

In property, the tax rules generally follow the trading rules (ITTOIA 2005 s 271E), so ‘wholly and exclusively’ and not capital (subject to the cash basis relaxations).

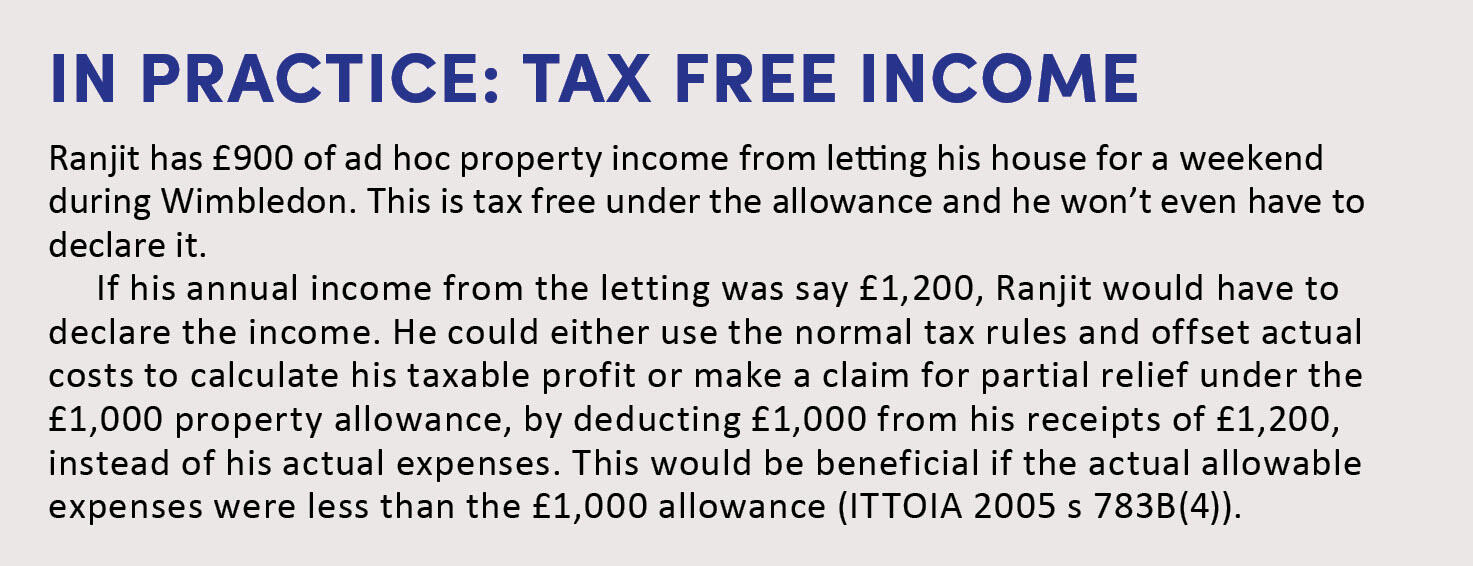

For small property profits (say, out of ad hoc lettings), the £1,000 ‘property allowance’ allows annual tax-free property income (not profits) up to £1,000 per individual owner, to be used as an alternative to the normal deductions basis; however, the normal deduction rules are not then available (s 307G). The rules on the property allowance allow for partial relief if the income is above £1,000.

Rent a room relief

This is a useful relief for owners of residential property, who rent a furnished room or rooms in their only or main residence (ITTOIA 2007 s 784). It can also be used by small-scale bed and breakfast owners.

This essentially allows for tax-free income from letting rooms to lodgers in a taxpayer’s house. It is useful to think of this as a ‘lodgers’ relief’, as it then allows us to more quickly understand how its capital tax equivalent (lettings relief) works. More of this in the next article.

The relief allows for up to £7,500 per tax year income receipts to be tax free in a taxpayer’s household – either accruing to an individual owner, or halving to £3,750 for shared ownership.

If the income exceeds the allowance, then a taxpayer can choose how to be taxed – either on a normal P&L basis, or an alternative basis by which only the excess over the threshold will be taxed.

