A new tax regime for qualifying asset holding companies

Share this article

A special tax regime has been created for qualifying companies to remove the obstacles preventing many funds from using UK resident asset holding companies.

Key Points

What is the issue?

From April 2022, there is a new regime for qualifying asset holding companies (QAHCs). Companies that meet the eligibility conditions can choose to enter into the regime.

What does it mean for me?

Advisers operating in the alternative investments space should familiarise themselves with the new UK regime. More generally, advisers should be aware that UK QAHCs will become features of holding stacks and consideration should be given to the implications on M&A scenarios.

What can I take away?

This article outlines the criteria for joining the QAHC regime and its key benefits. It then provides an illustration of how the tax computation of a QAHC might look, before discussing some of the administrative points applicable to QAHCs and how to seek assistance from HMRC’s dedicated QAHCs team.

The UK has done much in recent years to build its reputation as a location for fund management. However, until now, for a variety of mainly tax reasons, industry has considered the UK to be a less attractive place to locate an asset holding company within an alternative investment fund structure. These companies sit between funds and their investments, facilitating the flow of funds between investments and investors.

Historically, industry has been content to locate management professionals in the UK serving funds whose asset holding companies were elsewhere – most commonly, although not exclusively, in Luxembourg. In recent years, the growing importance of substance in obtaining reliefs, including under tax treaties, has led to calls to facilitate co-location of fund management teams and their investment structures.

Following extensive consultation with industry stakeholders, the UK government has created a special tax regime for ‘qualifying asset holding companies’ (QAHCs) to remove the obstacles preventing many funds from using UK resident asset holding companies. In turn, this should enable those funds to be comfortable retaining or establishing a management team in the UK. This regime confers a selection of tax benefits on QAHCs and their UK resident investors.

These benefits are designed to ensure that, in common with many other fund vehicles in use around the world, as far as possible QAHCs enable fund investors to achieve the same result as if they had invested in the fund’s underlying assets directly.

The QAHCs reforms are being taken forward as part of a wider review of the UK’s funds regime. This review is seeking to further improve the UK’s attractiveness for funds, whilst supporting a wider range of efficient investments suited to investors’ needs.

Qualifying for the regime

In order to qualify for the regime, a QAHC must meet criteria as to its ownership and its activities. Summarising considerably, it must be at least 70% owned by:

- investment funds;

- entities such as pension funds or life insurers which make investments for a pool of beneficiaries; or

- other entities which are tax exempt for good policy reasons (such as most charities and many public bodies).

A QAHC must predominantly have an investment business. Anything else it does must be ancillary to that business, and not be substantial. This effectively limits trading activity of a QAHC to such things as the provision of some management services to its investee companies.

The intention is that QAHCs will play a role in facilitating the management of investments and the flow of funds from investments to ultimate investors. This role is necessarily intended to be limited, but not entirely passive.

Benefits of the regime

When a company enters the regime, a number of tax benefits become available to it and its investors, as follows:

- an exemption from tax on gains on the sale of shares, except where those shares are in UK real property rich companies;

- an exemption from tax on gains on the sale of non-UK real property;

- an exemption from tax on non-UK source real property income, as long as that income has been subject to tax in the source country;

- an ability to claim deductions in respect of the coupons on instruments such as convertibles or results dependent loans, which might otherwise be treated as distributions;

- an exemption from withholding tax on interest payments made by the QAHC;

- an exemption from stamp duties on share repurchases by the QAHC;

- disapplication of the rules which may treat the premium on a share buyback by the QAHC as a distribution; and

- an ability for UK resident non-domiciled shareholders to treat returns as non-UK source (and so eligible for the remittance basis) to the extent they derive from non-UK situs investments of the QAHC.

Companies entering the regime with certain assets will be treated as disposing of those assets and reacquiring them at market value at the point of entry.

