Making a withdrawal

Share this article

Peter Mills provides guidance on changes to dividend taxation and how they affect profit extraction for SMEs

Key Points

What is the issue?

Over the past decade a discrepancy has arisen between effective rates of tax for different means of profit extraction, with dividend extraction becoming the default mechanism. Profit extraction continues to be a fundamental question for SME owners and last year’s changes to taxation of dividends have reinvigorated the debate.

What does it mean to me?

The changes gave us a refreshing opportunity to revisit the question and it remains important to be proactive and work closely with clients to design and implement extraction strategies that continue to work effectively in the context of their wider personal circumstances.

What can I take away?

It has become increasing important to ensure a profit extraction strategy is tailored and bespoke and careful consideration of a clients’ personal situation can add real value in helping them maximise the return on their business activities.

What is profit extraction?

How to extract profits from a business remains one of the fundamental questions facing owner managers and, as tax advisers, we are often asked to consider the most effective way of returning business profits to the owners.

The question continues to be relevant and whilst, simplistically, changes in legislation effected by Finance Act 2016 mean more tax to pay for the majority of SME owners they also provide a refreshing opportunity to reassess the effectiveness of existing extraction strategies.

Key legislative changes

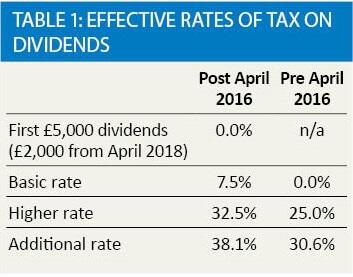

From 6 April 2016, the rules governing taxation of dividends were reformed, with the abolishment of the 10% dividend tax credit and imposition of a 7.5% increase in the effective rates of tax on dividends. As small compensation, Finance Act 2016 also introduced a £5,000 dividend ‘allowance’ (although that was scheduled to reduce to £2,000 before the announcement of the general election and may well do so depending on the otcome) amongst other new allowances for savings income.

The rates of tax on dividends, before and after the change, are set out in table 1.

Business structure and incorporation

Although the question of profit extraction is one that is often limited to consideration of the corporate shareholder, last year’s changes to taxation of dividends have broader consequences for the debate about whether a company is, in the first instance, an effective vehicle through which to operate.

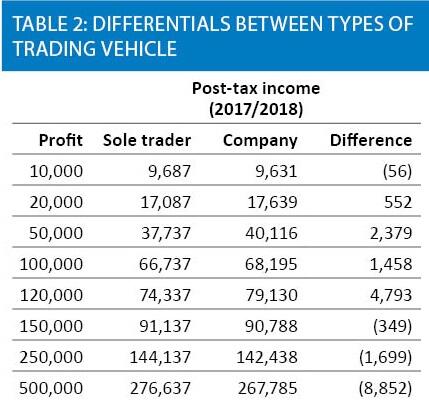

There is an apparent and continued intention from the government to align the effective tax position of a private individual and a company and, although the position will alter slightly as corporation tax rates reduce further from 2020, table 2 below illustrates the narrow differential, particularly at lower profit levels, between the two types of trading vehicle (the example is based on non-devolved tax rates).

Therefore, after taking into account the additional administrative costs associated with corporate ownership, an SME owner may well consider operating an unincorporated business to be more straightforward and cost effective.

Needless to say, whilst incorporation can be a relatively painless experience for a trading business, the limited capital gains tax reliefs available for disincorporation mean that existing business owners operating through a company are unlikely to be given sufficient incentive to disincorporate. There will also be other commercial factors that may increase the overall attractiveness of a corporate structure, including:

- Liability – corporate shareholders have limited liability.

- Perception – incorporation may improve perceived credibility.

- Other tax reliefs – certain tax reliefs (such as R&D relief, patent box, EIS) are only available to companies.

- Flexibility – companies give greater flexibility over remuneration strategy.

- Retention of profits –companies suffer a lower rate of tax on profits retained in the business.

Profit extraction for corporate owners

The options available for the corporate owner to extract profits are much more flexible than for a sole trader and it is therefore important to carefully consider all of the options available, in the applicable context, in implementing an effective strategy.

At its simplest, the question of profit extraction for the corporate owner results in a comparison between taking salary or extracting profits as dividends. As a general rule, the optimal position has always been to take a modest salary to the level of the NIC threshold and the remainder as a dividend. Whilst the comparable effectiveness of dividends was reduced after 6 April 2016, the conclusion is likely to remain broadly unchanged.

