Levelling up: sustainable development

Share this article

The UN Sustainable Development Goals promote tax policies to support economic growth in developing countries.

Almost exactly ten years ago, on 25 September 2015, the 193 countries of the UN General Assembly adopted the 2030 Agenda for Sustainable Development which created the 17 world Sustainable Development Goals. Since then, most reputable organisations have shown some form of support or commitment to delivery of the goals.

The goals are all related. Tax policies can encourage investment, which leads to employment, which leads to taxation, which in turn leads to development. In virtually all circumstances, economic growth is a prerequisite for revenue growth.

The importance of growth

What is the purpose of taxation? The answer is clear: to provide adequate revenues that fund the necessary functions of government. In the words of an opinion in a famous decision of the US Supreme Court, ‘taxes are what we pay for civilized society’ (Compania General de Tabacos de Filipinas 275 US 87 (1927)). Taxes provide a continuing source of revenue. Governments use these revenues to promote economic development and social progress.

However, this seemingly simple question on the purpose of taxation quickly raises other equally important questions. First, how do governments determine the levels of taxation that will best meet their needs? Second, how should policymakers determine which tax policy is best?

The answer to these questions should determine both the scope and contours of tax policy and the design of the tax system. The purpose of tax policy should be to encourage investment and thus drive economic growth using a simple formula: Investment leads to employment, which leads to taxation, which leads to development.

Increases in tax revenues, and hence a government’s ability to fund essential functions, depend on profitable businesses employing workers – and on investors, domestic or foreign, placing funds into those businesses or starting new businesses. In virtually all circumstances, more growth means more revenue.

Too often, discussions on tax policy miss this most important element. It is too simple to adjust the level of tax rates in response to economic conditions (or worse, to favour certain types of economic activity over others). Instead, a focus on growth should shift policymakers’ priorities to a more fundamental question: how to design a tax system to promote the economic growth that itself drives higher revenues.

China is perhaps the world’s most prominent example of rapid economic growth leading to the eradication of poverty. Other nations seek to follow this path, but they need assistance in doing so – and encouragement to stay the course even in difficult times with demanding fiscal pressures.

Through its Belt and Road Initiative (BRI) – a massive global infrastructure and economic development strategy launched by President Xi Jinping in 2013 – China has sought to develop closer ties with developing countries around the world so that other nations may embark on the same path of development and economic growth. Over 140 countries have signed up to BRI related projects.

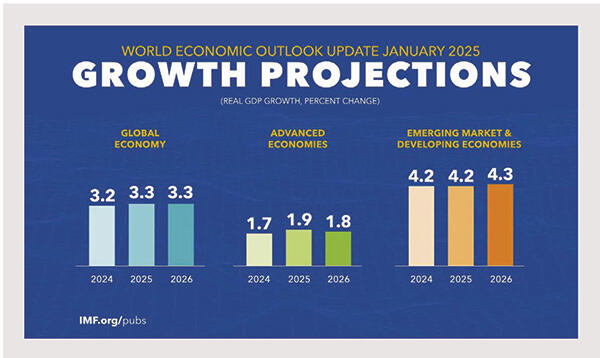

A focus on growth works. African countries highlight the trend. According to the World Bank’s Global Economic Prospects Report of June 2025, Sub-Saharan Africa’s real GDP growth is now projected to accelerate from 2.9% in 2023 to 4.3% in 2027.

Consider Kenya, which according to the Report is projected to have a GDP growth rate of 4.5% in 2025 and which is building that growth on the foundation of a very diverse economy not reliant on one dominant sector. Ethiopia, which had an economy smaller than Kenya in 2020, is also on a growth push and is expected to overtake Nigeria in 2026. Many African countries already enjoy fast growth: countries including Benin, Ethiopia, Guinea, Niger, Rwanda, Uganda and Zambia are all forecast to have growth rates above 6% in 2026.

A tax system designed to promote growth

For many countries, tax incentives have long been pivotal in attracting investment. Yet as reforms progress, policymakers must consider how to design incentives that encourage productive investment while avoiding distortions, ensuring that they contribute positively to sustainable development as part of an overall strategy for growth.

To assist this process, governments should understand how tax policy influences investors’ decisions, particularly as companies face a maze of tax regulations in a rapidly shifting environment.

