Not exactly child's play

Share this article

Ian Goodwin examines the tax challenges of paying for childcare

Key Points

What is the issue?

From 2017, The government introduced a further arrangement (in addition to childcare vouchers) to help parents with the cost of childcare. This is known as ‘Tax Free Childcare’ and it has caused parents, guardians and employers to review their approach due to how these schemes differ and what the future of the employer supported childcare scheme looks like.

What does it mean to me?

For both employers and employees, there is a potential lack of clarity about how the schemes affect them. This article analyses the two arrangements in detail.

What can I take away?

Although the Tax Free Childcare arrangement takes away compliance responsibilities from the employer, it does leave the employee with more choices and considerations. But employers should not just ignore Tax-Free Childcare, especially where they provide childcare vouchers.

With more parents and guardians now working full time and living apart from other family members, there is a growing need for support from employers and childcare providers. Many employees have sought to fund childcare costs by using the Government’s ‘employer-supported childcare scheme’ arrangement. This scheme has helped parents to manage costs as it benefits from income tax and Class 1 National Insurance Contribution (NIC) exemptions.

However, from 2017, the Government introduced an additional arrangement to help parents with the cost of childcare. This is known as ‘Tax Free Childcare’ and it has caused parents, guardians and employers to review their approach due to how these schemes differ and what the future of the employer supported childcare scheme looks like.

For both employers and employees, there is a potential lack of clarity about how the schemes affect them. This article analyses the two arrangements in detail. Please note that this article does not assess the interaction with child tax credits or other Government support.

What is the employer-supported childcare scheme (childcare vouchers)?

The current employer-supported childcare scheme was introduced in 2005, and was followed by changes in 2011. Many employers found these 2011 changes to have brought a significant administrative burden. The scheme saves parents/guardians money on childcare costs, because it provides income tax and Class 1 NIC relief on qualifying childcare costs, up to a certain amount. This amount was set at £243 per month (or £55 per week) where certain conditions were met. The scheme has proved popular with employees thanks to the savings it has provided, in comparison with paying for childcare support out of net pay. It is estimated to have helped over 750,000 employees.

Employers have and continue to typically operate the scheme on a ‘salary sacrifice’ basis to manage the costs of operating the arrangement and provide childcare vouchers. The participating employees then could sacrifice up to £243 of their salary per month before any income tax and NIC deductions (subject to how their pay interacts with the National Minimum Wage (NMW). In exchange, employees would then receive electronic vouchers to be used to pay for qualifying childcare.

The scheme has provided relief on a per-employee basis, rather than a per-child basis, and is only available to employees who work for an employer which offers access to the arrangement. Therefore, regardless of the number of children in their care, the income tax and NIC exemption remained the same. This meant that a parent with one child would be able to claim the same amount as a parent with five. However, where both parents / guardians work for employers which provide access to the scheme, they could both claim vouchers up to a maximum of £243 per month, income tax and NIC free.

The April 2011 changes

From 6 April 2011, the government implemented changes to the employer supported childcare scheme. The changes related to restricting the income tax and NIC relief available to those employees categorised as higher or additional rate tax payers. This change is only relevant to employees who signed up for the arrangement on or after 6 April 2011. If an employee was already participating in childcare vouchers prior to 6 April 2011, their income tax and NIC-exempt amount remains at £243 per month. This is regardless of their level of earnings, provided they remain employed by the same employer and have not taken a break from the scheme for a period of more than 52 weeks. This has meant that employers have been required to set up a ‘Basic Earnings Assessment’ to ensure employees do not receive too many vouchers free from income tax and Class 1 NIC deductions. The complexities around setting up appropriate systems to accurately undertake a Basic Earnings Assessment have led to errors in calculations. As a result, a number of employers have received penalties from HMRC for giving certain employees too many vouchers free of income tax and NIC. The vouchers available for income tax and Class 1 NIC relief is currently restricted to the following:

- Basic rate taxpayers can have up to £55 a week (£243 a month) tax and NIC exempt

- Higher rate taxpayers can have up to £28 a week (£124 a month) tax and NIC exempt

- Additional rate taxpayers can have up to £25 a week (£110 a month) tax and NIC exempt

We explain below the technical aspects of the Basic Earnings Assessment.

The Basic Earnings Assessment

‘Relevant earnings’ includes salary, wages, fees and other contractual payments including allowances, guaranteed overtime and contractual commissions/bonuses. HMRC has confirmed that performance-related discretionary bonuses and non-guaranteed overtime payments do not need to be included. Similarly, overtime payments should be included only if they are guaranteed. Therefore, it is important that employers know what payments they are making to their employees and have established what payments are not included in the assessment. This means that it is important to establish the characteristics of payments made to employees to ensure they are being assessed and understood correctly by those responsible for the governance of the arrangement.

