The lay of the land

Share this article

Andrew Symons examines the CGT implications of assignment and grant of land leases

Key Points

What is the issue?

The capital gains tax implications of the assignment and grant of land leases can be complex.

What does it mean to me?

Transactions concerning land often involve significant numbers and so correctly assessing the facts of a case is important to avoid potentially costly errors.

What can I take away?

By working through the facts of a case methodically the correct tax analysis should not, in many cases, be unduly difficult to reach. Particular care must be taken in establishing restrictions on or reductions to allowable costs.

Where an individual makes an outright disposal (assignment) of, or grants an interest in, a lease relating to land, they are disposing of a chargeable asset.

Where a lease is granted, this represents a part disposal of the asset from which the grant is made.

The proceeds of disposal, after the deduction of allowable costs, are subject to capital gains tax (CGT), assuming a gain arises. This article focuses on some of the main provisions which apply to such a disposal when calculating the chargeable gain, or loss.

Statutory references are to Schedule 8 of the Taxation of Chargeable Gains Act 1992, unless otherwise specified.

Meaning of ‘lease’

It is important to first consider some definitions. For CGT purposes a lease of land is given an extended definition at paragraph 10(1) as including an underlease, sublease or any tenancy or licence, and any agreement for such and, in the case of land outside the UK, any interest corresponding to a lease as so defined.

Lease duration

Where the duration of a lease does not exceed 50 years it is considered a wasting asset (a ‘short’ lease); a fact which significantly impacts the gain computation, hence its identification is of great importance.

Often, the duration of a lease will simply be its length as determined by the lease agreement. However, it may be treated differently in some circumstances. Reference only to the facts known or ascertainable at the time when the lease was acquired or created need be made.

When determining the length of a lease:

- Where it is terminable by way of notice given by the landlord, it is taken to expire on the date it could first be terminated under such notice;

- Where its terms (or other circumstances) render it unlikely to continue beyond a given date (before its natural expiry), it is taken to expire on that earlier date. This applies in particular where rent is due to substantially increase or some other onerous obligation crystallises and the lease may be terminated by notice given by the tenant;

- Where the tenant can extend the lease unilaterally by notice, it is assumed to be so extended subject to the right of the landlord, by notice, to determine the lease.

Assignment of a long lease (>50 years)

Where the duration of an assigned lease exceeds 50 years, the normal gain computational rules apply. Namely, cost (including enhancement expenditure) is deducted from disposal proceeds to arrive at the chargeable gain, or loss.

