In the margins

Share this article

Neil Warren gives important tips on margin schemes and HMRC’s approach when record-keeping is poor

Key Points

What is the issue?

The opportunity for traders selling second-hand goods to account for VAT on the margin, instead of the full selling price, is an important opportunity in the legislation

What does it mean to me?

The record-keeping requirements for margin schemes are strict. Regular checks should be made to ensure that systems comply fully with HMRC Notice 718

What can I take away?

If HMRC consider that records are inadequate and that tax has been underpaid, they have the power to assess output tax based on selling prices rather than profit margins

Selling goods on the internet has increased dramatically in recent years. Many sales made by small and medium-sized enterprises are made through eBay and similar trading sites and often involve second-hand goods.

In general, small-scale traders need not worry about VAT because their total sales will be less than the annual registration threshold. However, businesses that are registered will need to account for tax on their sales. This article examines the VAT issues of selling second-hand goods, but also includes high street traders and internet activity, where the tax is payable on the profit margin in most cases, rather than the selling price.

Basic rules

The second-hand margin scheme has been an important part of the legislation since VAT was introduced in 1973, particularly for antique dealers and second-hand car traders, as well as businesses that deal in works of art and collectors’ items. There are several points to bear in mind:

- The sales value, rather than the profit margin, is relevant for VAT registration, with the exception of the tour operators’ margin scheme (known as TOMS in VAT speak).

- The opportunity to account for output tax on the profit margin, rather than the selling price, is a generous concession; the record-keeping requirements for second-hand traders are strict – see HMRC Notice 718, section 5. Dealers must keep a stock book showing the purchase and selling prices of each item they sell and strict invoicing requirements (for buying and selling) need to be met.

- In the case of a margin-scheme trader selling goods at a loss, there is no ‘loss relief’ to claim, such as when the profit on item A can be offset against a loss on item B. The loss on item B produces a ‘nil’ VAT liability. However, the ‘global accounting scheme’ section in Online sales below spells out exceptions.

- Goods purchased by a trader with VAT charged on the full selling price by the supplier must be excluded from the margin scheme; normal VAT accounting will apply to those items.

The key point to remember is that, if the conditions of the margin scheme are not met, HMRC have the power to assess output tax on the selling price of the goods, assuming they are not zero-rated or exempt.

The overhead problem

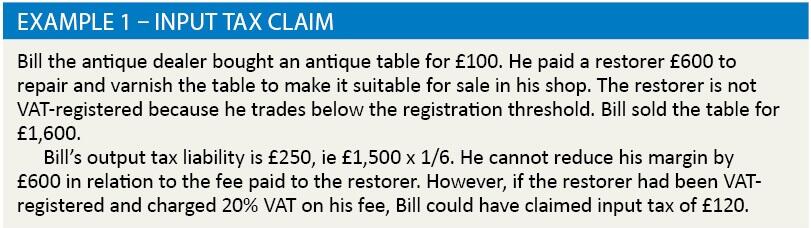

Going back about 25 years to my Customs and Excise days, I visited an antique dealer who prided himself on keeping immaculate records. ‘You won’t find a single error all day,’ he boldly predicted at the start of my visit. His comment about the quality of the records was completely accurate; but, as we all know, accurate tax declarations also rely on a correct understanding of the principles. Within 30 minutes of my arrival, his confidence had disappeared because I discovered that he was incorrectly dealing with charges made by his restorer (see Example 1). This is a key feature of a margin scheme – overhead items are treated separately and there is no addition to the purchase price for the goods.

Car dealer challenge

A practical query I recently dealt with involved a bookkeeper for a second-hand car dealer. When the business bought cars at auctions, the auctioneer sometimes charged a ‘buyer’s premium’ that did not include VAT. But at other times the premium was charged separately and added VAT at 20%. ‘Why was that?’ the bookkeeper asked, and how should she deal with the VAT, given the margin scheme?