Fluctuations in the value of loan relationships held as investments give rise to the same tax consequences for a QAHC as for any other UK resident company. However, it is expected that credit funds, where the QAHCs will be investing in portfolios of debt, will typically be funded by profit participating loans with the result that a QAHC pays tax on a profit commensurate with its contribution to overall profit generation, in line with the transfer pricing rules.

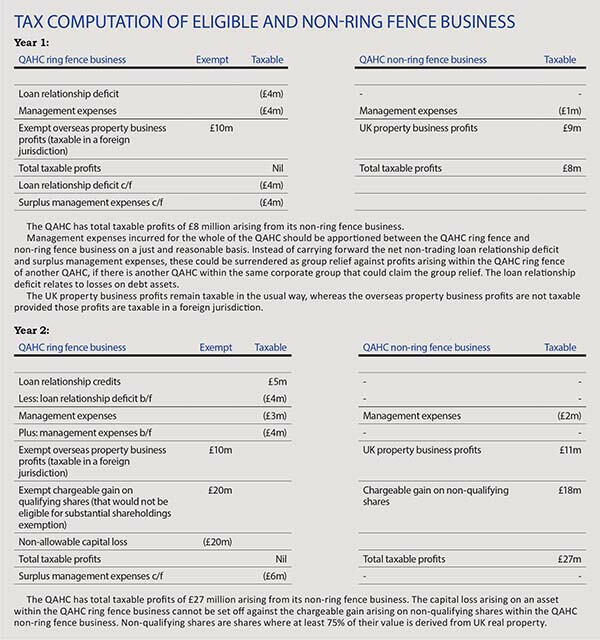

A QAHC may carry on some business that is not eligible for any of the relieving rules – this is referred to as the non-ring fence business. It may carry on a very limited trade, as long as it is not substantial and is ancillary to the investment business. It may also carry on an investment business which falls outside the reliefs, such as the holding of UK real property or shares in companies that are UK real property rich. Any such business is effectively taxed as normal, and the QAHC must prepare a tax computation showing both elements of its business. This streaming is illustrated in the example in the box below.

Tax rules relating to groups reflect the above; e.g. no gain/no loss treatment does not apply if a capital asset is transferred to a QAHC from a normal company with which it is grouped, if that asset would be exempt in the QAHC’s hands. Effectively, the tax-privileged business of the QAHC is treated as if it was carried on by a different company from any other business, and that notional company can only access group treatment with the tax-privileged businesses of other QAHCs.

Administrative issues

Those familiar with HMRC’s Collective Investment Scheme Centre (CISC) will recognise the benefits of working with a dedicated team responsible for procedural matters and monitoring compliance. HMRC will be replicating the CISC model with a new QAHC team. You can contact the team at [email protected], 03000 515900 or at Wealthy and Mid-Size Business Compliance, HMRC, BX9 1QW.

A company that meets the eligibility conditions and wishes to join the QAHC regime must notify the QAHC team, electronically via bit.ly/3IB2hMf. Please do not send notifications to the QAHC team by email or post as they will not be accepted by HMRC as valid.

Once a company joins the QAHC regime, as well as the usual company tax return, it must make a return of certain information for each accounting period:

- name and unique taxpayer reference (UTR) of the QAHC;

- name, address and UTR of any person who has provided investment management services to the QAHC during the accounting period;

- an estimate of the market value of the gross assets of the QAHC’s ring fence business at the end of that accounting period;

- the gross proceeds arising from disposals of assets from the QAHC ring fence business during the accounting period; and

- the amounts of any payments made by the QAHC on the redemption, repayment or purchase of its own shares.

The annual QAHC information return must be made electronically via the link above. A penalty of £300 may be levied for failure to provide this information.

In addition, the company is expected to indicate that it is a QAHC by entering the appropriate code in box 4 (type of company) of the form CT600 for each accounting period.

Technical guidance is in HMRC’s Investment Funds Manual at IFM40000+ at bit.ly/3psPQuw. The QAHC legislation is at Finance Act 2022 Schedule 2.