Working it out

Share this article

Neil Warren considers the VAT challenges facing an accountancy practice buying a property for use in its business, which it then rents out three years later when it relocates to new premises

Key Points

What is the issue?

When a business buys a building and pays VAT, input tax recovery depends on its use of the building, e.g. whether this is for taxable or exempt activities. An option to tax election does not need to be made by the buyer just because the seller had an election in place at the time of the sale. It is also important to be aware of the 20 year period, after which an election made with HMRC by a taxpayer can be reversed.

What does it mean to me?

There are large amounts of VAT at stake when a business buys and sells property so it is important to be clear about the rules for claiming input tax and when input tax might need to be repaid to HMRC if the use of the building changes, e.g. from generating taxable income to exempt rental income. Any errors can be corrected by HMRC going back four years.

What can I take away?

The capital goods scheme requires input tax on some property expenditure to be adjusted over ten years – this can create many challenges for property owners. An awareness of the scheme is important to avoid a potential problem. And be aware that SDLT is always charged on the VAT inclusive price of a property, so a sale without VAT will produce a tax saving.

VAT and property challenges are often best explained with a practical case study. It gives the chance to more easily explain the quirks of the legislation and, as many advisers know, there are many potential traps with this massive subject. So in the first part of a two-part article (the second part will be in a future issue of Tax Adviser), I will look at the ‘VAT life of a property’ for a commercial business, i.e. by considering the purchase of the building, its use by the business and subsequent sale. By the time you have finished reading the articles, you might advise your clients to rent rather than buy property to avoid the potential VAT headaches!

The case study

Let me introduce you to Duran and Co Accountants who, as it says on the tin, offer accounting services to clients. In other words, their business is fully taxable as far as the nation’s favourite tax is concerned and they have no input tax block. The business trades as a partnership and it has just bought the freehold of an office in the village of Spandau for £600,000 plus VAT, which will be occupied by the partners and all staff. What are the VAT issues to consider?

Why is VAT being charged?

As a starting point, the purchase of the freehold of a non-residential building is usually exempt from VAT, with two main exceptions:

- The building is less than three years old, so is standard rated by statute, i.e. an override to the exemption for land supplies in VATA1994, Sch 9, Group 1.

- The seller has made an option to tax election on the property so needs to charge 20% VAT on the selling price.

Let us assume that the second situation applies to the property in Spandau, i.e. VAT is being charged because of the seller’s option to tax election and not because the building is less than three years old. Here are some important tips:

- Duran and Co will be able to claim input tax on the purchase of the building because it will wholly use it for taxable purposes.

- It is important that proof of the seller’s option to tax election with HMRC is acquired before exchange of contracts. This is because a business can only claim input tax on correctly charged VAT.

20 year rule

There is another question that Duran and Co should ask the seller: did you opt to tax the property more than 20 years ago, and therefore can you reverse the election by submitting form VAT1614J to HMRC, before the sale takes place? If so, it can then be an exempt, sale i.e. avoiding the 20% VAT charge.

You might wonder why this is necessary when Duran and Co can claim input tax anyway. There are two reasons:

- SDLT is charged on the VAT inclusive price of the deal – so there is a tax saving here if the sale excludes VAT;

- There is a cash flow challenge for the buyer, i.e. paying VAT to the seller and waiting up to three months to claim input tax on a VAT return.

The reason I often give the 20-year rule its moment in the VAT spotlight is because with each passing day, more elections will have passed the 20-year period and therefore can be reversed. However, don’t forget that the key date is 20 years from when the seller’s option to tax election took effect, and not 20 years from when he bought the property.

To give a balanced argument, our seller needs to check his own VAT position before submitting form VAT1614J to HMRC. If the sale of the property is exempt from VAT rather than standard rated, this might cause him a problem with the capital goods scheme (CGS), if he either bought the property within the previous 10 years at a cost of £250,000 or more excluding VAT, or has spent more than this amount on either an extension, improvement or refurbishment project. In these situations, the input tax initially claimed on the expenditure is adjusted over a 10-year period with annual adjustments. So if our imaginary seller bought the property five years ago for £300,000 plus VAT and claimed input tax because of his taxable use, an exempt sale of the property to Duran and Co will, all things being equal, lead to a £30,000 input tax adjustment. This is because the sale of the building will mean that all remaining intervals (to complete the ten) will be deemed to be relevant to exempt rather than taxable use (HMRC Notice 706/2, para 9.1).

