Partial exemption in VAT registered businesses

Share this article

Partial exemption is a well-known problem area for many VAT registered businesses. Here are the answers to your questions about the key rules, along with some VAT saving tips.

Key Points

Key Points

What is the issue?

Partial exemption is high risk as far as VAT errors are concerned. It is important that staff who allocate input tax between the three different expense categories understand the principles of recognising a link between an expense and either taxable or exempt income.

What does it mean for me?

If the standard method based on income ratios produces an unfair result, you could apply to HRMC to use a special method in the future. But you must certify that your proposed method gives a ‘fair and reasonable’ result in terms of input tax recovery.

What can I take away?

A practical use of the partial exemption de minimis limits could produce an input tax windfall of up to £7,500 on costs that relate to exempt supplies. The article illustrates how a landlord earning buy-to-let rental income can benefit from these rules.

What are the basic rules of partial exemption?

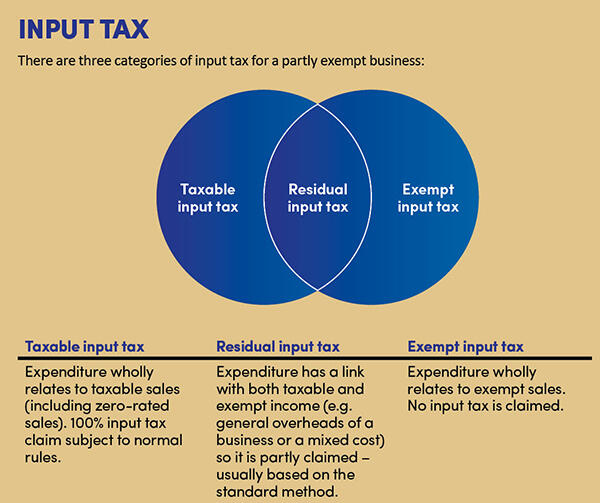

If a business only has taxable income – including zero-rated sales – it is entitled to full input tax recovery on its expenses, subject to the usual rules. If it has only exempt income, it cannot claim any input tax and, in most cases, will not be registered for VAT. The problem is when a business has both taxable and exempt income, and input tax apportionment is needed. The starting point is the concept of ‘direct attribution’ and the need for a business to allocate input tax on its expenses to one of three different categories – see the diagram below.

How is input tax apportioned between the three categories?

Think of an estate agent. The business earns exempt income from mortgage commission and taxable commission when it acts as an agent to sell a property.

If the business purchased a computer solely for the use of a mortgage broker, it will be input tax blocked because the expense wholly relates to its exempt supplies. However, it will fully claim input tax on a computer used by a sales negotiator selling houses. And a computer for the office receptionist will be treated as an overhead/mixed cost and therefore partly claimed.

It seems that ‘residual input tax’ is the most complicated figure. How is it apportioned?

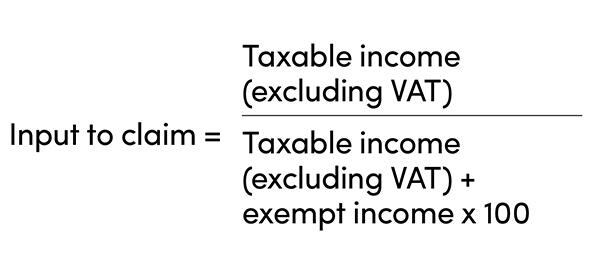

As the default position, a business must use the standard method of calculation, which is based on its ratio of exempt income to taxable income using the following formula (expressing the result as a percentage):

Note: If the total residual input tax figure is less than £400,000 a month on average, the percentage is rounded up to the next whole number (see VAT Notice 706 para 4.7).

The quarterly calculation is provisional and is superseded by an annual adjustment at the end of each partial exemption tax year, which is compulsory for all partially exempt businesses. The same formula is used but with annual rather than quarterly figures. A partial exemption tax year ends on 31 March, 30 April or 31 May, depending on the VAT periods of the business, or 31 March for a business on monthly returns.

So, presumably, the annual adjustment will always produce a different result compared to the quarterly calculations?

The annual adjustment can produce both under and overpayments of tax compared to the quarterly calculations. A taxpayer can either include the difference on the return at the end of the tax year or the next return.

I used to act for a members’ golf club, which bought most of its fixed assets in the first calendar quarter of the year when it also earned most of its exempt income from annual golf memberships. So, it had a low input tax recovery with the quarterly calculation – because of the high percentage of exempt income – which increased when the annual adjustment was done. The annual adjustment process corrects seasonal trading variations such as this.