Importantly, this relief is not available for letting an annexe, or say a flat over the garage, as the let area needs to be part of the main residence. A simple litmus test of this is is whether the lodger has to use the same front door as you do.

There is a useful HMRC Helpsheet (HS 223) that provides the essential information.

Tax relief on ‘dwelling related loans’

I want to turn now to a common scenario of a client who has a buy-to-let property which has been purchased with a mortgage.

There is no marginal tax relief available for ‘dwelling-related loans’ (ITTOIA 2005 s 272A) for the 2020/21 tax year onwards. (It has been progressively diminishing since 2017/18.)

Instead, a relief broadly equivalent to basic rate relief is given by way of a tax reducer in the taxpayer’s income tax computation. Your software should automatically calculate this if you have filled in the right boxes in the supplementary property pages of a tax return, but it’s always worth checking.

This restriction does not apply to furnished holiday lets.

Tax relief on capital items

Landlords will purchase items such as fridges and sofas for use in their let properties, and the question then is: what tax relief are they eligible for?

Capital Allowances Act 2001 s 35 specifically disallows capital allowances in a dwelling house in either a UK or an overseas property business – unless it’s a furnished holiday let (see below). So landlords will have to use the alternate replacement of domestic items relief (RDIR) in ITTOIA 2005 s 311A.

RDIR is specifically targeted at the replacement of domestic items; critically, therefore, it does not apply to the first spend – that is ‘dead spend’. They must be broadly like-for-like replacements, although changes in technology are acceptable.

Note that s 35 is limited in scope to items within the house, so does not preclude capital allowances on items not in a dwelling house.This would include things like ladders, mowers and trailers used by a landlord in a property business. That’s normal capital allowance territory.

Furnished holiday lets

Furnished holiday lets occupy a rather strange place in the UK tax landscape. Although they are ultimately a property business (either in the UK or the EEA), they in some ways feel like a quasi-trade and receive rather better tax reliefs than buy-to-lets.

Furnished holiday lets are eligible for capital allowances, so they don’t need to rely on the RDIR rules and therefore get more immediate tax relief on qualifying expenditure. Note, however, that capital allowances may be repayable if a property loses its furnished holiday let status.

Furnished holiday let status is achieved by meeting the rules. The two most obvious are that:

- broadly in a tax year, the property is available for 210 days and is actually let for 105 days (ITTOIA 2005 s 325); and

- the property cannot be let to the same person for more than 31 days.

There are relieving provisions if a furnished holiday let is part of a property portfolio of furnished holiday lets, and also where the let meets the qualifying conditions in one year and then fails in the next two years.

Income from furnished holiday lets also qualifies for pension tax relief as it is ‘relevant earnings’. This is not the case for buy-to-let income.

There is a useful HMRC Helpsheet (HS 253) that provides the essential information.

Sharing spousal and civil partner income

As advisers, we are often asked about the unequal spousal/civil partner sharing of income from a jointly held buy-to-let, perhaps to use underutilised personal allowances or basic rate bands.

The starting point (subject to certain exceptions) is that the two individuals are entitled to income in equal shares (Income Tax Act 2007 s 836). This is often not the outcome that the clients desire. So if they make a joint election under Income Tax Act 2007 s 837, then the property income will instead be taxed according to their actual unequal shares, which must reflect their beneficial interests in the property.

This is the Form 17 procedure – an HMRC download which should be posted to HMRC together with the paperwork that supports the unequal holdings. The Form 17 procedure cannot be backdated more than 60 days.

If changes are required in the property ownership to achieve this, then legal advice should be sought.

It is important to note that these two sections only apply to spousal or civil partner relationships. They do not apply to other property ownership arrangements, such as a parent and child or life partners not in a formal marriage/civil partnership.

In these circumstances, the share of property profits and losses will usually be based on the actual share of ownership.

Conclusion

As ever, as tax advisers, we need to be aware of the whole landscape and to be able to use our peripheral vision to solve problems. Property tax like other areas, is multi-faceted.