Lights, pixels, action: the UK creative industries

Share this article

UK creative sector tax incentives are helping to fuel industry growth, while requiring careful compliance to secure their full benefits.

Key Points

What is the issue?

The UK’s creative sector thrives partly thanks to targeted tax incentives that support film, television, video game, theatre and cultural productions. These reliefs have been redesigned to comply with global tax rules, support domestic production post-Brexit and prevent misuse, while still encouraging investment.

What does it mean to me?

For creative businesses, these expenditure credits and cultural reliefs can provide significant financial benefits. However, eligibility rules, certification requirements and precise accounting demands make compliance complex.

What can I take away?

The new audio visual and video games regimes, alongside permanent enhanced cultural relief rates, signal the government’s long-term commitment to sustaining the UK’s creative industries.

Experiencing a delay on the way to my firm’s Glasgow office recently because the shooting of the latest Spiderman film had taken over the city centre, I reflected on just how successful our creative sectors have become. The UK boasts internationally renowned film studios, video games companies, museums, ballet companies and theatres – just a few of the diverse sectors which come under the umbrella of creative industries.

According to the Department for Culture, Media and Sport (DCMS), the creative industries contributed an estimated £125 billion to the UK economy in the 12 months to 30 June 2025 – a 38% increase in real terms since 2010 (see tinyurl.com/bdj86ja8). This growth reflects sustained government support and international competitiveness, despite challenges such as changing consumer habits, US trade threats and the knock-on effects of US writers’ and actors’ strikes on global productions. The rise of AI has also created new concerns around copyright, intellectual property and employment within the sector.

A key factor behind the UK’s creative success has been its tax incentives for content production. Although the original film tax relief became notorious for misuse and aggressive tax planning schemes aimed at individuals – which HMRC has spent years contesting – the redesigned system, together with a range of new incentives across other creative industries, has become a vital part of funding for the industry. These incentives fall broadly into two categories:

- expenditure credits, covering the audio-visual expenditure credits (AVEC) and video games expenditure credits (VGEC); and

- cultural reliefs, covering theatre tax relief, orchestra tax relief and museums and galleries exhibition tax relief.

This article focuses on the AVEC and VGEC regimes.

The mechanism of these reliefs was revised in recent years to align with the global minimum tax framework introduced under the OECD’s Pillar Two rules. Previously, relief operated through an enhanced deduction whereby a company could claim a payable tax credit if it claimed relief and made a loss. However, under Pillar Two, such deductions risk reducing a company’s effective tax rate below the 15% threshold, triggering top-up taxes. The AVEC and VGEC systems were therefore introduced to preserve the relief’s benefits without lowering effective tax rates for Pillar Two purposes.

The creative sector reliefs have also evolved since the UK’s exit from the European Union. Previously, eligibility generally required a certain proportion of qualifying expenditure to be incurred with the European Economic Area. Following Brexit, qualifying expenditure must now relate to UK activity, ensuring that the benefits directly support domestic production.

Expenditure credits

The AVEC and VGEC are ‘above the line’ credit regimes introduced to replace earlier reliefs for film, television and video games production, which operated through enhanced deductions and an option to surrender relevant losses for payable tax credits. These new regimes apply to all qualifying expenditure incurred from 1 January 2024 and are mandatory for claims for relief on new productions from 1 April 2025. Productions that began before that date may still claim under the historical incentives until 31 March 2027.

Qualifying expenditure

The AVEC and VGEC reliefs do not cover all production expenditure but costs in relation to the following can qualify:

- Film and TV: pre-production, principal photography and post-production; and

- Video games: designing, producing and testing.

Certain types of expenditure are explicitly excluded from qualifying for relief:

- Research and development (R&D) expenditure, even if no R&D tax relief claim is made.

- Any amounts unpaid four months after the year end do not qualify until they are paid.

- Expenditure that generates non-arm’s length profits for connected parties is disallowed, as are completion bonds and other forms of insurance.

- Initial concept design costs do not qualify, nor does expenditure that would ordinarily be disallowable under corporation tax rules, such as entertaining and capital expenditure.

- Publicity, marketing and promotion costs are excluded, as are expenses related to debugging video games, audit fees, sales and distribution costs, and financing costs.

These exclusions ensure that relief remains focused on genuine production activity rather than ancillary or administrative expenditure.

What’s the benefit?

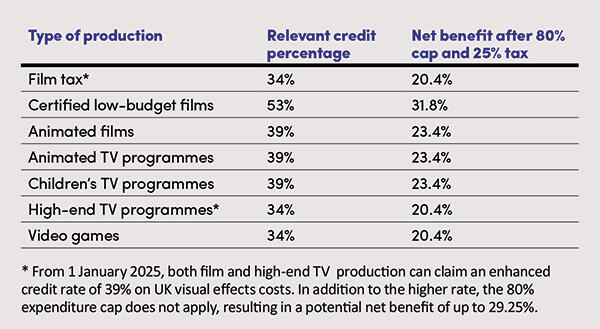

The first step in calculating the benefit available under the AVEC and VGEC regimes is to determine the total relevant global qualifying expenditure. Within that expenditure, all amounts used or consumed within the UK must be identified. A taxable expenditure credit is then applied at the relevant rate to the lower of the UK expenditure or 80% of the total global qualifying expenditure. (For certain visual effects work, an additional credit can be claimed.)

As noted earlier, the credit is recognised ‘above the line’ in the company’s financial statements – that is, as income rather than as a tax credit.

