Better together?

Share this article

The frozen VAT registration threshold means there is a big incentive for creating separate legal entities to trade below this limit. Neil Warren considers practical examples and the views of both HMRC and the courts

Key Points

What is the issue?

The VAT registration threshold has been frozen at £85,000 since 2017, and will continue unaltered until at least 2024. There is an incentive for growing SME clients to try to avoid registering by trading through two different entities, so that each entity gets a separate threshold.

What does it mean for me?

If a business split is not carried out properly – for example, record keeping and trading issues overlap – HMRC might seek to retrospectively register the entities as a single business, on the basis that they were never separate in the first place.

What can I take away?

It is important to ensure that business owners have a clear intention to create separate entities. Both entities must have a properly defined trading structure; for example, for invoicing arrangements and liaising with customers.

An undeniable outcome of the annual VAT registration threshold being frozen at £85,000 since 2017 is that more clients and advisers are interested in the controversial topic of business splitting. In other words, can we separate our business into two different legal entities, so that each entity gets its own VAT threshold? This potentially means annual VAT free sales of £170,000 – happy days!

For a service business making sales to the general public, or a business such as a restaurant that has zero‑rated inputs (food) but standard‑rated sales (meals), the incentive to stay out of the ‘VAT club’ is massive. In this article, I’ll consider the important question: where are we now as far as business spli tti ng is concerned?

Business splitting in practice

Imagine the following situation: Mario trades as a mobile hairdresser with annual sales of £60,000. He has decided to buy a salon as a going concern, which will be operated by staff rather than himself – it has annual sales of £130,000. Mario must immediately register for VAT as far as the salon is concerned. With a transfer of a going concern (TOGC), the buyer is treated as making the sales of the seller for the previous 12 months, meaning that he must register for VAT from his first day of trading because the historic sales are more than £85,000.

The problem for Mario is that if he buys the salon as a sole trader, his mobile hairdressing fees will also be subject to VAT – an annual loss of £10,000 with the output tax liability (£60,000 x 1/6). So, would it make sense for him to buy the salon in a different legal entity, perhaps a limited company where he is the sole or majority shareholder? The company will still need to register for VAT but his sole trader earnings are protected.

HMRC powers

HMRC has the power to treat two separate businesses as a single partnership if they are closely associated by ‘financial, economic and organisational links.’ See Legislation on business splitting. However, there are three important facts:

- HMRC’s power to correct the register applies from a current or future date, as long as the split has been carried out correctly. This means that each entity has separate bank accounts, trading names, self‑assessment tax returns, supplier accounts, separate circle of customers, etc.

- The key word in the legislation is ‘and’. HMRC must prove all three of the ‘financial, economic and organisational’ links and not just one or two.

- If the split has not been carried out correctly, with record keeping and trading issues muddled between the two entities, HMRC might retrospectively try to register the combined businesses for VAT, going back up to 20 years.

Case law

The courts have ruled against HMRC in a number of First‑tier Tribunal (FTT) cases in recent years, and I will highlight two lost by the department. Both structures had significant shortcomings in the argument that they were separate entities and both involved husband and wife partnerships.

In the case of Charles Caton v HMRC [2019] UKFTT 549, the issue in dispute was whether his sole trader business Commonwealth Café was separate from a restaurant run by his wife on the same premises called Waterfront Restaurant. Both entities traded below the £85,000 threshold but HMRC claimed that Mr Caton owned both businesses, with a combined turnover that exceeded the registration threshold between 2009 and 2016.

Factors that indicated there was only one business included the fact that there was a single website, and Mr Caton bizarrely said in a HMRC questionnaire that he owned the restaurant and his wife was an employee, and all card payments for both businesses were banked into Mr Caton’s account. They also shared the same washing up area and used the same main supplier.

However, Mrs Caton controlled the menu in the restaurant and each business had separate tills and staff. The key issue that persuaded the tribunal in favour of the taxpayer was a clear intention by the owners to run separate entities: ‘Mrs Caton wanted to “do her own thing rather than rely on John”.’ The appeal was allowed.

A similar victory came in the case of Graham Belcher v HMRC [2017] UKFTT 0427 (TC) for hairdressers Mr and Mrs Belcher. The Belchers even completed a partnership self‑assessment tax return but still managed to convince the court that they owned separate sole trader salons with their own sales. Each salon traded below the VAT registration threshold. The judge commented that there was ‘no conscious intention to run a single business in a partnership’.

