Lessons to be learned

Share this article

Neil Warren gives some VAT saving tips and pitfalls to avoid in relation to supplies of private tuition

Key Points

What is the issue?

The VAT liability of supplies of private tuition can vary according to the subject being taught and the legal entity which is providing the services. It is important to be clear about the relevant provisions in the legislation to avoid output tax errors being made.

What does it mean to me?

If supplies are exempt from VAT, they are not included in the registration test – only taxable sales are included. And in cases where employees or subcontractors provide tuition as well as a sole trader or partner, then output tax apportionment will be needed.

What can I take away?

Private tuition provided by a limited company is always standard rated, so if a person has more than one business activity, it will save VAT if the private tuition income is kept as a sole trader or partnership, with a different entity for the other activity. But the split needs to be carried out on normal commercial terms to avoid a potential challenge from HMRC.

Why are the VAT rules on private tuition so important? One reason is because it is one of the few situations in the world of the nation’s favourite tax where the rules are different for an incorporated business compared to one that is unincorporated, such as a partnership or sole trader. And secondly, owners supplying private tuition services often have their fingers in other business pies (for example, a piano teacher also selling musical instruments), so there might be scope to do some business splitting as well, potentially avoiding the liability to register one or both entities for VAT. But great care is needed if this route is taken, as I will explain in this article.

Basic rules

Private tuition is exempt from VAT if two important conditions are met:

- It is given in a subject ordinarily taught in a school or university.

- The tuition is given by either a sole trader or member of a partnership in a personal capacity. (LLPs are accepted as a partnership.)

(The relevant legislation is VATA 1994 Sch 9 Group 6 Item 2; see also HMRC Notice 701/30 s 6.)

The legislation means that any tuition provided through a limited company is always standard rated, even if the tuition is given by a sole company director who is also a 100% shareholder of the company. The issue of fiscal neutrality was considered in the case of Empowerment Enterprises Ltd [2008] CS 2006; in other words, is it fair for a limited company to pay tax on supplies that are exempt when provided by a sole trader or member of a partnership? However, the court concluded that the word ‘private’ could only be associated with a sole trader or partnership so the appeal was dismissed.

If private tuition is provided by employees or subcontractors on behalf of the business, it is always standard rated. And if a session is provided jointly by both employees and a sole trader or partner, output tax can be apportioned in any fair and reasonable way. If the calculation process is too time consuming, then HMRC generously confirm that all income from joint tuition can be treated as taxable! (See HMRC VAT Education Manual VATEDU 40400.)

Dancing classes and exemption

There is no doubt that the issue of whether a subject is ordinarily taught in a school or university has kept the courts busy over the years. And the most recent First-tier Tribunal case about dancing classes was a controversial decision.

In A Cook [2019] UKFTT 321, Ms Cook gave tuition in a form of dance known as the Ceroc brand (a franchise), which has 900 different dance moves, mainly linked to Latin American origins. The classes were held at 11 different venues and were described as a ‘fun night out and a way of meeting members of the opposite sex’. There was a licensed bar, disc jockeys were employed to play the music, and each attendee paid between £5 and £8 per session. The priority was to promote ‘entertainment, socialising and dance tuition’.

Having read this summary, you might agree with HMRC’s conclusion that the sessions were ‘recreational’ rather than ‘educational’ and that VAT exemption did not apply. However, the tribunal disagreed and decided that Ceroc moves ‘should be considered as being the same as teaching dance in a school or university’. The judge felt that the advertising of the event as ‘fun and entertaining’ did not detract from the ultimate purpose, which was to teach dance. The appeal was allowed.

What does ‘ordinarily taught’ mean?

The exact wording in HMRC’s notice 701/30, which is an interpretation of the legislation rather than having legal force, is that ‘the subject is one taught regularly in a number of schools or universities’. I like this phrase: for example, there is a university in Lancashire that has a two-year degree course in soap opera studies but it is an isolated course so exemption would not apply to private tuition given about the latest storylines in Eastenders or Coronation Street.