Having said that, it nonetheless remains important to tailor a strategy to the specific context. One exception that may be frequently overlooked is that of innovative companies making R&D claims where the shareholder has significant involvement in the R & D, who may find that the enhanced deductions available on salaries actually make this a comparably more attractive strategy.

Other less conventional alternatives may also be an option and company pension contributions, interest on loans and rent on privately held commercial property can all be effective ways to extract profits by removing the National Insurance obligation. Under current legislation these options have the added benefit that they avoid the monthly instance of tax that arises on PAYE income.

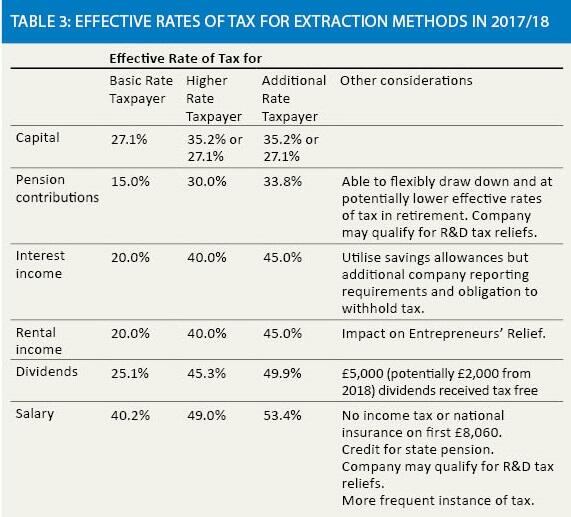

By way of a summary, the effective rates of tax applicable to various extraction methods, ignoring any specific allowances, are as set out in table 3.

It is clear that for those owners with surplus cash who have not utilised their annual pension allowance, and are still within their lifetime allowance, that pension contributions will usually be the most efficient method of extracting profits from a company. This is unlikely to be an ideal strategy for younger entrepreneurs who may be a number of years away from retirement, but could be effective especially where the owners are close to retirement anyway or if there is no immediate or foreseeable need for the cash. Referring to my earlier comment about R&D tax reliefs, pension contributions can also become even more effective when those costs qualify for R&D relief, given the enhanced corporation tax deductions.

Other extraction methods are only likely to be applicable in limited circumstances, but a full consideration of the wider personal situation can provide an opportunity to capitalise on the effectiveness of other methods. For instance, where individuals have lent money to a company but never considered charging interest or have retained a commercial property personally and not considered charging a market rent, in most circumstances extracting profits by these methods will be more effective than either a salary or dividends, although it is imperative to consider the wider ramifications, particularly of charging rent.

In addition, the array of allowances and reliefs available mean that careful structuring and planning can enable a single individual to draw down up to £22,500 in tax free income in 2017/18 and with the added benefit of securing a corporation tax deduction on the majority of that income. This can be achieved by taking a small salary up to the NIC threshold followed by interest to utilise the balance of personal allowance, the £5,000 savings allowance and basic rate allowance, with the remaining taken as dividends to utilise the £5,000 dividend allowance.

In addition, careful family planning can often open up further opportunities to minimise a structure’s overall exposure to tax, for instance through involving spouses and adult children in the business, where commercially appropriate, to utilise their personal and other allowances and lower rates of tax.

To give an example, consider the case of a married couple, one of whom owns 100% of a trading company but neither of them have any other income, and who give their adult child £10,000 a year as a contribution to university living.

Assuming they made corporate profits of £150,000 and extracted them all as dividends (except for an £8,060 salary each) their net income would be £95,904. If they were to split the shares between them and transfer a small amount of shares to their child so the income accrues directly, they could achieve a much more attractive £112,304.

Capital routes

Efficient planning throughout the business lifecycle is important but the holy grail remains the extraction of profits in a form that qualifies Entrepreneurs’ Relief, most notably a share sale or by a liquidation. However, the water has been muddied by the introduction of targeted anti-avoidance rules in April 2016 which potentially limit the benefit of a liquidation in certain circumstances. HMRC’s application of the new rules is still somewhat uncertain, and a more detailed consideration of their impact is a subject for another article.

Summary

From a high level, last year’s changes to dividend taxation are likely to result in additional tax to pay for owner managers but they also give us, as tax advisers, a refreshing opportunity to reassess the effectiveness of our clients’ existing extraction strategies. Profit extraction is an essential question for most business owners and the range of options available can make this not only a particularly interesting area on which to advise, but one in which careful consideration of client’s personal circumstances can add real value in helping them maximise the return on their business activities.