A matter of timing

Share this article

Neil Warren considers important time limits and deadlines that apply to certain land and property deals

Key Points

What is the issue?

An option to tax election sent to HMRC needs to meet important time limits; e.g. notified within 30 days of the decision to opt being taken. Advisers should also be aware of the six month, six year and 20 year opportunities to revoke an election, so that future property income is VAT exempt again.

What does it mean for me?

If a client changes their mind about a property project, meaning that intended taxable supplies will be exempt from VAT (or vice versa), the payback and clawback rules mean an input tax adjustment will be necessary for the previous six years.

What can I take away?

Certain builder services on residential property qualify for 5% VAT, including work on a dwelling that has not been lived in for at least two years. But third-party evidence of the empty period must be given to the builder to support the reduced VAT charge.

Timing is everything. This is a much-used phrase in today’s society and is often quoted in diverse subjects ranging from politics to sport. And tax, of course. A correct application of the VAT rules for land and property requires a UK business to get the timing right on many issues. I’ll share practical examples in this article.

Option to tax election

There are two stages to making a correct option to tax election with HMRC:

- Decision: A landlord or business owner with an interest in a property has incurred a large amount of input tax, which would be blocked under partial exemption if he didn’t opt to tax the building and charge 20% VAT on future supplies linked to the building; e.g. rental income or selling proceeds. He therefore decides that an option to tax election is necessary.

- Notifying HMRC: HMRC must be notified of the election in writing (usually by submitting form VAT1614A) within 30 days of the decision being made. But there is good news – this time period has been temporarily extended to 90 days due to the trading difficulties caused by Covid-19. HMRC will always acknowledge the election in writing, giving landlords an important document to support future VAT charged on either renting out or selling the building (see VAT Notice 742A para 4.1).

This leaves an obvious question, however. What happens if a landlord fails to carry out the above time deadlines correctly? Can HMRC be notified of an election retrospectively?

There is good and bad news here. If the landlord has carried out the ‘decision’ stage correctly, and is charging VAT on rent and claiming input tax on expenses, but has just failed to notify HMRC, the situation can be rescued. A belated election will usually be accepted by HMRC as long as proof of the ‘decision’ date is given; e.g. copies of sales invoices charging VAT to the tenants (see VAT Notice 742A para 4.2.1).

Revoking an election

Here is a quick question: how many separate occasions are there when a business can revoke an option to tax election with HMRC, once it has been made? The answer is three – with six month, six year and 20 year opportunities.

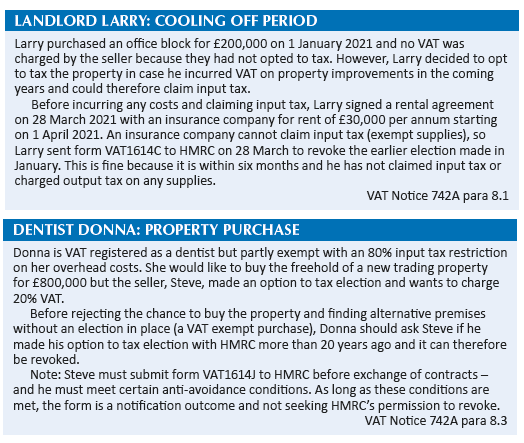

The six month window is often referred to as the ‘cooling off’ period – where a landlord realises that an election is not in his best interests. There is a specific form for the revocation (VAT1614C) and strict conditions need to be met. See Landlord Larry: cooling off period.

Imagine that you purchased a property on 1 January 2010 and opted to tax it, charging VAT on rental income and claiming input tax on expenses. You sold the property on 1 January 2013, charging VAT on the sale. It is now 1 January 2021 and you have decided to repurchase the same property. What are the VAT issues?

An important point with the option to tax rules is that elections made by taxpayers do not automatically end when they deregister or sell a property. Their election remains in place and this is important if a deregistered landlord sells the property in the future – he will need to re-register for VAT to ensure output tax is correctly charged. However, if the opter has not had an interest in the property for six years, the election is automatically revoked. In this case, the owner’s election ended on 1 January 2019, six years after the initial sale. The merits of making a new election would therefore need to be considered when the property is repurchased in January 2021.

Twenty year rule

The option to tax rules were introduced on 1 August 1989, so the first revocations were possible on 1 August 2009 with the 20 year rule. That date is nearly 12 years ago, so there are many elections that can now be revoked by landlords. Future income from the property will then be exempt, rather than standard rated.

An important fact is that buyers will often have more interest than sellers in an election being revoked, and it should be considered on every property deal. Even if a buyer can fully claim input tax, he or she still has the cash flow challenge of paying VAT and waiting up to three months to reclaim it on a VAT return. And stamp duty land tax is charged to buyers on the VAT inclusive price of a property deal. See Dentist Donna: property purchase.

Payback and clawback rules: six year window

Let me introduce you to Sally. She purchased a plot of land in Skegness in April 2016, with the intention of building a three-bed detached house to sell on the open market. This will be a zero-rated sale, so she registered for VAT straight away to claim input tax on building materials and professional fees. Builder services are zero-rated so there is no input tax to claim.

The certificate of completion was issued in April 2021 but Sally has now decided to rent out the house on a long-term basis, rather than sell it. What VAT problems does this create?

The answer is that her original input tax claims need to be adjusted with the ‘payback and clawback’ rules (see The VAT Regulations 1995 Regs 108-110):

- If input tax was claimed because of an intention to make taxable sales, it will need to be paid back to HMRC if the intention changes to the making of exempt supplies. Rental income from residential property is always exempt from VAT unless it relates to holiday lets. This is the ‘clawback’ rule and applies to Sally.

- If input tax was not claimed because of an intention to make exempt sales, it can be subsequently reclaimed if the intention changes to the making of taxable supplies. This is the ‘payback’ rule and the reverse of Sally’s situation.

- The rules depend on the first supply that is made by the taxpayer, and input tax needs to be included on the return that includes the date when the intention changed.

In the VAT world, we are used to working with a four year period for past errors on VAT returns; however, a payback and clawback correction is not an error – it is an adjustment. A six year time window is relevant here, so Sally will need to repay all input tax claimed, going back to the initial costs incurred when she first registered in April 2016.

As a final issue, if Sally intended to temporarily rent out the house, perhaps waiting for an upturn in the property market, she can review her input tax over a ten year life of the property. So, for example, if she intends to rent out for two years and then sell, 20% of the input tax would relate to exempt supplies and the other 80% would still be taxable.

For further details on this concession, which was introduced back in 2008 during the financial crisis, see VAT Notice 706 para 13.12.

Building supplies: two year empty period

The 5% VAT rate applies to some building services supplied on residential properties; e.g. work that converts a non-residential building into dwellings, such as an office block being converted into apartments.

It also applies if a project results in a change in the number of residential units; e.g. a detached house is converted into two semi-detached houses, or vice versa. It also applies if a dwelling has not been lived in for at least two years when the work begins.

The property owner must provide evidence of the empty period to the builder. This must be third party documentation, such as council tax statements, electoral register or housing office records – it cannot be a signed statement from the property owner saying it has been unoccupied for more than two years. There is no need for the owner to issue any signed certificate to the builder, only the relevant evidence (see VAT Notice 708 s 8).