The motor car challenge!

Share this article

Neil Warren provides guidance on claiming input tax on a new car, in light of four recent Tribunal cases dealing with this issue

Key Points

What is the issue?

VAT charged on a new car is blocked for input tax purposes if it is not used exclusively for business purposes and is also available for private use. Two separate businesses have recently convinced the courts that cars they had purchased were not available for private use. What does the phrase ‘available for private use’ actually mean?

What does it mean to me?

There might be scope to claim input tax on past car purchases and also plan restrictions for private usage on future purchases. Each car purchase needs to be considered on its merits.

What can I take away?

Despite the two tribunal victories, it will be very hard to prevent private use of vehicles in most cases. In one of the cases, however, the tribunal said that a small amount of private use was not a problem, such as occasional detours while on a business trip.

The issue of whether input tax can be claimed on new cars bought by a business has kept the courts busy for many years. Neil Warren considers four recent First-tier Tribunal cases and asks if there is scope for more claims to be made in the future.

The legislation says that input tax cannot be claimed by a business on a new motor car unless it is exclusively used for business and is not available for private use. It is the second condition that presents the most challenges – how can a business prove that a car is not ‘available’ for private use? Two separate businesses managed to convince the courts in recent tribunal cases which I will review in this article. But to balance the books, HMRC also won two cases, to leave the current state of play at 2-2. As you would correctly conclude, this equal score means that this issue is not clearcut and each purchase needs to be considered on its merits.

Background

As a starting point, if a business trades as a driving school, car hire business, taxi firm or car dealer, then it can claim input tax on its car purchases. Any business can claim input tax if it buys a vehicle that will be used as a genuine pool car. The two main features of a pool car are:

- It is not allocated to any single employee and is available for the general use of company employees

- It is kept overnight at the business premises and not at the home addresses of employees.

But in other cases, valid claims on car purchases are very rare and HMRC have been known to not only disallow input tax but also issue penalties.

A question I am sometimes asked by accountants is as follows: if a taxi or car hire firm buys a vehicle for its trading purposes but there will be some private use of the car by directors or employees, can it still claim input tax on the purchase? The answer is ‘yes’ as long as the car is purchased primarily for business purposes. To quote from HMRC VAT Manual – Input Tax – VIT52100: ‘HMRC accepts that there will be some private use of these cars.’

To share a tale from my Customs and Excise days, I visited a construction company in Leicester about 30 years ago where the director claimed that he personally drove a Fiat Uno car (for younger readers, an Uno is a small economical car a bit like a Mini) and that a Jaguar XK8 with a personalised number plate and expensive alloy wheels was a pool car for general use by employees. He had shrewdly worked out that an input tax sacrifice on a £5,000 car was a better result than on a £30,000 car. Needless to say, I reversed that outcome and disallowed the input tax on the Jaguar. I made him sweat before accepting that the Uno was a pool car.

The legislation

The relevant legislation about input tax and cars is set out in Article 7 of the Value Added Tax (Input Tax) Order SI 1992/3222. There are two hurdles to overcome:

- The intention should be to use the vehicle wholly for business purposes; and

- It should not be available for private use.

As explained above, the second test is often the main problem – what does the law mean by ‘not available for private use’? The answer is that there must either be a legal or physical restriction in place to prevent private use and this was the key issue in the four cases that I will now consider.

