Let me entertain you!

Share this article

The festive season means that many businesses will either be hosting Christmas parties or giving gifts to staff and clients. Neil Warren considers the VAT treatment of these expenses

Key Points

What is the issue?

Input tax can be claimed on the costs of entertaining employees because it is classed as a business expense. But input tax cannot be claimed on the costs that relate to non-employees, including shareholders, retired employees and partners/spouses of staff . Input tax apportionment will be needed for Christmas parties where both employees and non-employees attend.

What does it mean for me?

Input tax can be claimed on business gifts given away for business purposes. But output tax will be due if the total cost of gifts given to the same person exceeds £50 excluding VAT in any 12 month period.

What can I take away?

A token charge to non-employees attending a Christmas party removes the input tax block under the business entertainment rules but the charge must be compulsory and will be subject to output tax. Finally, make sure that venues charge 12.5% VAT for your Christmas meals, the reduced rate which applies to most hospitality supplies until 31 March 2022.

The relaxation of the lockdown rules hopefully means that staff and customers will be able to get together for a decent Christmas party this year. Hurrah! And for those businesses that have traded profitably, there will probably also be some decent gifts given away to reward hard work and customer loyalty. In this article, I will consider the VAT treatment of entertaining expenses and business gifts.

Entertaining costs

The starti ng point with business entertainment expenditure is that input tax can only be reclaimed on the cost of hospitality provided to staff . Entertainment given to non-staff members, such as customers, suppliers or the spouses of staff, is blocked and the input tax cannot be recovered. For example, imagine that the partners in a firm of lawyers have decided to host a big Christmas party at a local restaurant. The guest list will comprise 20 staff plus one guest each, plus some important suppliers and clients. The total party will comprise 50 people. The company can claim 40% of the VAT on the final bill as input tax; i.e. 20/50 based on the ratio of staff to total guests.

As a topical VAT saving tip, it would be sensible to agree a meal price with the restaurant that excludes alcohol and separately pay for the alcohol on the night. The charge by the restaurant of, say, £60 plus VAT per head will then be subject to 12.5% VAT, the rate that applies unti l 31 March 2022 to most hospitality sales, including catering supplies. Alcohol has always been subject to 20% VAT. The lower rate reduces the loss of input tax on the guest meals in my example.

Hosting role?

Hopefully the message from business owners will be for everyone to have a good time at the Christmas party. In other words, staff will be focusing on dancing and singing and not carrying out a hosting role to look after the non-employees. This is because a condition of reclaiming input tax on the staff meals is that the staff must not be acting as host to the guests. If that is the case, then input tax on their costs is blocked as well. (See VAT Notice 700/65, para 3.3.)

In some situations, there can be a problem with claiming input tax on the cost of directors’ meals, or sole trader and partner meals in the case of an unincorporated business. But there is no problem if an event is open to all staff , such as the Christmas party. (See VAT Notice 700/65, para 3.2.)

Unfortunately, however, exclusions from the definition of an employee include pensioners – even if they are being paid a company pension as a retired employee – and former employees, as well as shareholders who are not also employees. And although a business can often reclaim input tax on the costs of providing subsistence to a subcontractor, this would not apply to the office Christmas party.

As a separate tip, there is no monetary limit on the cost of hospitality provided to employees to enable input tax to be claimed. The annual limit of £150 per head including VAT is only relevant in the mysterious world of direct tax and means that the whole amount will be assessed as a benefit in kind for the employee if the £150 limit is exceeded. How mean is that!

Overseas customers

What would be the situation if our imaginary firm of lawyers also invited some of their prestige international clients to the party? Is there scope to claim input tax on the cost of their meals and also the hotel rooms being paid for them as an extra treat?

To give some background, there used to be an input tax block on the cost of entertaining overseas customers but then a couple of ECJ judgments meant that UK VAT law had to be amended back in 2010.

