New limit

Share this article

Adeline Chan and Roger Muray provide an HMRC perspective on the corporate interest restriction

Key Points

What is the issue?

The new Corporate Interest Restriction rules impose a limit on the amount of finance costs that companies can deduct for corporation tax purposes.

What does it mean to me?

Any group with net financing costs of more than £2 million per annum may be affected. A group may need to appoint a reporting company by 31 March 2018 and file an interest restriction return by 30 June 2018.

What can I take away?

Even if there is no interest restriction, appointing a reporting company and filing an abbreviated interest restriction return may be beneficial. Most other rules limiting interest continue to apply, including transfer pricing.

Subject to the provisions in the Finance Bill passing through Parliament and receiving Royal Assent, the new Corporate Interest Restriction rules will be effective from 1 April 2017. They will impose a limit on the amount of finance costs that groups can deduct for tax. These rules reflect the recommendations of the OECD Base Erosion and Profit Shifting Project and the requirements of the EU Anti-Tax Avoidance Directive.

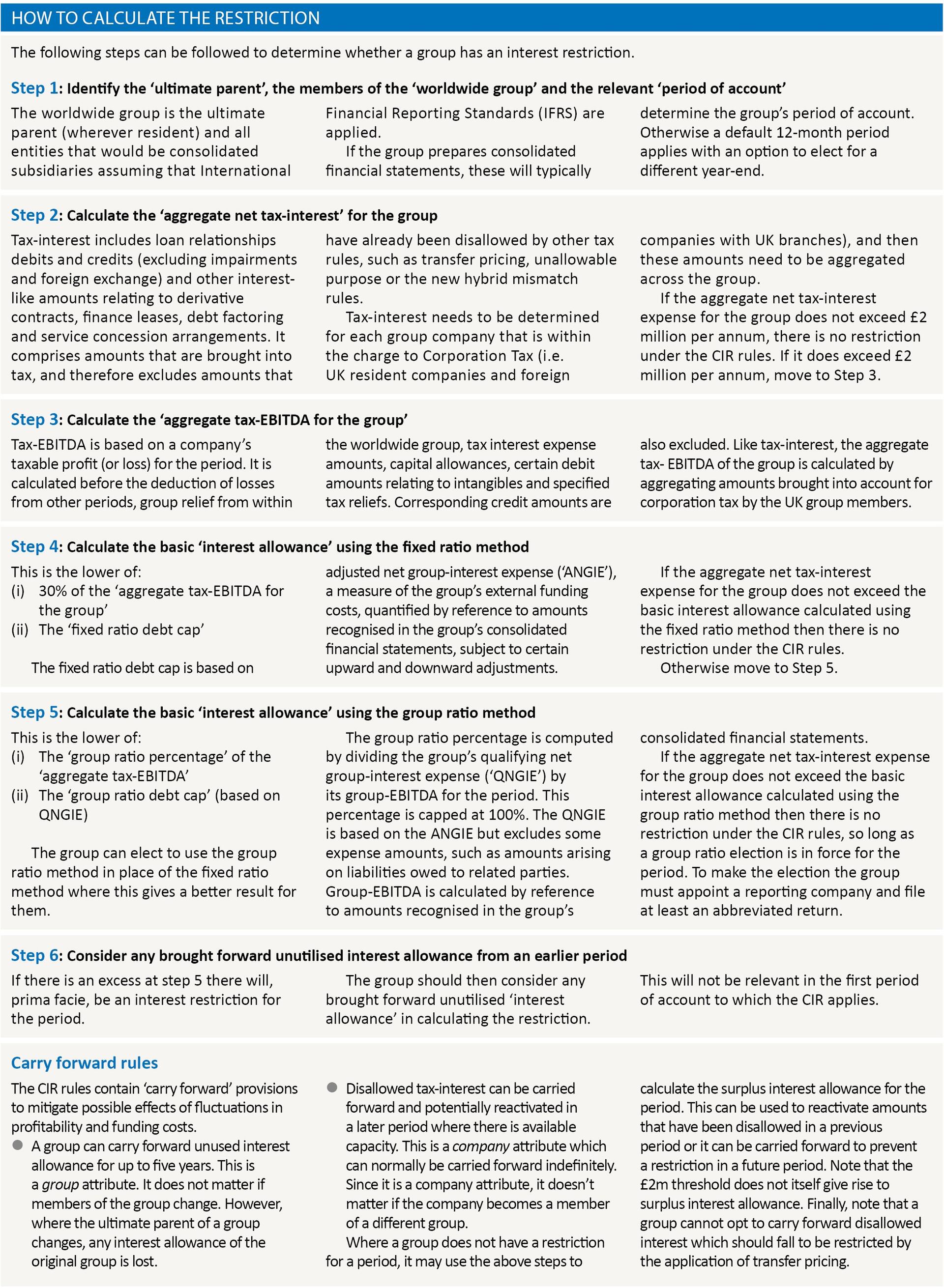

In a classic example of UK base erosion through excessive funding costs, a lowly-geared multinational funds its UK operations with a high level of internal debt. The Worldwide Debt Cap (‘WWDC’) rules targeted such situations, but allowed the group to deduct interest in the UK up to the group’s overall gross external interest cost. The new CIR rules replace the WWDC rules. These go further by limiting Corporation Tax deductions for net financing costs to a percentage of ‘tax-EBITDA’. This is the UK taxable profits, before deduction of interest, capital allowances (the tax equivalent of depreciation in the UK) and amortisation of intangible fixed assets. A single limit applies to the worldwide group.

