Making a sacrifice

Share this article

Vaneeta Khurana and Tony Nevin explain what optional remuneration (or salary sacrifice) means for employers

Key Points

What is the issue?

New legislation will be introduced from 6 April 2017 under ‘optional remuneration’ to limit the tax and NIC advantages currently available under existing salary sacrifice arrangements.

What does it mean to me?

Employers will need to review the way in which benefits are currently provided and ensure the benefits which are ‘exempt’ are tax and NIC compliant.

What can I take away?

Employers must take action to review current benefits/remuneration policies and communicate the change and its impact to employees.

The Government for some time has been concerned about the way in which the provision of benefits has evolved over the years with a growing market for flexible benefits, often combined with salary sacrifice arrangements. It recognises that such arrangements allow employers to attract and retain employees as part of their overall remuneration package in a very competitive and diverse employment market. However, it has stated that such arrangements both represent an increasing cost to the Exchequer and create inequality between employees and employers who benefit from the tax and National Insurance Contributions (‘NIC’) advantages, and those that don’t. There is particular concern about employees close to the National Minimum or Living wage or unable to participate in such arrangements.

A Government consultation document issued on 10 August 2016 proposed to limit the range of tax and NIC-advantaged benefits in kind that may be provided in a remuneration package. As a result, from April 2017 the ITEPA 2003 Act will include new sections 69A and 69B and consequential amendments in other sections. The term ‘salary sacrifice’ is not mentioned at all in the draft legislation which refers throughout to ‘optional remuneration’ arrangements (‘OpRA’) but ‘salary sacrifice’ remains in existing legislation, so the Government must be presumed to feel that the different name is necessary to avoid confusion.

What is OpRA?

OpRA covers circumstances where the employee:

(A) gives up a present or future right to receive earnings in order to receive a benefit; or

(B) is given the option of receiving a benefit or earnings, i.e. additional earnings, for example flexible allowances exchangeable for cash (something that wasn’t made clear in the consultation document).

In either case, the employee is taxable on the amount ‘forgone’. In type A arrangements, the amount forgone is the amount or value of earnings given up and in type B arrangements the amount forgone is the amount or value of earnings offered to the employee instead of the benefit.

So, what are the new rules?

From April 2017, where under OpRA benefits are provided the income tax and Class 1A NICs chargeable value of the benefit will be the greater of:

- the amount of earnings that the employee would have received if they had not taken the option of receiving the benefit; and

- the otherwise taxable ‘cash equivalent’ value of the benefit in kind.

- The employer will have to deduct income tax and pay employer’s Class 1A NIC on the value of the optional remuneration.

Exemptions

Employer-provided pensions (including advice), death and retirement schemes, childcare, cycles and cyclist’s safety equipment provided under cycle-to-work schemes and ultra-low emissions vehicles (ULEVs- vehicles whose emissions do not exceed 75 gm/km) will all be exempted from the optional remuneration rules.

The Government has no present plans to tax salary sacrifice in return for intangible benefits such as additional annual leave or flexible working hours.

Reconciling OpRA with the benefits code

Specific rules will be introduced, designed to ensure that optional remuneration applies to all salary sacrifice cases and exemptions in the benefits rules do not override them and so nullify their effect.

The special case exemption applies to the following (this is not an exhaustive list):

- reimbursed expenses;

- independent advice in respect of conversions and transfers of pension scheme benefits;

- subsidised meals;

- recommended medical treatment; and

- trivial benefits.

So, what benefits will be impacted?

Whilst there is a list of exemptions and exclusions, the main benefits that, in our experience are typically provided by many employers that will be affected by the new rules are:

- health assessments

- mobile phones

- technology (such as iPads, android devices etc.)

- cars

- car parking

- own goods/ products

HMRC’s response to the consultation document also makes reference to ‘…white goods, concierge services and double glazing’, which are not the norm based on our experience.

Transitional measures

Following consultation the draft Finance Bill includes transitional measures which also open the (double glazed?) window for new arrangements to be made before 6 April 2017. The new rules only apply to new arrangements made on or after that date but existing arrangements will become subject to the new rules at the earlier of:

- the end, change, modification or renewal of the contract;

- 6 April 2018 for benefits other than for cars, vans and fuel, accommodation, and school fees;

- cars, vans and fuel, accommodation, and school fees will be brought into the new rules from 6 April 2021.

Practical problems

HMRC still needs to clarify a number of issues including when the arrangement is considered to have been entered into. For example, if a car is selected by an employee under a salary sacrifice arrangement in March 2017 it may not be delivered for three months – at which point the reduction in salary occurs via the payroll. At which point is it considered that the salary sacrifice has been entered into, on selection i.e. when the employee agreed to vary its terms of employment, or when the reduction in pay takes place?

It is worth noting that as salary sacrifice agreements (variation of contracts) fall under employment law and in the absence of specific legislation will HMRC have to base its decision on when an agreement is in place based on contract law?

