Merged R&D scheme: impact on quarterly instalment payments

Share this article

We explore the implications of the new merged R&D tax relief regime for taxable profits and quarterly instalment payment obligations.

Key Points

What is the issue?

Under the merged regime, R&D relief is now treated as a taxable credit, which increases taxable profits rather than reducing them. This change can push companies above the QIP threshold, even if their underlying profits remain unchanged, thereby triggering earlier tax payment obligations.

What does it mean to me?

When calculating QIPs, companies must base their instalments on pre-credit tax liabilities. This can lead to underpayment and interest charges if not properly accounted for. The ‘year of grace’ rule gives companies a one-year buffer before entering the QIP regime, though this does not apply to companies in the ‘very large’ instalment regime.

What can I take away?

Advisers are encouraged to help clients forecast their taxable positions under the new rules and ensure timely compliance with QIP obligations to avoid penalties and interest.

The merged research and development (R&D) tax relief scheme was introduced for accounting periods beginning on or after 1 April 2024. Whilst most commentary to date has focused on the changes impacting the R&D landscape, one important aspect not to be overlooked is the wider impact on tax attributes and quarterly instalment planning.

The former regimes

Under the SME regime, the impact of an R&D claim acted as a ‘super-deduction’ within the tax computation – reducing taxable profits. To the extent that a loss arose, a company could surrender such losses for an R&D tax credit.

As a reminder, ‘large companies’ (those with taxable profits in excess of £1.5 million) are required to pay their corporation tax liability under quarterly instalments, rather than nine months and one day after the end of the accounting period. These thresholds are reduced by the number of associated companies (the impact of which we will see in the example below).

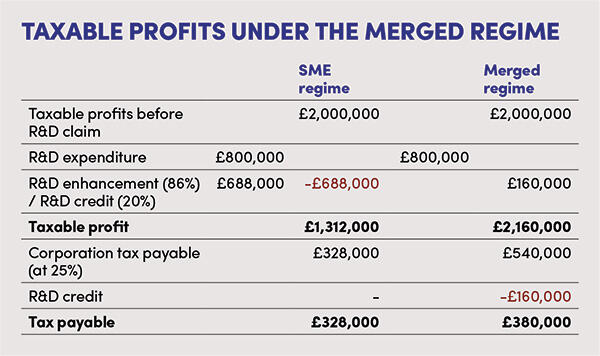

If a company anticipated taxable profits of £2 million but also had qualifying R&D expenditure under the SME regime of £800,000 (resulting in a further deduction of £688,000) then it would fall below the quarterly instalment payments (QIP) threshold (assuming no other associated companies) and continue to pay its corporation tax liability nine months and one day after the period end. This is no longer the case under the merged R&D regime!

The merged R&D regime

For accounting periods beginning on or after 1 April 2024, the R&D relief under the merged regime is treated as a taxable credit – rather than a super-deduction. This has two important impacts.

Firstly, the taxable credit is to be taken into account in determining whether or not the company’s taxable profits will fall into the QIP regime or not. Taking the example above and applying it to the merged regime, a company anticipating taxable profits of £2 million with £800,000 of qualifying R&D expenditure would have a taxable profit of £2.16 million and therefore need to consider the QIP regime. This is shown in Taxation profits under the merged regime above.

The second impact is that the reduction in the tax liability from the credit cannot be taken into account for QIP purposes. The R&D expenditure credit (the RDEC) is a standalone credit, so is not treated as a deduction in calculating the corporation tax liability. The reduction in liability from the RDEC therefore should not be taken into account for the calculation of quarterly instalment payments; i.e. instalments in the above example should be made on the £540,000 rather than the £380,000, otherwise late interest will be calculated.

What about the year of grace?

A company will only need to pay its corporation tax liability in quarterly instalments when it is within the regime for a second consecutive period. Whilst this grace period is useful in giving companies time to plan and prepare, it is important to be aware of when the instalment dates fall due – particularly with interest on late or underpaid instalments now being charged at 6.5% from 18 August 2025.

Let’s look at the above example again – but this time base the workings on two associated companies, such that the thresholds for QIP become £750,000.

In the year ended 31 March 2025, taxable profits of £1,312,000 result in the company being in excess of the QIP threshold for the first time, and so it will need to consider QIPs for the 31 March 2026 period end. The quarterly instalment dates become:

- 14 October 2025: 25% of estimated liability

- 14 January 2026: 50% of estimated liability

- 14 April 2026: 75% of estimated liability

- 14 July 2026: 100% of estimated liability

Note also that the company tax liability for the 2025 tax year will also be due on 1 October 2026, which can have a significant impact on cashflow.

The very large instalment regime

What about companies in the very large instalment regime? Companies in the ‘very large’ regime have their instalment due dates accelerated by a further three months, becoming: 14 June 2025; 14 September 2025; 14 December 2025; and 14 March 2026.

A company is considered to be in the very large regime if its taxable profits exceed £20 million. This threshold is reduced by the number of associated companies, so whilst you would normally not expect to be caught out by having profits rise to this level in one year, it is not uncommon for companies to fall into the accelerated regime with relatively modest profit levels, by virtue of being part of a group with multiple subsidiaries worldwide. This can particularly be the case with private equity-backed businesses.

Crucially, there is no ‘year of grace’ under the very large instalment regime. Once a company falls into it, the new instalment dates are to apply in that year.

Why is this important?

A company previously making R&D claims under the SME regime will need to consider how the impact of the merged R&D regime impacts their taxable profits, and whether they inadvertently fall into the QIP regime.

As can be seen from the dates above, falling into the quarterly instalment regime can result in a company being required to settle its tax liability significantly earlier than if it is used to doing this nine months after the year end, and potentially incurring interest charges if it is not on top of its instalment payment dates.

Advisers are strongly recommended to proactively engage with taxpayers to help forecast their future position, bearing in mind the interaction of the R&D merged regime and quarterly instalment payments, in order to help mitigate interest charges accruing.

© Getty images