Contract of employment preventing private use

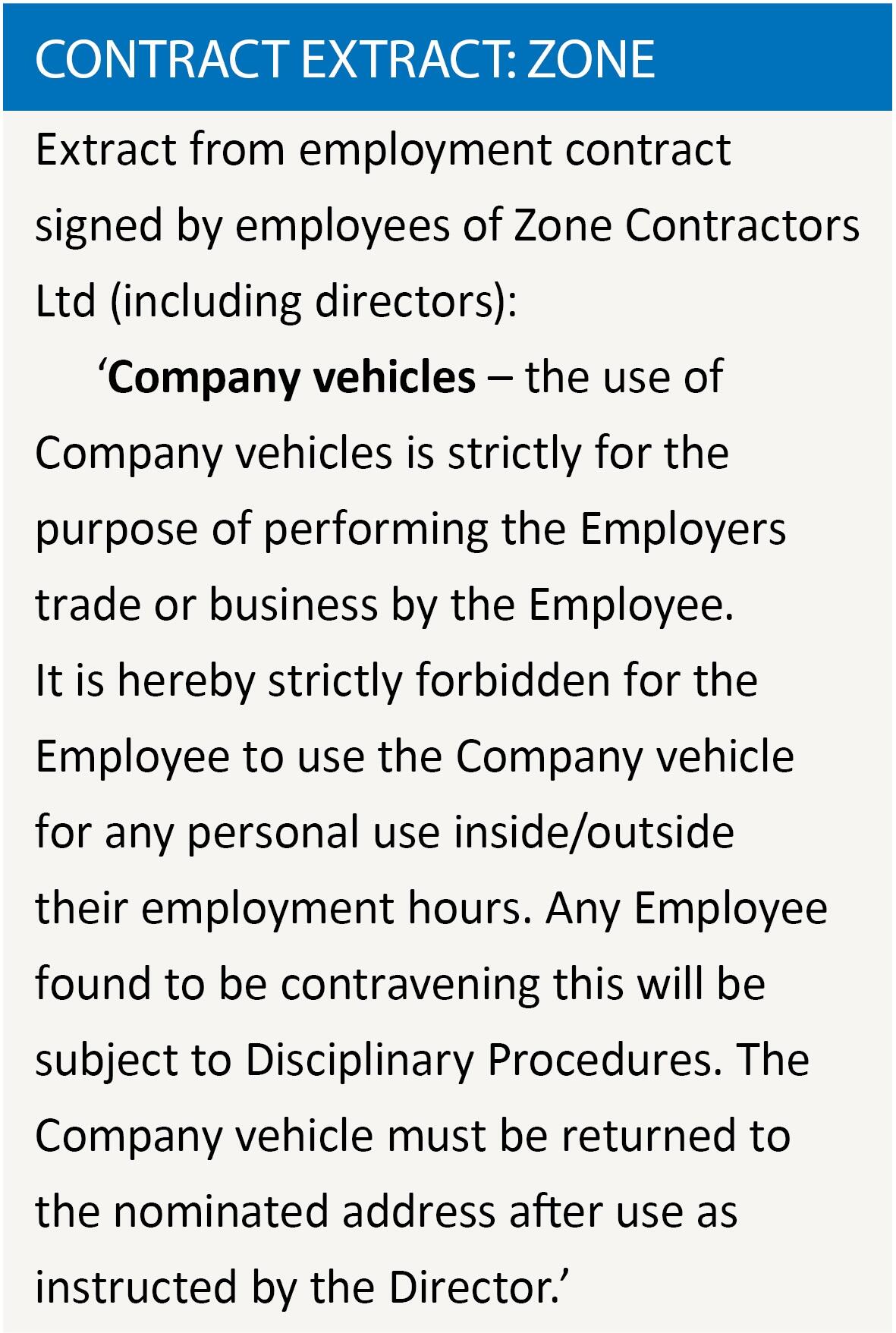

A strongly worded contract of employment that prevented employees from using company cars for private travel was the crucial factor that saw a tribunal victory for Zone Contractors Ltd (TC5330). The company was entitled to claim input tax totalling £27,151 on the purchase of six new cars because the tribunal was satisfied that they were wholly used for business and not available for private use. The contract was signed by all employees when they joined the company but HMRC’s view was that the contract was a red herring because it was not properly enforced. The tribunal rejected this argument.

I have shown the relevant paragraph in Contract extract: Zone and it is certainly worded very clearly. To quote from para 48 of the tribunal report: ‘The tribunal considers that the terms of the contract are explicit and binding.’ The company’s argument was also helped by the fact that all of the key employees and directors had their own cars for private use and they also convinced the tribunal that the vehicles were either left on site overnight or at the company’s premises i.e. never taken home by employees.

Business only insurance cover

The key fact in the case of Jane Borton (TC5224) was that the insurance policy for her Land Rover Freelander car only covered her for business trips, i.e. there was a specific exclusion for social, domestic and private use (SDP). However, many insurance policies (possibly the majority) don’t provide stand-alone business cover so the fact that a policy might include SDP use does not automatically block an input tax claim. In fact, the insurance policy in the Zone case included SDP use because it was a fait accompli of that particular level of cover.

I was disappointed to read that as well as HMRC raising an assessment for £4,913 to disallow Ms Borton’s input tax claim on her Land Rover, the officer also issued a careless error penalty of £736. But a happy ending was achieved because both the assessment and penalty were overturned by the tribunal and to quote from the report (para 22): ‘We are satisfied on the basis of the evidence as a whole that the appellant had no intention, at the time she acquired the Freelander, to make it available to herself or any other person for private use.’

Cases won by HMRC

Ireland Generator and Spare Parts Ltd purchased a car in VAT period 10/15 and claimed input tax of £2,424, which was subsequently disallowed by a compliance officer (Case TC5415). To be honest, this was an easy victory for HMRC because the company director kept the car at his home over the Christmas period and there was no legal or physical restriction in place to prevent private use by the director or employees of the company. As the tribunal noted in para 22 of the report: ‘The appellant cannot show that the car was out of the reach of anyone who could potentially undertake a private journey.’ The appeal was dismissed.

In the case of Venda Valet Ltd (TC5321), the court concluded that although there was an informal agreement between the two directors that a Mercedes car would not be made available for private use, there was no legal or physical restriction in place. So the court upheld the assessment of £7,833 raised by HMRC to disallow input tax claimed in April 2013.