There are several steps in determining how the benefit is ultimately received, but it may take the form of either an offset against other tax liabilities or a payable credit (net of a notional corporation tax charge). Assuming that the full amount is available for offset or payment – and that all relevant expenditure is used or consumed within the UK – the net benefit to the company is shown in the table below.

Key qualifying criteria

To qualify for relief, the production must be certified as British, have at least 10% of its core expenditure incurred within the UK and meet specific criteria depending on the relief in question. The main qualifying requirements are as follows:

Films: The production must be intended for theatrical (cinematic) release. To qualify as certified low-budget films and obtain the enhanced credit percentage, productions must satisfy two further tests:

- the total core expenditure must not exceed £23.5 million; and

- the film must have either a UK writer or director, or qualify as a co-production.

Animation: The completed production of films or TV programmes must include animation, and at least 51% of the total core expenditure must relate to the completed animation.

TV programmes: TV programmes must be produced for television or online broadcast by the general public. To qualify as children’s TV programmes, when production begins it should be intended primarily for an audience under the age of 15; and competitions may be included provided the total value of prizes does not exceed £1,000.

High-end TV programmes: Including dramas, comedies and documentaries, these must have an average core expenditure of at least £1 million per hour of slot length, and each episode must have a minimum slot length of 20 minutes.

Video games: The game must be intended for supply to the general public. It should allow player interaction that meaningfully influences the outcome, and the result must not be predetermined. Games produced for advertising, promotional or gambling purposes are excluded, although in-game advertising does not disqualify a production.

Exclusions: Certain types of television programmes are specifically excluded from qualifying for relief. These include advertisements, as well as news, current affairs or discussion programmes. Quiz shows, game shows, panel shows, variety shows, chat shows and similar formats are also excluded. Programmes that include competitions or contests do not qualify, nor do broadcasts of live events or theatrical or artistic performances that were not created primarily for filming – although other reliefs may sometimes apply in these cases. Finally, programmes produced for training purposes are not eligible.

BFI Certificate

For any of the qualifying claims outlined above, a cultural certificate must be obtained through the British Film Institute (BFI). The Secretary of State for the DCMS certifies productions based on the advice of the BFI Certification Unit. Certification is awarded either for qualifying co‑productions or for productions that meet the relevant cultural tests – although for video games, certification can only be granted based on the cultural tests.

The cultural tests operate on a points-based system, with points awarded for factors such as cultural content, cultural contribution, use of UK cultural hubs and personnel. The number of points required to qualify varies by production type. Interim certificates may be granted while a production is still in progress, but a final certificate must be obtained on completion. In some cases, an Accountant’s Report must also be submitted to the BFI.

Although tax advisers can assist with this process, the claimant is often best placed to complete the questionnaire, as they will have the most detailed understanding of the production’s creative and operational aspects.

Cultural reliefs

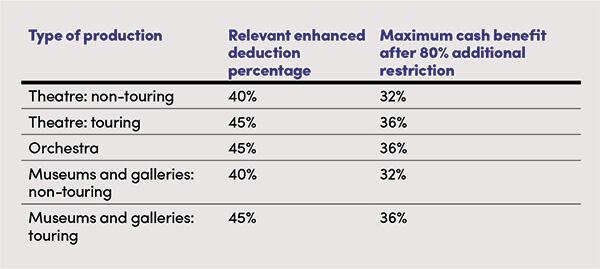

Additional tax reliefs are available for qualifying expenditure incurred on theatrical performances, orchestral performances, and museum or gallery exhibitions. The mechanism for these cultural reliefs has remained consistent in recent years; however, the applicable rates have changed. Initially increased on a temporary basis to provide support through the Covid-19 pandemic, these enhanced rates were made permanent from 1 April 2025, rather than reverting to their pre-pandemic levels. The permanent rates are shown in the table below.

Practical issues

It is essential to ensure that the company qualifies for the relevant relief, as the legislation applies specifically to companies that are primarily responsible for the qualifying production. It can be advantageous to establish a separate legal entity to manage the project and claim the relief. This approach should always be evaluated with specialist accounting, legal and tax advice.

Each qualifying production should have its own profit and loss account, clearly identifying all income and expenditure associated with that production. Since many projects span several years, claims can be made as expenditure is incurred and must be calculated on a cumulative basis, making financial tracking essential throughout the production’s lifecycle.

Claimants must also comply with specific administrative requirements. Relief claims must be included within the company’s tax return, and an Additional Information Form must be submitted to HMRC before the return is filed. This form provides further details about the claim and the associated productions, and timely, accurate completion is critical to ensure the relief is processed correctly.

Conclusion

These generous incentives have played a crucial role in strengthening the UK’s creative sector. For many claimants, they now represent an integral component of forecasting and budgeting, showing that the legislation has successfully nurtured and encouraged growth within these industries.

The introduction of the AVEC and VGEC regimes, alongside the government’s ongoing engagement with industry stakeholders, reflects a sustained commitment to supporting creativity and production in the UK. As a result, enhanced reliefs for low-budget films, visual effects and animation have been introduced, becoming key tools in retaining talent and production activity within the country.

Given the potential value of these incentives, it is vital that claims are accurate and well-prepared to ensure prompt approval by HMRC. As outlined, there are numerous qualifying criteria to consider – not only for the claimant company but also for each underlying project and the related expenditure.

Complexities and areas of uncertainty are inevitable. Calculating cumulative expenditure across a long-term production can be challenging, as can determining what constitutes UK expenditure in certain scenarios. Questions may also arise where the purpose of a production changes mid-course or if it is abandoned entirely. In such cases, professional advice from tax and creative sector specialists is invaluable to ensure compliance, maximise available reliefs, and navigate the finer details of the legislation effectively.

© Getty images