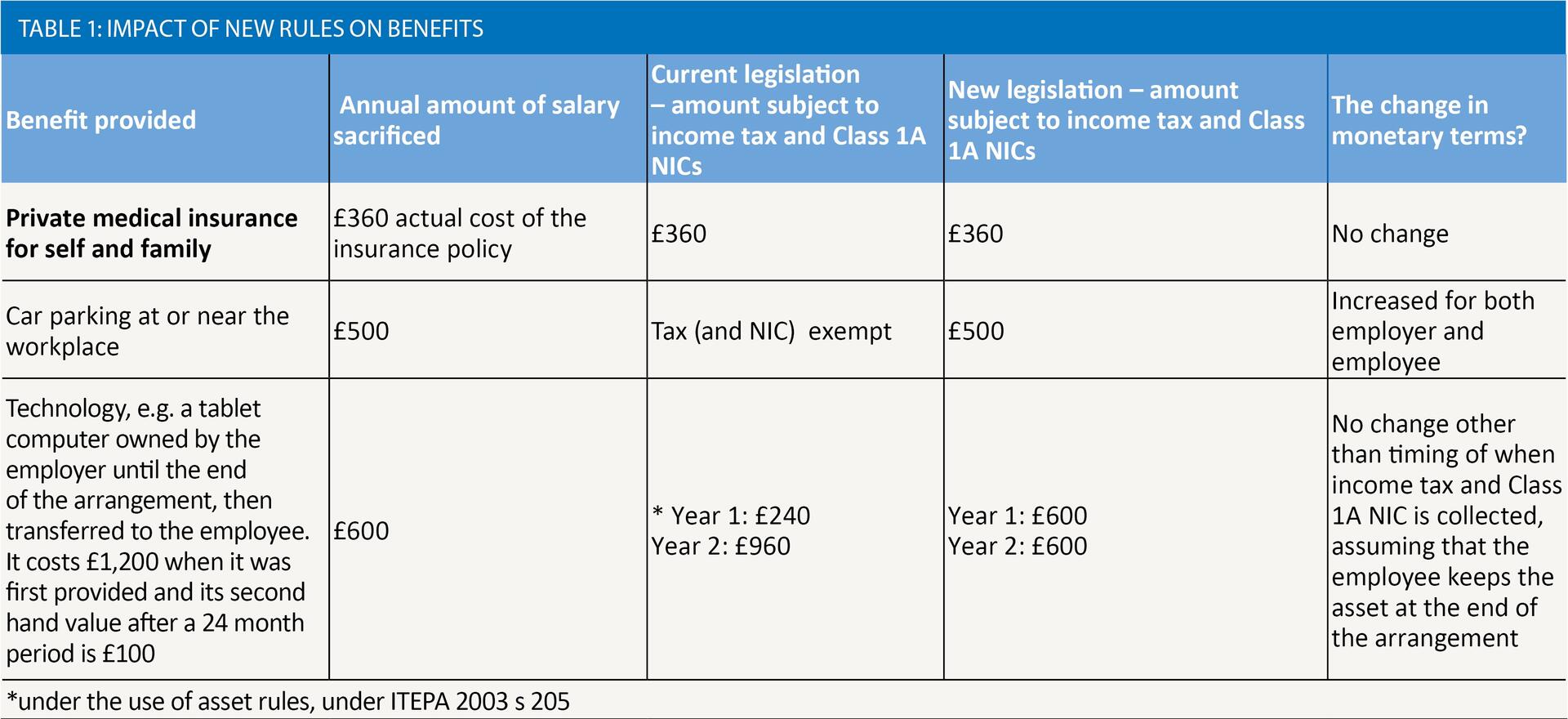

Three examples have been provided below where benefits have currently been provided by way of a salary sacrifice arrangement, to illustrate the impact of the new rules. Cars are covered separately. See table 1.

Cars: Where employers provide cars by way of a salary sacrifice arrangement, and the arrangement is in place before 6 April 2017, these are effectively protected until April 2021 under the transitional rules unless the contract is varied. As already mentioned, when an arrangement is deemed to be in place it needs to be clarified. We think that this can be when an order is placed subject to the wording surrounding the contractual commitment by all parties that the arrangement is an OpRA.

In most cases currently, employees select cars where the income tax and NIC on the amount of salary sacrificed saved outweighs the benefit in kind tax charged via the P11D process. Therefore, under the new legislation, these arrangements will almost certainly leave both employees and employers with increased costs as it removes any employee income tax and employer NIC advantage on the difference between the amount sacrificed and the benefit in kind value.

What do employers need to do now?

Step 1: Review

Employers need to review compensation and benefits policies in line with the changes and assess the financial impact. This will mainly be an issue for employers with substantial levels of optional remuneration: some will need to take a view on whether the cost of reviewing existing arrangements would outweigh the potential saving.

Step 2: Assess what options are available

Having completed any necessary review, employers will need to look at their options, remembering that pre-6 April 2017 vehicles and fuel, accommodation and school fees arrangements are being grandfathered, and considering other commercial reasons for salary sacrifice arrangements, particular to the employer.

Step 3: Communicate

It is important that the changes are communicated effectively and positively with employees. There is lots of press announcing the death of salary sacrifice so employees need to know the facts, what it will mean for them financially, and the plan of action.

Conclusion

Optional remuneration creates significant changes that can vary from sector to sector. It is an established employee remuneration practice that can offer choice and flexibility in today’s diverse workforce and support employees’ individual lifestyles. At the same time, it offers savings to both employers and employees which may not be available going forward.

The closing date for comment on the draft Finance Bill clauses was 1 February and the 2017 Finance Bill can be expected to be brought to Parliament in late March following the 8 March Budget.