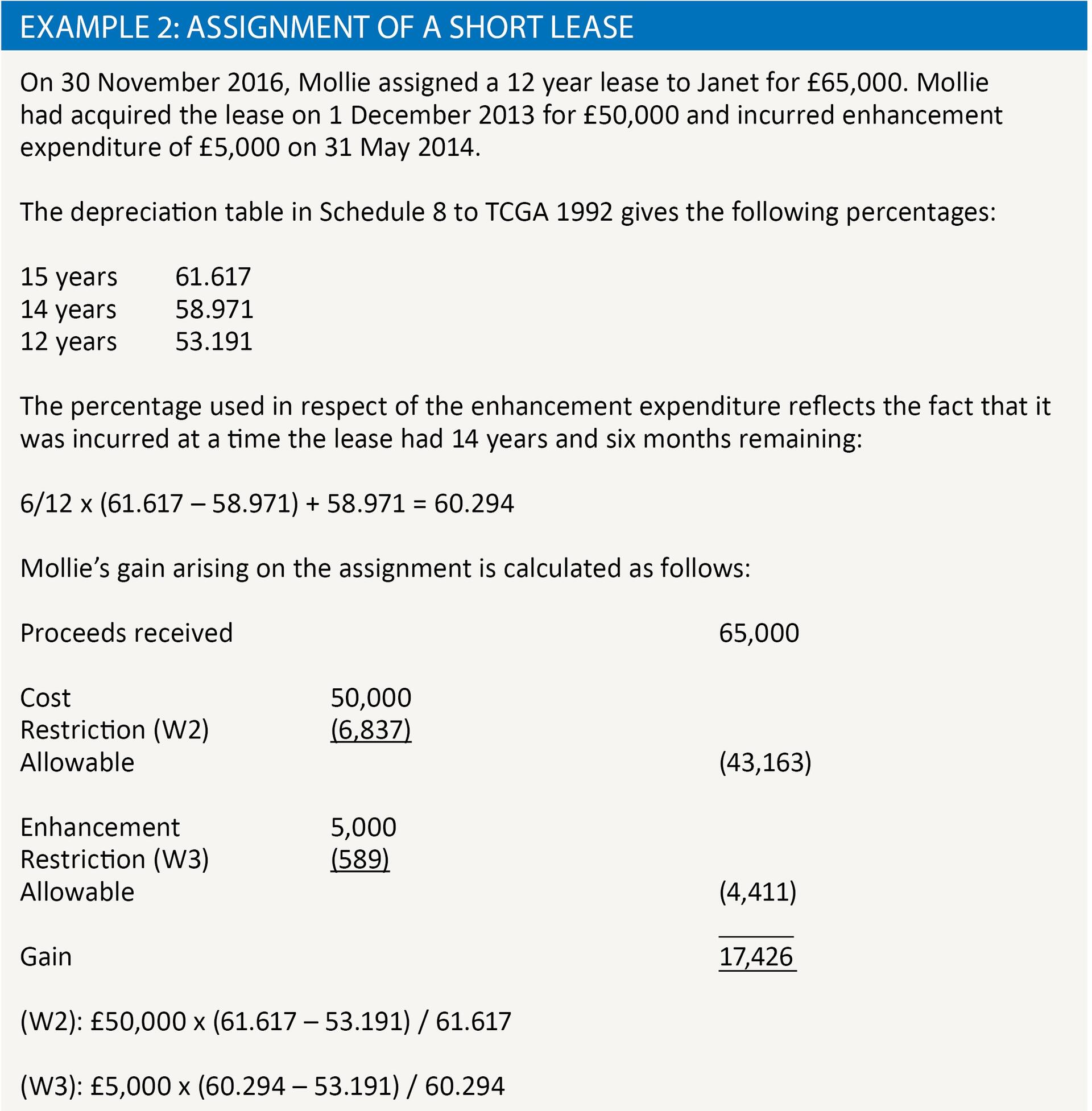

Assignment of a short lease

Where a short lease (determined as at the date of assignment) is disposed there is a restriction on the amount of expenditure which is allowable (the lease being a wasting asset).

A curved line reduction in the allowable cost is made with reference to the depreciation table, containing percentages, in paragraph 1, which also provides the fraction with which to calculate the restriction: (P(1)-P(3)) / P(1).

P(1) represents the percentage for the unexpired lease term at acquisition of the lease and P(3), the percentage derived from the table for the length of unexpired lease at the date of disposal.

Enhancement expenditure is similarly restricted using the fraction: (P(2)-P(3)) / P(2), where P(3) is defined as above and P(2) is the relevant percentage for the length of unexpired lease term at the time of enhancement.

An exception to this treatment includes where a lease is acquired subject to a sublease otherwise than at a rack-rent and the lease’s anticipated value at the time of expiry of the sublease exceeds the allowable expenditure on disposal. Here, the lease is not treated as a wasting asset until the end of the duration of the sublease.

Another exception arises where the property subject to the lease has, during the period of ownership, been used solely or partly for the purpose of a trade, profession or vocation and capital allowances have or could have been claimed in respect of the lease or related enhancement expenditure.

The lease percentages in paragraph 1 are stated in whole years; where the duration of the disposed lease is not a whole number of years, a monthly apportionment should be applied. For this purpose, 14 days or more counts as one month.

Where, at acquisition or enhancement, the lease is not a wasting asset (but it is when sold), P(1) and P(3) are taken to be 100 when wasting each element of cost. See example 2.

Meaning of ‘premium’

Before discussing the grant of leases, the meaning of premium must be understood. Premium is defined in paragraph 10(2) as including any like sum (other than rent), whether payable to the intermediate or a superior landlord, on or in connection with the granting of a tenancy. It is presumed that such a sum paid represents a premium except in so far as other sufficient consideration can be shown to have been given.

A premium may be paid in cash or in money’s worth.

Other capital sums may be treated as premiums. For example, where the landlord is a freeholder or leaseholder (with more than 50 years to expiry) and a payment is made by their tenant under the terms of the lease for the commutation of rent, as consideration for the surrender of the lease, or as consideration for the variation or waiver of terms of the lease, that sum is often treated as if it were a premium.

The occurrence of such a deemed premium does not require revision of a previous disposal computation; it is considered a separate transaction and hence a further part disposal. There are a number of more specific provisions in this area which are not discussed further here.

A deemed premium may also arise where a lease is granted between connected persons or persons otherwise not acting at arm’s length.