When to carry out the basic earnings assessment

The assessment has to be carried out at the ‘required time’. This is the start of the tax year except in respect of employees joining the scheme part way through the year, in which case the required time is the joining date. Therefore, most employers will carry out the assessment based on the information that they have available on an employee’s pay as at 5 April, or when they agree to join the scheme at a different time. Employers therefore need to have set up a system to manage this compliance obligation.

The current position

As it stands, the employer supported childcare scheme continues to be available for employers to offer to employees and for qualifying employees to take advantage of. Following an update in March 2018, the scheme will be available to join until 4 October 2018. The scheme will then close to new entrants and only those registered and participating prior to 4 October 2018 will continue to be able to receive childcare vouchers after 4 October 2018.

Following this date, all new parents/guardians will only be able to join the Tax Free Childcare scheme. This is intended to simplify and provide a consistent and fair approach to supporting childcare costs, across parents and guardians in the UK.

Tax Free Childcare

Tax Free Childcare was launched on 21 April 2017 and has been rolled out gradually, following legal challenges and petitions that wished to stop the arrangement being introduced as it is intended that this new arrangement will replace the employer support childcare voucher arrangement.

Tax Free Childcare is not an employer scheme – it operates directly between the Government, the parents, and the childcare providers via an online account. The individual applies for this online.

Tax Free Childcare operates on a per-child basis rather than a per-employee basis. For every 80p the parent(s) pays into a newly-created Childcare Account, the Government will contribute 20p, up to a maximum amount of £2,000 per child (up to £10,000 can be added to each child’s account).

Before applying, parents/guardians will need to check that their childcare provider is signed up to the scheme in order to use the Tax Free Childcare account.

It applies equally to the self-employed, provided all participants meet the eligibility criteria.

Please note, any cash put directly in to a Tax Free Childcare account by an employer will be subject to income tax and Class 1 NIC via payroll.

Eligibility criteria for Tax Free Childcare

In summary, any individual parent/guardian or pair of parents needs to meet the following conditions to be eligible for the Tax Free Childcare arrangement:

- Initially, only children under the age of 5 years qualified, but the scheme has now been extended to include children under the age of 12 (they stop being eligible on 1 September, after their 11th birthday) and disabled children under the age of 17.

- To be in work – or getting parental leave, sick leave or annual leave, each earning at least the NMW for 16 hours a week;

- To not be in receipt of any tax credits, universal credits or employer supported childcare;

- To not have individual household taxable income over £100,000; and

- Confirmation of meeting the qualifying criteria every 3 months, known as the ‘entitlement period’.

Please note, if a child is disabled the individual may get up to £4,000 of relief a year until they are 17 under the Tax Free Childcare arrangement.

Which scheme shall I choose?

