Looking closely

Share this article

Neil Warren considers the VAT issues relevant to an accountancy practice that decides to sell a commercial building that it owns

Key Points

What is the issue?

In most situations, VAT will be charged by a property owner if he sells his building and has made an option to tax election on the property in question. But there are situations when the option is overridden, e.g. if the buyer intends to convert it into dwellings or use it for a relevant residential or charitable purpose. The sale might also avoid a VAT charge if it is sold with a tenant in place, i.e. as a TOGC.

What does it mean to me?

There are large amounts of VAT at stake when a business buys and sells property so it is important to be clear about the rules for both charging output tax and claiming input tax. If a building is sold as exempt from VAT, this could have implications for input tax claimed by the seller, e.g. because of capital goods scheme adjustments.

What can I take away?

Any VAT issues concerning a property sale need to be considered before a deal takes place, i.e. as a planning exercise. The VAT outcome depends on known facts at the time of the supply and this cannot be changed with retrospective action.

To pick up the story from the first article I wrote on VAT and property (‘Working it out’, Tax Adviser June 2018), Duran and Co Accountants bought the freehold of a property (plus VAT) and traded from the building for three years, before renting it out to a firm of solicitors following their relocation to a new site. It is now two years later, and the partners have decided to sell the building. They opted to tax the building before the solicitors started their tenancy arrangement.

Convert building into residential use

Let us firstly consider the situation where the solicitors have ended their rental agreement, so Duran and Co is selling a vacant building. As an opening question, can you think of two situations when the sale will be made without adding 20% VAT, despite Duran’s option to tax election i.e. the sale will be exempt rather than standard rated?

The first situation is if the buyer intends to convert the building into dwellings or a building that will be used for a ‘relevant residential purpose’ (RRP). The latter relates to use as e.g. an elderly persons home, student or nursing accommodation. In other words, a change from commercial to residential use is planned for the building. The buyer will issue form VAT1614D to the seller, which confirms his intention to convert the building into dwellings or for RRP use. The form must be issued before the price of the deal is legally fixed, i.e. before exchange of contracts (VAT Notice 742A, para 3.4).

Here are the answers to some questions that you might be asking:

- If I am the buyer, must I have obtained planning permission to convert the property into dwellings before I can complete form VAT1614D? The answer is ‘no’ because it is all about your intention at the time of the deal. The actual statement you will be signing is Condition 2 of the form, which says: ‘I intend to convert the building or part of the building mentioned above with a view to it being used as a dwelling or dwellings or solely for a relevant residential purpose’.

- What if my intention as the buyer is to only convert part of the building into dwellings? The good news is that the seller’s option to tax election can be partly overridden to reflect the residential use but VAT will still be charged on the commercial element. There is no specified method of output tax apportionment in the legislation but it must be carried out on a ‘fair and reasonable’ basis e.g. a square footage or floor split calculation. So if one floor out of two will still be used for commercial purposes, a VAT charge on half of the selling price will be appropriate.

- If I change my mind after I have bought the building and never convert it to residential use, will I have to repay the VAT I saved? The answer is ‘no’ – it is all about the buyer’s intention at the time of the supply. If these intentions are genuinely stated, there will be no comeback if the buyer changes his mind in the future about his use of the building.

Charitable use

The second situation when Duran and Co’s option to tax election will be overridden is if the buyer is a charity and intends to use the building or part of the building for a ‘relevant charitable purpose other than as an office.’ In this situation, there is no official HMRC form to complete, so the charity will confirm its intention to the seller in writing.

The phrase ‘other than as an office’ basically means that the building will not be used by the charity for head office type functions e.g. dealing with the charity’s accounts, administration, IT issues etc. However, if the office use is, for example, to provide a base for staff operating a telephone helpline service to assist people in need of support, this is not a problem (VAT Notice 742A, para 3.5).