A modified debt cap is retained in the new rules. This is more stringent than the WWDC because deductions for net ‘tax-interest’ (see step 2 in the table) are limited to the external net accounting finance costs rather than the gross under the WWDC.

All groups may calculate their interest allowance using the fixed ratio method, which sets the limit at 30% of tax-EBITDA, subject to the debt cap. An optional group ratio method prevents the CIR rules having an overly restrictive impact on groups that are highly leveraged. This allows the group to replace the 30% fixed ratio with a ‘group ratio’ based on the group’s consolidated financial statements. There are also specific rules for public infrastructure companies which meet strict conditions.

What do you need to do?

Groups need to decide between three main options:

- Do nothing, because no interest restriction arises and this is likely to be the case for future periods of account, for example, because net tax-interest for the group is expected to remain below £2 million per annum.

- Appoint a reporting company which files an abbreviated Interest Restriction Return (‘IRR’), which identifies the group members. This would be prudent where no restriction arises in a period of account but the group may face a restriction in a later period. In that eventuality, the group can replace the abbreviated IRR with a full IRR to carry forward unused interest allowance up to five years.

- Appoint a reporting company which files a full IRR. For groups that are subject to a restriction for the period, appointing a reporting company simplifies the administration and allows the group flexibility in how any restriction is allocated. A full IRR is also necessary to reactivate amounts of previously disallowed tax-interest.

Can a group do nothing?

If a group has ‘aggregate net tax-interest expense’ of less than £2 million per annum (‘the threshold’), it cannot suffer an interest restriction. If this is likely to be the position going forward, it can ignore the CIR rules, i.e. take option 1 above. The threshold amount is not an ‘interest allowance’ that groups can deduct.

Other corporation tax rules that can restrict the deductibility of interest remain in place. For instance, transfer pricing and unallowable purpose rules will continue to restrict finance costs that exceed arm’s length amounts or are tax-motivated. They apply first to determine the amount of tax-interest that is tested by the CIR rules. It may be that these other rules limit tax-interest to below £2 million.

What if the £2 million threshold amount is exceeded but no restriction arises?

Groups with net tax-interest expense in excess of the threshold amount but for which no restriction arises do not need to appoint a reporting company or file a full IRR. However, the group may choose to appoint a reporting company and file an abbreviated IRR.

This has two main benefits. Firstly, if it subsequently turns out that there is a restriction for the period then the reporting company can exercise flexibility in allocating the restriction between group companies. Secondly, it allows the group to subsequently file a full IRR in place of the abbreviated IRR. This permits a group faced with a restriction in a later period to go back up to five years and file full IRRs calculating and carrying forward unused interest allowance.

Where a reporting company has been appointed then it must file an IRR for the period. However, if the group does not suffer a restriction in the period, it has a choice between filing an abbreviated or a full return.

Even if the threshold amount is exceeded, the group may not have to perform a full CIR calculation if it can conclude that a restriction is highly unlikely based on reasonable estimates of ‘aggregate net tax-interest expense’, ‘aggregate tax-EBITDA’ and ‘adjusted net group-interest expense’. A record of the approximate calculations should be kept together with other records to show the group has taken reasonable care in arriving at the conclusion that there is no restriction.

Groups with interest restriction

Groups which have an interest restriction can take option 3 above. While not obligatory, appointing a reporting company will simplify administration as well as giving the group greater flexibility in allocating the restriction.

Reporting company

The ‘reporting company’ should normally be appointed within six months of the end of the group’s period of account. However, for periods of account ending before 30 September 2017, the time limit has been extended to 31 March 2018. The appointment has to be authorised by at least 50% of non-dormant group companies within the scope of UK Corporation Tax. It rolls over to future periods of account, unless revoked.

The reporting company is responsible for filing original IRRs and any revised IRRs, allocating restrictions and reactivations of tax-interest across the group companies, and dealing with any related HMRC enquiries. If the group does not appoint a reporting company, HMRC has the power to do so.

The rules give a reporting company discretion to allocate interest restrictions between group companies as long as all the disallowed amount is allocated. However, to protect minority interests, the CIR rules limit the amount that can be allocated to companies which choose to be ‘non-consenting’.

Filing an IRR

Where a reporting company has been appointed and the group suffers a restriction in the period then the reporting company must submit a full IRR.

The normal time limit for filing a return is 12 months after the end of the period of account or if later, three months after appointment of the reporting company. After this a penalty can arise. However, the filing deadline for an IRR in the first year has been extended so that it cannot be before 30 June 2018.

Contact with HMRC

Groups can discuss their situation with their HMRC customer relationship manager (‘CRM’) if they have one. For groups without CRMs, the main point of contact with HMRC for technical queries is via the CIR mailbox ([email protected]).

Conclusion

This article provides a very brief introduction to the new CIR legislation. Draft guidance is already publicly available on gov.uk. Although the new rules are lengthy, few groups will have to engage with many of the sections. Much of the complexity stems from a desire to protect groups from unfair outcomes while maintaining the policy objective of ensuring that tax relief on financing costs is commensurate with the activities of the group that are subject to corporation tax.