Option to tax myth

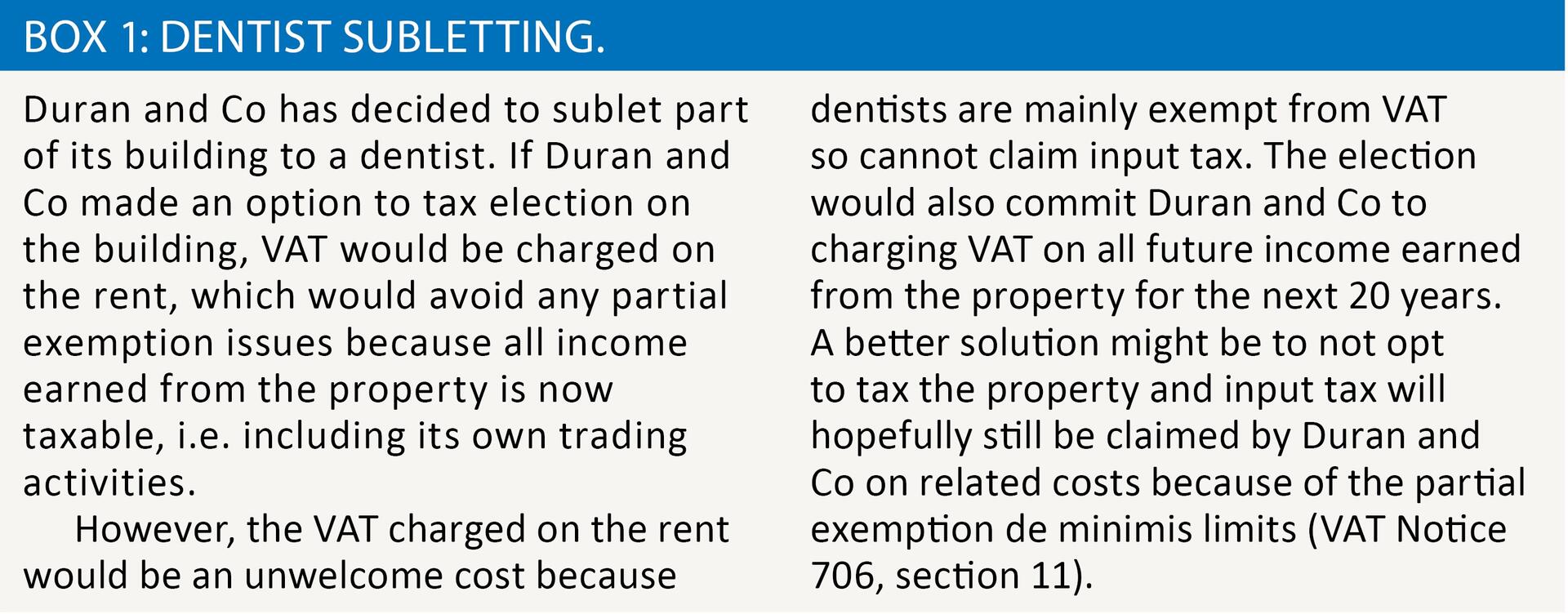

There is a myth in the VAT world that if a seller has opted to tax a property, the buyer must also opt to tax the same property as a condition of claiming input tax. This is not correct: in our example, Duran and Co will be able to claim input tax because the property is being wholly used for taxable purposes. There is no such thing as an opted property – each taxpayer makes a decision as to whether an option to tax election is in their best interests. See Box 1: Dentist subletting.

Property rental

To continue the story, Duran and Co bought the Spandau office in 2015. It is now 2018 and the partners have decided to relocate to another site, so will rent it out to generate long term income. There are three potential tenants: a charity wants to use it as a place of worship; a betting shop for its head office function; and a firm of solicitors. Which tenant would you recommend as far as VAT is concerned?

Before this question is answered, it is necessary to again consider the CGS, i.e. because Duran and Co bought it less than ten years ago at a cost of more than £250,000 excluding VAT. So there are still seven annual adjustments outstanding, which is now relevant because the use of the building has changed from making taxable supplies of accountancy services to the exempt activity of earning rental income. The input tax to adjust each year is £12,000, i.e. total VAT paid on the purchase price of £120,000 divided by ten years. So wholly exempt use of the building in the next seven years will lead to £84,000 of input tax being repaid to HMRC. However, the good news is that an escape plan is available.

Option to tax election

The easy way for Duran and Co to avert a problem with the CGS is to opt to tax the property with HMRC before a tenant is found, so that the rent will be subject to VAT. This means that the building will continue to be used by the partnership for taxable activities, so it does not need to consider the complex issues of either the CGS or partial exemption. Input tax can also be claimed on any ongoing costs associated with the property, e.g. agent fees, repair costs, advertising costs to find a tenant etc. Duran and Co will notify the election to HMRC on form VAT1614A.

So going back to our choice of tenant, the VAT charge to the betting shop will be as welcome as rain in Manchester on a Bank Holiday weekend, because its activities are exempt from VAT so it is input tax blocked on its costs. And care is needed with the charity: if a charity uses a building for a ‘relevant charitable purpose other than as an office’ (such as a place of worship) it can ask the landlord to override his election and make the rent exempt again. (VAT Notice 742A, para 3.5.) So it is reasonable to conclude that the most VAT efficient solution will be to agree a tenancy with the solicitors because they can claim input tax on their costs.

Conclusion

The election made by Duran and Co has averted a VAT problem but it is important to recognise that an election is not a ‘win win’ in every situation. As explained above, an election made by a taxpayer on a property remains in place for 20 years before it can be reversed, so this could be a problem for Duran and Co if future tenants cannot claim VAT, e.g. a bank or betting shop. The election will also apply to the future sale of the building in most cases and I will consider these VAT issues in my next article.