The above wording will produce a clearcut VAT answer in most situations. For example, there is no doubt that piano, singing and maths lessons will all qualify for exemption but court cases in recent years have confirmed that the following subjects do not qualify:

- Transcendental meditation – Colin Beckley (VTD19860);

- Belly dancing – Audrey Cheruvier (TC03148);

- Yoga – Stuart Tranter (TC4071); and

- Pilates – Christine Hocking (TC4130).

So, bringing these issues together, the judge in the Cook case focused on the subject being taught, namely dance, and associated this with education rather than recreation.

Business splitting

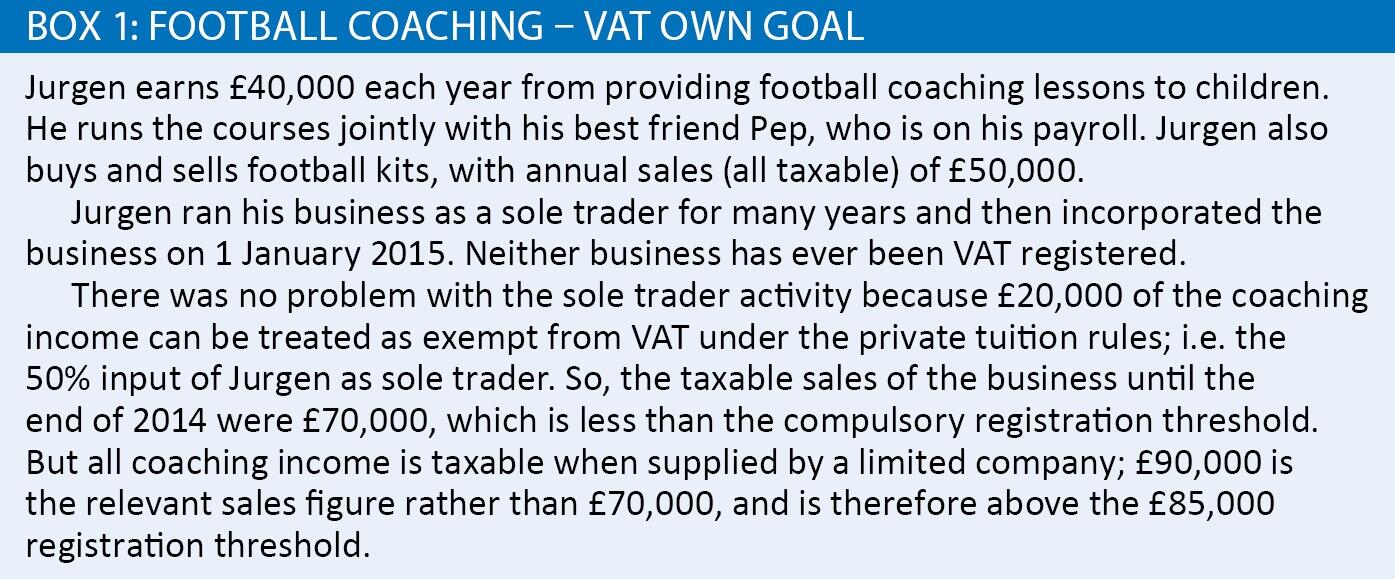

One of the biggest own goals I encountered many years ago involved a football coaching business that also bought and sold football kits. The owner (a sole trader) took his accountant’s advice and incorporated the business. See the example of Jurgen in Box 1: Football coaching: VAT own goal.

In reality, a decision to keep the coaching activity in Jurgen’s sole trader business and just transferring the merchandising activity to a limited company would have been a complete ‘win: win’ for VAT purposes:

- It avoids the need for the company to register for VAT in the short term.

- The company has scope to increase annual football kit sales from £50,000 to £85,000 without registering for VAT. It is no longer partly inhibited by the fact that 50% of the coaching fees were taxable under the sole trader entity.

HMRC challenge?