Learning points

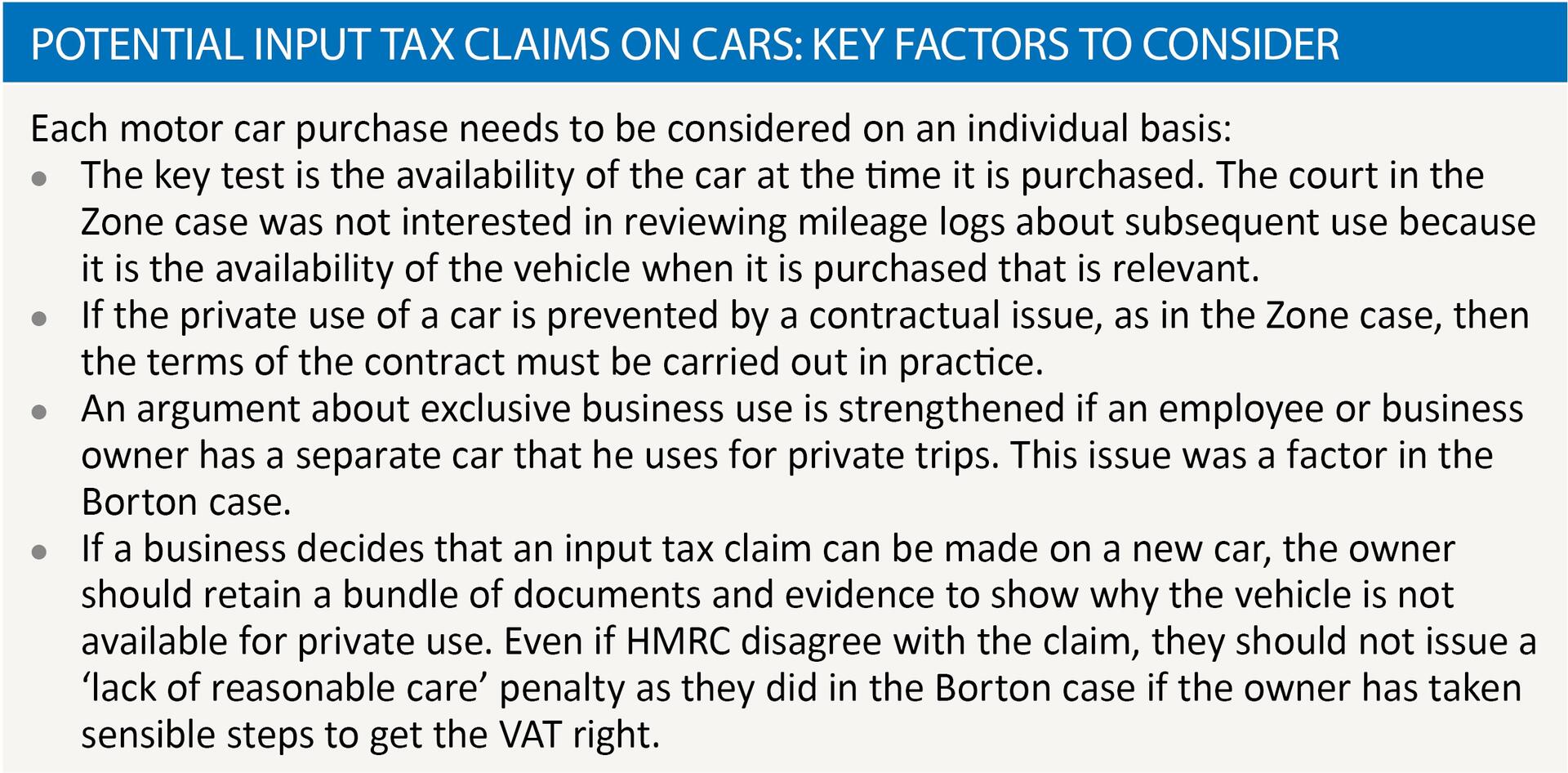

It is clear from the four cases I have considered that each vehicle purchase needs to be considered on its merits to assess the ‘available for private use’ issue. As an overall guide, see Potential input tax claims on cars, where I have highlighted the key issues to consider.

As another twist to the tale, HMRC also put forward the valid argument in the Zone case that private use of a car would include detours to buy ‘cigarettes or lunch while out on a business journey or even going off site to collect lunch’ (para 56). The tribunal concluded that such use could be ignored as de minimis and added that if such use of cars was relevant, it would be virtually impossible for any car to qualify for input tax deduction under Article 7.

As a final comment, be aware that the four cases I have analysed were all heard in the FTT, so the conclusions are only binding on the parties involved. As far as I am aware, none of the outcomes have been appealed to a higher court but we’ll wait to hear on that one.