Governments must also prioritise practical considerations. Companies must understand the impact of tax policies, ensure compliance and consider implications across diverse jurisdictions. Businesses generally favour broad-based and easily administered taxes. Simplifying invoicing and tax collection fosters efficiency and promotes investment. In contrast, unpredictability in a tax regime can deter investment, underscoring the importance of clarity and stability in tax frameworks to maintain investor confidence and stimulate economic growth.

It is important to stress that tax policy is not merely a question of determining tax rates. Excessively high tax rates discourage both domestic and foreign investment; excessively low rates mean that governments miss opportunities for revenue that can promote development. Setting rates appropriately is essential (and often challenging) but will depend on domestic circumstances. The more significant question is how a tax system is designed and the goals it seeks. Poor or corrupt tax administration, for instance, discourages foreign investment as surely as high rates do.

As a series of general principles, tax systems that promote economic growth are systems that are:

- fair to all taxpayers;

- predictable in their effects to drive investment and ensure that both domestic and foreign taxpayers understand their obligations;

- understandable to promote very high levels of compliance; and

- simple for revenue administrations to administer, to reduce opportunities for corruption and support fairness and predictability in the overall system.

Of course, there are important steps that countries should take even while focusing on growth: improve transparency in tax systems; seek digital and artificial intelligence efficiencies; make tax administration fairer and more predictable as regards both direct and indirect tax; and bring more businesses into the formal economy where they will pay tax. African countries, including South Africa, Mozambique and Zambia, have made important reforms in these areas.

It is also important to ensure that tax administrations in developing countries have the necessary knowledge and skills to implement the tax policies, which require what the UN calls ‘capacity building’. An example of this is China’s Belt and Road Initiative Tax Administration Cooperation Mechanism.

Capacity building: China

The Belt and Road Initiative Tax Administration Cooperation Mechanism (BRITACOM) is the non-profit official mechanism for tax administration cooperation amongst the 150 or so jurisdictions that subscribe to China’s Belt and Road Initiative. These represent about 75% of the world’s population and more than half of global GDP.

As its website (www.britacom.org) states: ‘The vision of the BRITACOM is to facilitate trade and investment, foster economic growth of the Belt and Road Initiative jurisdictions and contribute to the fulfilment of inclusive and sustainable development as set out in the United Nations’ 2030 Agenda for Sustainable Development.

The BRITACOM aims to contribute to building a growth-friendly tax environment through cooperation and sharing of best practices in following rule of law, raising tax certainty, expediting tax dispute resolution, improving taxpayer service and enhancing tax capacity building. It promotes reforms involving tax regimes in a range of industries, including extractive industries, agriculture and many others.

This work is geared to develop systems that are fair and predictable, while also promoting sustainable economic growth based on increased foreign and domestic investment. In addition, BRITACOM has promoted the concept that these systemic issues require attention at the highest levels of national policymaking.

ITIC and ADIT

Since it was established in 1993, initially to support investment in countries of the former Soviet Union, the International Tax and Investment Center (ITIC) has been running workshops in developing countries that are experiencing a significant increase in foreign direct investment, such as Tanzania, Mozambique and Uzbekistan. These events are aimed at educating local legislators and administrators in the ways of working of the industry that is making the investment. The workshop topics usually include an explanation of the industry’s value chain, tax treaties, transfer pricing, subcontractor taxes and VAT considerations.

ADIT is the international tax qualification of the CIOT. It is highly respected by both tax practitioners and tax administrations in Africa and elsewhere, with around 800 new students registering each year. In terms of student numbers, the top three countries for ADIT in Sub-Saharan Africa are Uganda, Zimbabwe and Kenya.

ITIC and ADIT are both non-profit educational organisations and collaborate on a joint exhibition stand at the annual Congress of the International Fiscal Association. At the next one, in Lisbon, ADIT will be unveiling a new, standalone award for the global minimum tax, which is Pillar Two of the OECD’s Base Erosion and Profit Shifting (BEPS) two-part solution (see tinyurl.com/38nxkncj).

To register for more information about the Pillar Two award as it develops, please contact Rory Clarke at [email protected].

In conclusion

There is simply no way to achieve the UN Sustainable Development Goals without real, sustained economic growth that lifts people out of poverty, increases gender equality, builds national education and health systems, provides funding for addressing climate change, and underpins strong domestic fiscal systems.

Collaboration and partnerships between the public and the private sector can aid governments in developing tax policy that promotes growth. This type of collaboration is supported by the UN under Sustainable Development Goal 17: Partnerships for the Goals. We should all follow its efforts and successes with interest.

© Getty images