Despite these taxpayer wins, it is better for splitting arrangements to be done properly in the first place, with all operational and accounting issues kept at arm’s length and on a commercial basis, rather than having to back pedal when HMRC comes knocking at the door.

Family challenges

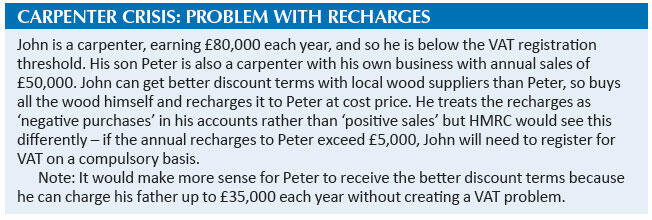

All inter‑trading between two closely connected entities must be carried out on an arm’s length basis; i.e. proper recharges are made for shared expenses and overheads. This outcome is harder to achieve when families are involved – there is not the same incentive to keep costs separate when money all belongs to the same family pot. The charging process can sometimes score a VAT own goal because it will increase the taxable sales of the business making the charges. See Carpenter crisis: problem with recharges.

Final challenges

The VAT issues are not clear cut. Advisers and HMRC might reach different conclusions on the same situation. Here are three practical scenarios – what is your view?

- Jack and Jill own a DIY store that is VAT registered as a partnership. They have decided to start a new venture, selling Christmas trees online. There will only be tree sales in November and December and total sales will be less than the VAT registration threshold. They decide to form a limited company for this activity.

- Landscaper John provides gardening services for private householders. His business has boomed and he is close to the registration threshold. He wishes to divide his business between a sole trader entity for ‘gardening work’ and a husband‑and‑wife partnership for ‘grass‑cutting services’, giving each customer separate invoices.

- Plasterer Mike operates as a sole trader and has formed a separate business with his wife for liquid floor screeding, keeping both entities below the registration threshold.

The verdict?

In my view, there is no problem with the tree proposal made by Jack and Jill. Selling DIY goods in a store is a very different activity to selling Christmas trees online. It will be easy to keep separate records and there will be a different circle of customers for each activity. However, there is clearly only one business activity for John, a garden maintenance service for private householders. He is on dodgy VAT grounds trying to make a split.

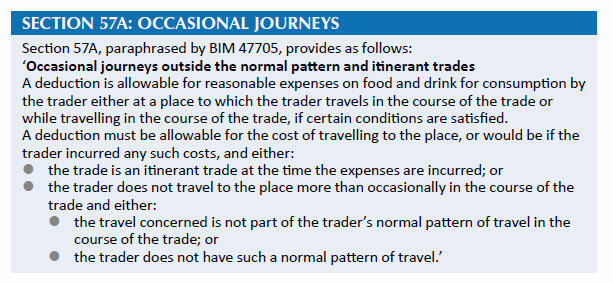

VAT enthusiasts might recognise the facts for plasterer Mike, which are based on the FTT case of Darren Vaughan v HMRC [2018] UKFTT 776, which was surprisingly won by the taxpayer in 2019.

Vaughan was a sole trader plasterer until 2012 but was then advised by his accountant to form a partnership with his wife for the screeding work to avoid a VAT registration problem; i.e. a business split was carried out. HMRC ruled that there had only ever been a single sole trader business and the combined turnover of both activities meant a registration date (retrospective) of 1 March 2013. The situation was not helped because there was confusion with purchase invoices being made out to the wrong business. The main conclusion of the judge was that the Vaughan family ‘did intend to separate the appellant’s existing sole trader business into two businesses’.

Final thoughts

In each of the taxpayer wins above, the judge made a comment about the importance of what the business owners intended to do;

i.e. to create separate entities. This conclusion about intentions seemed to be given more priority than some of the practical shortcomings, such as the muddling of purchase invoices in the Vaughan case.

So, as a practical tip, make sure that your clients are clearly focused in their mind about the commercial reality of the split.

Finally, always stand back and look at the important issue of customer perception. Do customers realise that they are dealing with separate entities when they part with their hard‑earned cash? If the answer is ‘no’, there will almost certainly be a potential VAT problem lurking in the background.

In the case of Mario and his hairdressing operations, I think it will be fine to form a separate entity for his new salon – just about!