If the standard method produces an unfair result, can a business use a different method to work out how much residual input tax it can claim?

Yes, it can apply to HMRC in writing to use a special method, which is any method that is not the standard method. Common examples are set out in ‘What are the special methods?’ below.

When requesting a special method, the business must certify to HMRC that it will give a ‘fair and reasonable’ result in terms of input tax recovery. If it is subsequently found that the method is flawed, HMRC has the power to issue an assessment to recalculate input tax on a ‘use’ basis (see VAT Notice 706 para 6.2).

Note: You can apply for a special method by email: [email protected]

What are the special methods?

- output values;

- numbers of transactions;

- staff time or numbers;

- inputs or input tax;

- square footage allocations;

- costs allocations; and

- management accounts.

You must calculate the percentage recovery rate produced in your special method to 2 decimal places.

What tips can you give a partially exempt business?

Here are two tips.

Firstly, make sure that input tax allocations between the three different categories – taxable input tax, residual input tax and exempt input tax – are carried out by an experienced member of staff. As a general observation, there is sometimes a tendency for a business to play safe and claim the lower amount of tax. For example: ‘I am not sure if this expense is “residual” or “exempt”. I’ll play safe and treat it as “exempt” … so I don’t upset HMRC.’

There have been numerous tribunal cases where taxpayers have won disputes. For example, the issue in the case of Folkestone Harbour (GP) Ltd [2015] UKFTT 0101 (TC) was whether the cost of erecting an expensive fountain on public land at the entrance to a new residential development directly related to houses being built and sold by the company. The tribunal agreed with the taxpayer that input tax could be claimed because the fountain created an image of style and class and therefore a direct link to the zero-rated property sales.

Secondly, be clear that a small link between an expense and taxable activities is enough to treat the input tax as residual.

Here is an example for our estate agent:

- The agent is planning to advertise its mortgage services in a newspaper, which will cost £5,000 plus VAT.

- The input tax of £1,000 cannot be claimed because it wholly relates to exempt activities.

- But what if the advert is amended to include the phrase: ‘We will also sell your house if you are thinking of moving.’

- This amendment, which might only take up 5% of the advertising space, transfers the input tax from ‘exempt’ to ‘residual’ because there is now a ‘direct and immediate’ link between the advert and both taxable and exempt activities.

What is meant by the phrase ‘direct and immediate’ link?

The phrase ‘direct and immediate link’ made its debut in the landmark ECJ case of BLP (Case C-4/94) and has largely stood the test of time.

For example, if you trade as a non-profit making theatre company, making exempt supplies of ticket sales for shows, you will probably pay a range of different production companies, which will be subject to VAT.

So, would it be possible to argue that the input tax on the fees should be treated as ‘residual input tax’ on the basis that if the show is good, then both exempt ticket sales and taxable bar sales will increase?

This argument is logical but the link between the production company costs and bar sales is ‘indirect’ – it is not sufficient to justify the expenditure being treated as residual input tax.

Can you explain the relevance of the partial exemption de minimis rules?

My personal view is that the de minimis rules should be abolished because they give a potential input tax windfall of £7,500 each year on costs that relate to exempt supplies.

The main de minimis test is that exempt input tax must be less than £625 per month on average and also less than 50% of total input tax. The annual adjustment calculation always supersedes the quarterly calculations – hence why £7,500 is the relevant figure.

The rules can be used to the advantage of a business owner. Think of a sole trader retailer who also owns a flat that he rents out on a buy-to-let basis. The flat is owned in the same legal entity as his business, so is part of his VAT registration. The rental income is exempt but a careful use of the de minimis rules will create an opportunity to claim input tax on the costs of the flat, including building repairs and improvements.

I advised a business a number of years ago to spread the cost of building works over two different partial exemption tax years to utilise two de minimis limits. But the legal entities must be the same. If a sole trader jointly owns a property with his wife or civil partner, the property income is earned as a partnership; i.e. a different legal entity to the main sole trader business.

Finally, don’t forget that ‘exempt input tax’ includes both input tax on costs that directly relate to exempt supplies and also the proportion of the residual input tax that is not claimed.

And, as a final tip, there are three de minimis tests, so if the main test doesn’t work, there are two other lifelines, so to speak (see VAT Notice 706 s 11).