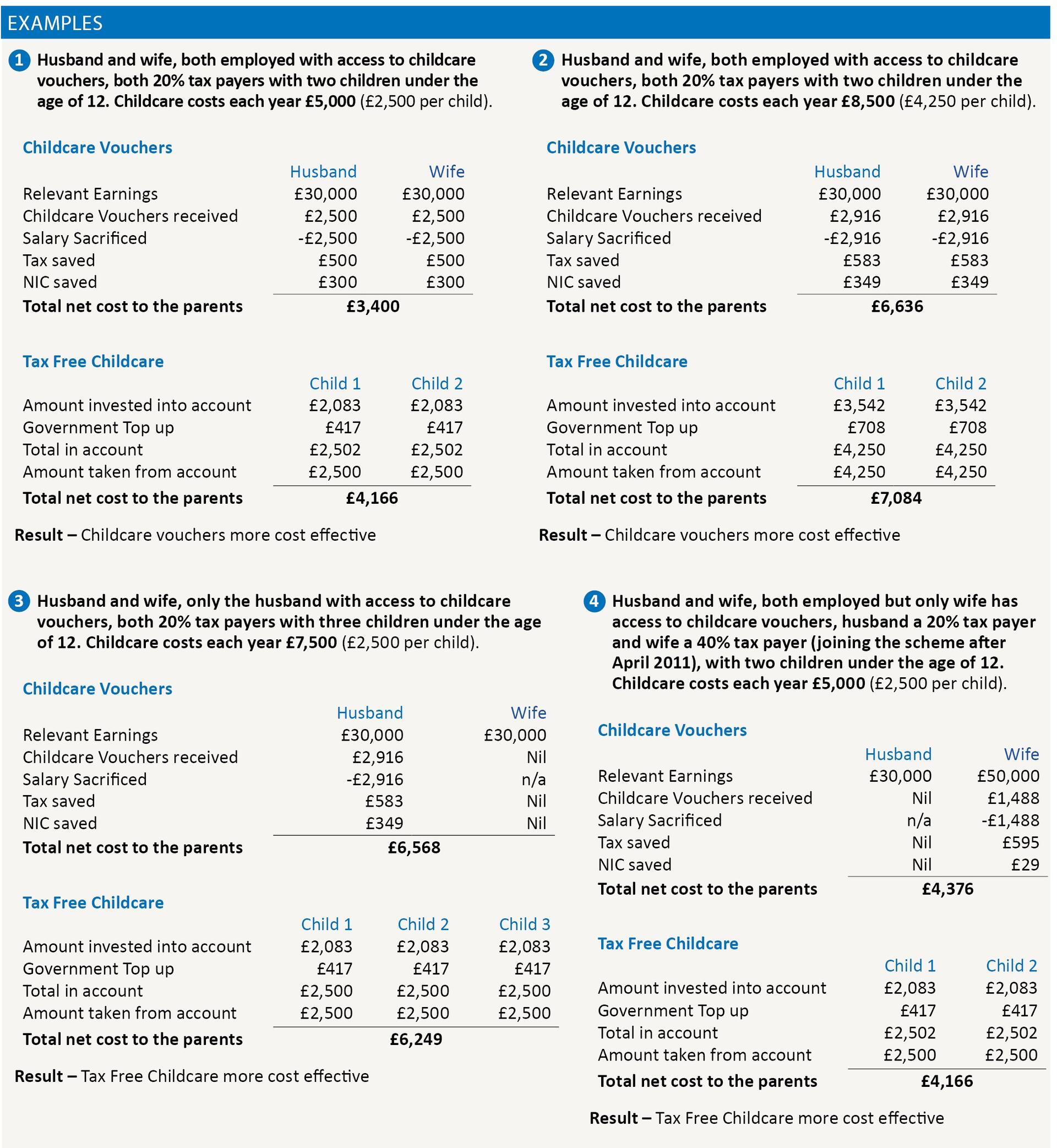

If you are eligible to receive childcare vouchers prior to 4 October 2018, you effectively have two choices – continue to receive childcare vouchers via the employer supported scheme or join the new Tax Free Childcare arrangement.

It will be important to establish which scheme is more cost effective if you qualify for both. See the illustrative example scenarios to help explore this in more detail.

What should employers and employees be doing?

Many employers have informed their employees that the Tax Free Childcare arrangement is available. However, they have no obligation to do so, even where they provide access to employer-supported childcare.

Employers providing information are taking care not to be giving financial advice and are therefore directing employees to seek their own advice and to read the information made available by the Government. Additionally, many employers with employer-supported childcare schemes have held workshops as part of their general reward strategy and communications approach to inform and update employees on the changes. This is particularly relevant given that the employer-supported childcare scheme is now due to close to new joiners on 4 October 2018.

Separately, employers have been assessing whether the introduction of a workplace nursery would be a more effective solution, given one can be provided tax/NIC free either via salary sacrifice or as an additional ‘perk’ (subject to meeting certain qualifying conditions). This is in addition to any childcare vouchers or Tax Free Childcare the employee may choose to receive.

An employee has an obligation to tell their employer that they have chosen to participate in Tax Free Childcare if they are currently in receipt of childcare vouchers. It is important to note that once an employee has told their employer that they have elected to benefit from the Tax Free Childcare arrangement, rather than from childcare vouchers, they cannot rejoin the employer’s childcare voucher scheme. The employee has 90 days to tell their employer that they are participating in Tax Free Childcare. The employee is still able to use any remaining childcare vouchers they have in their childcare voucher account after they join the Tax Free Childcare arrangement.

Taking the next step

Although the Tax Free Childcare arrangement takes away compliance responsibilities from the employer, it does leave the employee with more choices and considerations. Providing support to employees can help ensure they continue to remain motivated, understand their reward more clearly, and their skills are retained in the business. Therefore, employers should not just ignore Tax Free Childcare, especially where they provide childcare vouchers. If they do not currently provide childcare vouchers, they may wish to introduce the arrangement before the current closure date of 4 October 2018.