The reason for the different treatment is because some auctioneers use a special scheme that treats their fees as VAT inclusive. According to HMRC Notice 718, para 11.3, car dealers must treat the two arrangements differently:

- the fee that charges VAT as a separate item is not included in the purchase price of the car as far as the margin scheme is concerned, but input tax is claimed separately by the dealer; and

- in the case of the ‘VAT inclusive’ buyer’s premium, the cost is added to the purchase price of the vehicle. This will reduce output tax payable when the vehicle is sold.

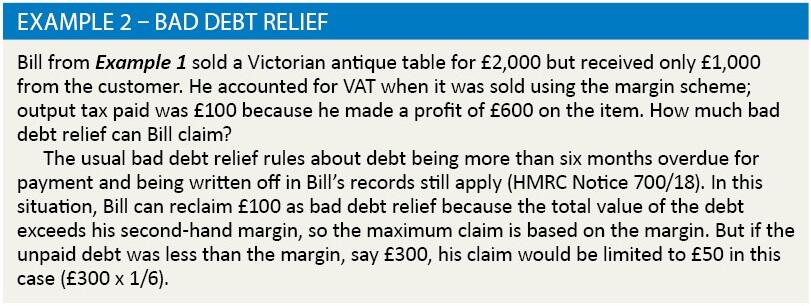

The other ‘margin scheme’ question I recently dealt with concerned a bad debt (see Example 2).

Online sales

How do we account for VAT if we sell second-hand goods on eBay, assuming we are registered? Let us assume that all goods are items of small value and they are all purchased from non VAT-registered suppliers – usually private individuals – or registered suppliers also using a margin scheme.

It would be impractical to keep a stock book to record every single item that is bought and sold. The saviour comes in the form of the ‘global accounting scheme’, which is intended for traders who sell a high volume of second-hand goods at low prices. The scheme does not apply to any goods that are bought for more than £500 – apart from when goods are broken down into smaller components and sold – and the individual items cost less than £500. This would include, for example, a car being broken up by a salvage business. The main features of the scheme are:

- VAT is payable at the end of a period based on the total margin, namely ‘total sales’ compared with ‘total purchases’. In effect, the scheme gives loss relief on any items sold below cost price. The scheme is also a winner for a business with increasing stock; that is because the ‘total purchases’ figure is not adjusted for opening or closing stock. But a business leaving the scheme must make a final adjustment for closing stock to reduce the ‘purchases’ figure.

- If a VAT period produces an overall ‘loss’, it can be carried forward and offset against future profits. This might occur in the first period of using the scheme because a value for opening stock can be included in the purchases figure.

- The record-keeping requirements are less stringent than with the second-hand margin scheme. No stock book is needed, for example. See HMRC Notice 718, section 15.

Dealing with HMRC

HMRC provide comprehensive guidance on second-hand schemes:

- VAT Notice 718 – the VAT margin scheme and global accounting. An important point to note is that the record-keeping requirements in the notice have the force of law.

- VAT Notice 718/1 – the VAT margin scheme on second-hand cars and other vehicles.

- VAT Notice 718/2 – the VAT auctioneers’ scheme.

- HMRC Guidance Manual – ‘VATMARG1000’ to ‘VATMARG13000’. This is the manual used by HMRC’s own officers, so it should be consistent with the approach they adopt on compliance visits.

But what if HMRC are unhappy with the records kept by a second-hand trader? Will they go back four years and assess tax based on selling prices instead of margins? The answer is that they do have the power to take this action. However, the officers should first consider whether they think VAT has been underpaid as a result of the poor record-keeping. If they are satisfied that tax has been correctly paid, it would be hoped that they issue a written direction about future record-keeping and use their discretion to accept the past declarations as correct. Even if they are not happy with the declarations, they should give the business owner time to bring the records up to standard. To quote from HMRC manual VATMARG10000:

‘If the non-compliance is serious or you are unable to verify the margin, consider if there are any reasons to assess immediately, such as time limits.

‘If not, give the trader the opportunity to reconstruct the records and warn that failure to do so may result in VAT being assessed on the full selling price of the goods. The trader is always to be given a reasonable amount of time to reconstruct the records; but in any event no longer than three months should be allowed.’