However, there is a big downside to this opportunity. Even though input tax can be claimed on the cost of entertaining overseas customers, there will be an output tax charge as a private benefit unless the expenses relate to a business meeting, and the hospitality provided is not deemed to be excessively lavish. The output tax charge will cancel out the input tax gain. There is no scope to claim input tax on hospitality provided to other international business contacts, such as suppliers or auditors. But the business meeting opportunity is not relevant to a Christmas party, which is clearly a social function, so there is no potential VAT saving here.

As a general comment, now that the UK is able to make its own VAT rules following our EU departure, it would be a useful piece of tax simplification work if the government could either allow input tax to be fully claimed on the cost of entertaining overseas customers without an output tax charge or, more likely, block it completely. This would remove the need to consider whether any hospitality is ‘reasonable in scale and character’ – a phrase used in VAT Notice 700/65, para 2.6.

Payment by guests

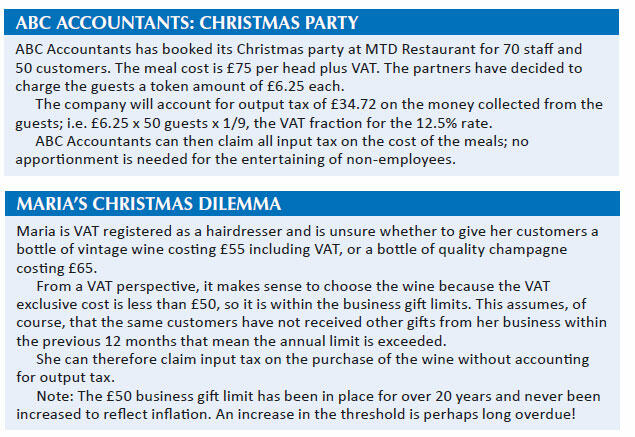

To put on my Scrooge hat, there are decent VAT savings to be made if a token charge is made to the guests. This is because a charge to guests means that the input tax block on entertaining is no longer relevant because there is no longer a supply of ‘free’ hospitality. The charge can be less than the cost of the food and drink provided to the guests. See ABC Accountants: Christmas party.

Service charges

Readers acting for restaurants and similar hospitality businesses might want to alert their clients to a potential VAT saver with service charges. If a service charge is a compulsory addition to the bill, it will be subject to VAT.

However, if it is an optional payment for the customer, described for example as a ‘discretionary service charge’, it is outside the scope of VAT as a voluntary payment. However, the restaurant staff must not insist on payment if the customer chooses not to pay because discretionary means there is a choice.

Business gifts

Imagine that ABC Accountants from my example has decided to celebrate an excellent trading year by giving bottles of champagne and wine as Christmas gifts to its best customers. Can input tax be claimed on the purchases of the goods from the wine merchant, without accounting for output tax on the onward supply to the customers?

The VAT rules allow a business to claim input tax on goods that will be given away for business purposes. And no output tax will be due on the VAT return that coincides with the date of the gift as long as it cost less than £50 excluding VAT. However, the £50 figure is an annual limit per person, so it is important to keep a record of who is receiving the gift, its total value and the date it was given.

If the £50 limit is exceeded in any rolling 12 month period, then output tax is payable on all of the gifts given to that person as if they had been sold, effectively disallowing the input tax claimed on the original purchase. See Maria’s Christmas dilemma.

In terms of the definition of a ‘business gift’, it must relate to a gift of goods that is made in the course of promoting a business. HMRC confirms that the definition includes ‘goods given to customers as a thank you’ (see VAT Notice 700/7, para 2.2). The goods don’t need to include the business name or logo.

If goods are purchased for non-business purposes, perhaps to give away to the business owner’s friends or relatives, then input tax is blocked on the purchase of the items because they are not being used for the purpose of the business.

A final bit of good news: if a business gives gifts to different employees who work for the same organisation, each natural person is entitled to receive £50 worth of gifts under the VAT rules. The threshold is not capped at £50 per business. Happy Christmas!