Business splitting is always a favourite topic among clients and advisers. I predict this will be particularly relevant in the next three years at least, as a result of the registration threshold being frozen at £85,000 until at least April 2022. In reality, Jurgen’s business split should be fine as long as he is clearly focused on keeping both activities separate in terms of invoicing arrangements, bank accounts, supplier accounts, advertising and general organisation. This should be possible because one of his activities involves selling goods and the other is supplying services.

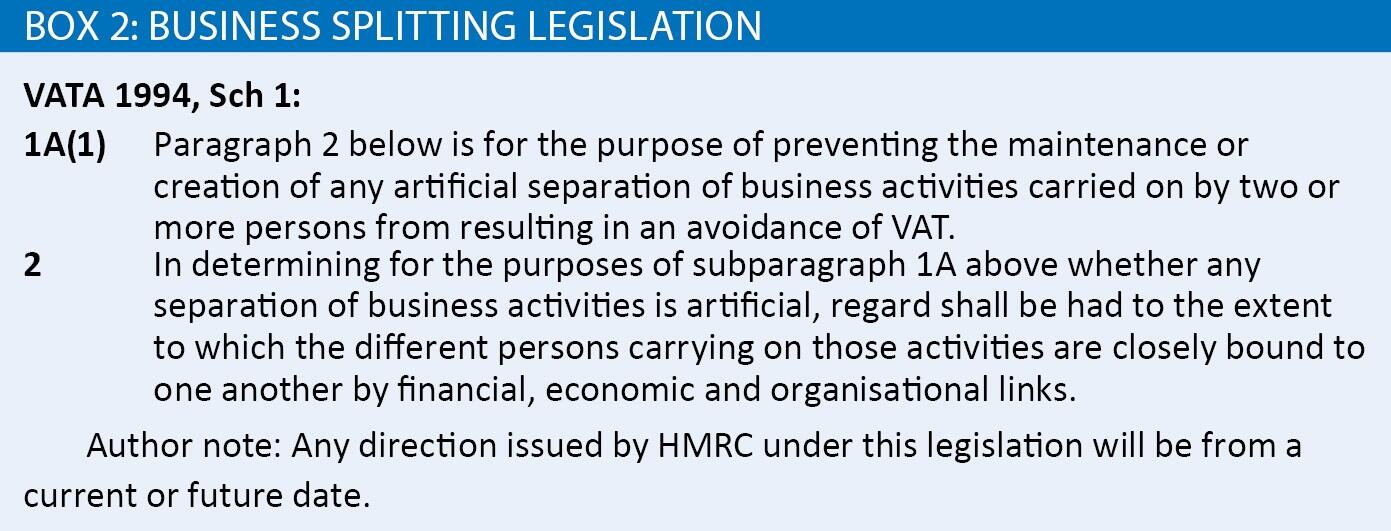

HMRC has the power to issue a direction to treat separate entities as a single business (see Box 2: Business splitting legislation). However, note that the key word is ‘and’ rather than ‘or’; i.e. all three links must be proven.

The worst possible outcome with a business splitting scenario is that HMRC decides there never have been two businesses artificially separated, and only ever one business under a single legal entity. In such cases, there is scope for retrospective VAT registration going back up to 20 years.

Recent case win

As a final tip, it is worth reading the recent First-tier Tribunal case of Charles Caton (TC7343), a case won by the taxpayer against the odds. The reason I say this is because Mr Caton told HMRC that he owned both a restaurant and café but then claimed that the restaurant was run by his wife as a sole trader, i.e. two sole trader businesses were in place, each business having individual turnover below the registration threshold.

The judge looked at the overall intention of the taxpayers to run separate entities, rather than the overlap that was evident in relation to issues such as having common suppliers and the same banking arrangements for card payments. There were separate tills, menus and staff and Mrs Caton clearly ran the show in the restaurant. But the lesson is clear: it is important to do a business split properly from day one, rather than having to defend an HMRC challenge when the organisational shortcomings come to light.