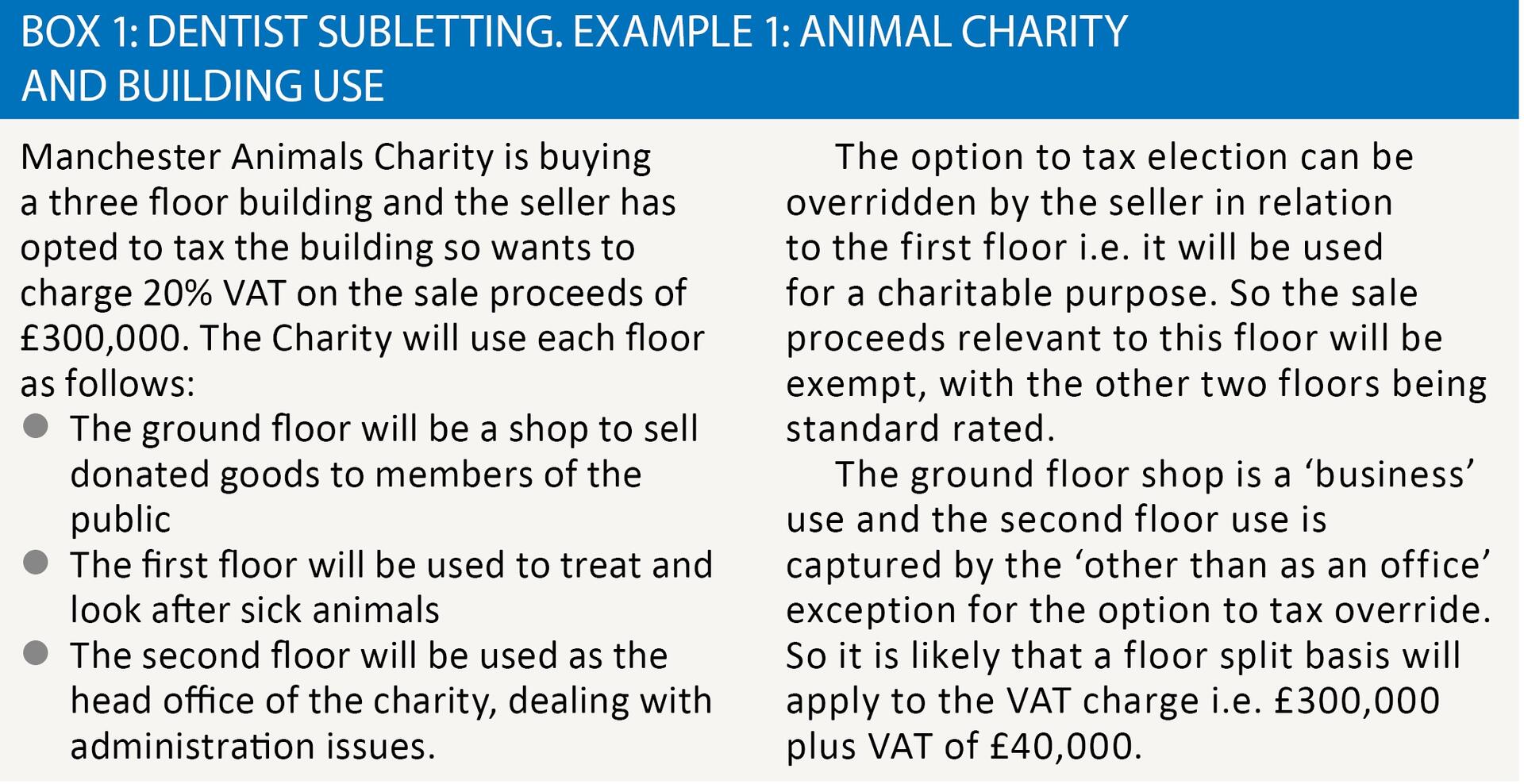

With regard to the ‘part of the building’ issue, it is important that the relevant use of the building can be clearly defined for each specific area – see Example 1: Animal Charity and building use.

Transfer of a going concern (TOGC)

We have so far considered the potential VAT issues with the building being sold as vacant but what would be the situation if it was sold with a tenant or tenants still in occupation i.e. the solicitors in our case study. The sale will be outside the scope of VAT as a TOGC as long as the deal meets certain conditions:

- The buyer will need to be either VAT registered or liable to be registered at the time of the deal.

- If the seller has opted to tax the property, the buyer must also opt to tax the property before the deal takes place i.e. form VAT1614A must be completed and submitted to HMRC’s Option to Tax Unit in Glasgow.

- The buyer must also confirm to the seller in writing that the option to tax election he has made will not be disapplied. This is an anti-avoidance measure – see VAT Notice 700/1, para 2.4.2.

The rental arrangement must be carried out on a proper commercial basis i.e. there is a genuine ‘property rental business’ in place at the time of the transfer. I recently dealt with a query where the tenant was only paying a peppercorn rent to the landlord, which did not constitute a business, so there was no scope for a TOGC.

Here is a teaser for you: what would be the VAT position if a ten floor building was being sold by a seller who had an option to tax election in place, but only one out of the ten floors had a tenant in place at the time of the sale i.e. nine floors were sold with vacant possession? Your initial thought might be that there is scope to treat 1/10 of the selling proceeds as a TOGC but the good news is that all proceeds will qualify as long as the conditions above are met. The HMRC guidance refers to this situation as a ‘partially let building’ and it makes no difference what the split is between tenanted and vacant. VAT Notice 700/9, para 6.2.

Capital goods scheme and TOGC

There is a twist to the tale for our buyer if a TOGC situation applies, namely that he will take over any remaining capital goods scheme (CGS) adjustments of the seller. You may recall from my first article that Duran and Co bought the property for £600,000 plus VAT five years ago, so this is within the scope of the scheme because the cost is more than £250,000 excluding VAT and the relevant adjustment period for land and property is ten years. So this means that input tax of £120,000 is reviewed by Duran and Co over a ten year period to reflect any change in use between taxable and exempt activities (and non-business activities as well since January 2011). So if Duran and Co bought the property in 2008 or later i.e. less than ten years ago, then some intervals are still outstanding for the buyer in the event of a TOGC. But as long as our buyer continues to use the building wholly for taxable purposes, the remaining annual adjustments will be ‘nil’ so no extra VAT is payable.

Input tax issues for seller

If a taxable business is sold as a TOGC, there are no input tax issues for the seller i.e. there are no partial exemption challenges. But if our imaginary property is sold as exempt or partly exempt because of the charitable or residential use issue, then input tax needs to be considered. The first challenge will be for Duran and Co to be aware that an exempt sale of the property will mean that any remaining intervals of the CGS will be treated as exempt rather than taxable. So if the business bought the property in 2015 for £600,000 plus VAT and sold it as VAT exempt in 2020 because the buyer is converting the property into dwellings, Duran and Co will have to repay half of the input tax i.e. the final five years of the ten year adjustment period are treated as being relevant to exempt activities because the property sale is exempt.

The second input tax challenge for a seller is to recognise that any costs that directly relate to an exempt property sale will also be input tax blocked under the rules of partial exemption e.g. estate agents fees, solicitors costs etc.