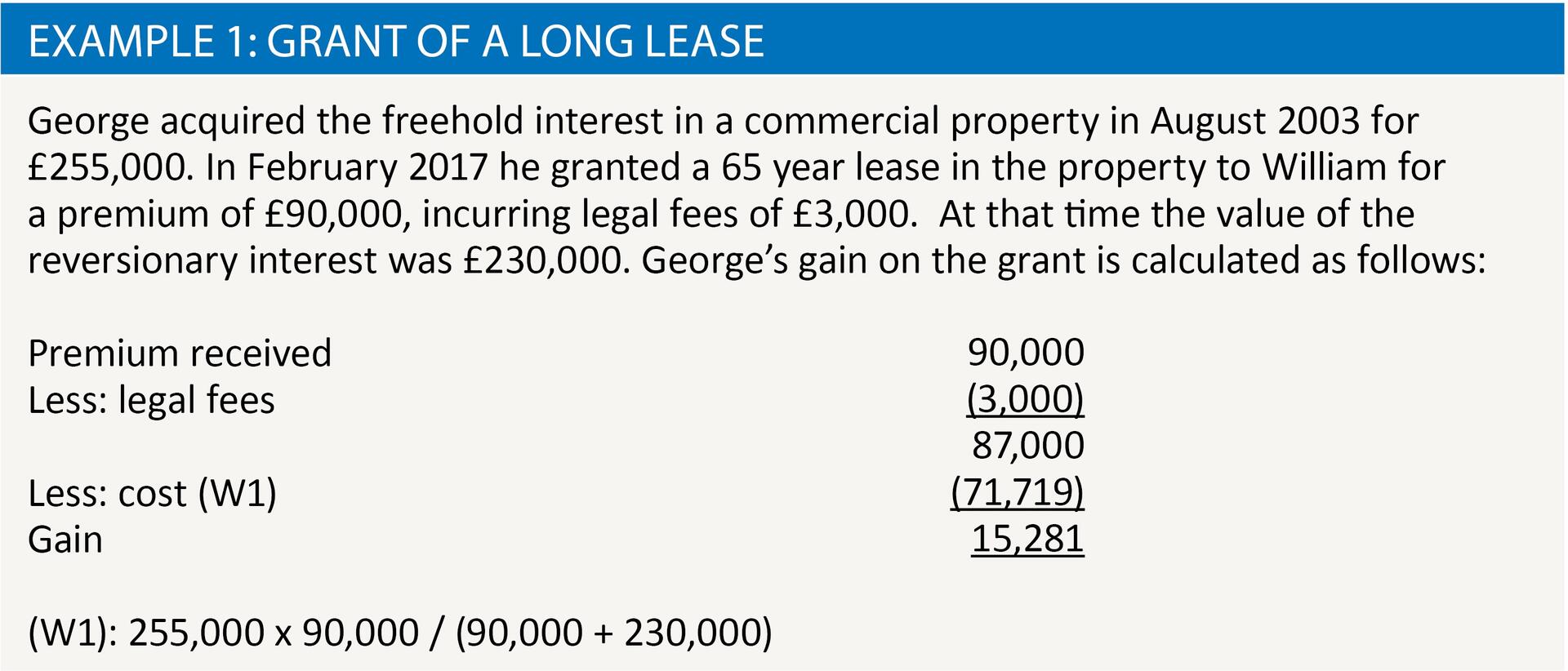

Grant of a long lease

Unsurprisingly, the premium paid on the grant of a lease is taxed after a deduction for allowable costs.

Being a part disposal, the well known apportionment of costs in s.42 of ‘A/A+B’ is applied, where ‘A’ represents the value of the premium and ‘B’, the value of the reversionary interest, including the right to receive rents under the lease.

A part disposal will still arise even where no premium is paid by the lessee. Where the landlord has incidental expenditure allowable under s.38(1)(c) a capital loss equal thereto arises. See example 1.

Grant of a short lease from a freehold or long lease

Where a short lease is granted from a freehold or long lease, part of the premium received is assessed to income tax on the landlord (the calculation of which is outside the scope of this article); this must be excluded from the CGT computation (i.e. only the ‘capital’ element of the premium is assessed to CGT, again, after a deduction for allowable costs).

Reflecting a part disposal, the allowable cost is restricted using the now subtly changed s.42 apportionment of a/A+B, where ‘a’ is the capital element of the premium. ‘A’ and ‘B’ retain the definitions as for the grant of a long lease.

Grant of a lease from a short lease

The A/A+B part disposal apportionment does not apply where a sublease is granted out of a short lease. Initially, the full premium (capital and income elements) is included in the computation, from which a proportion of base cost is deducted – a number of restrictions to this cost can apply.

Firstly, a reduction in the allowable expenditure is required where the sublease covers only part of the land subject to the original lease.

Being a part disposal of a wasting asset the allowable cost is restricted using the lease depreciation table, and fraction: (C-D)/P(1) [or (C-D)/P(2) in the case of enhancement expenditure], where ‘C’ is the relevant percentage in respect of the unexpired lease term at the time of grant of the sublease and ‘D’, is the relevant percentage in respect of the unexpired lease term at the time when the sublease expires. The definitions of P(1) and P(2) remain as before.

Before applying ‘(C-D)/P(1)’, allowable cost is reduced for the grantor, where their interest in the asset was itself acquired by way of grant (of a short lease) to the extent that they have received a deduction for the purpose of calculating the profits of a trade, profession or vocation in respect of the income element of the premium previously paid by them.

Additionally, where the actual value of the premium paid on the grant of the sublease is less than that which would have been paid (the ‘notional premium’) had the rent payable under the sublease been the same as that payable on the head-lease then the allowable cost on the grant of the sublease is reduced in the proportion: actual premium/notional premium. This seeks to prevent tax manipulation arising by charging higher rents in lieu of a lower premium, thus avoiding CGT.

Finally, to arrive at the chargeable gain, a deduction is made for the element of the premium which is assessed to income tax. This deduction cannot convert a gain into a loss, or increase a loss.