Personal property tax unlocked

Share this article

Calculating SDLT rates on property purchases by individuals can be a complex business, explains Jo White

Key Points

What is the issue?

Stamp duty land tax applies to property purchases by individuals on all transactions in England and Northern Ireland.

What does it mean to me?

The introduction of a surcharge rate, multiple dwellings relief, first-time buyers’ relief and issues related to mixed use mean that all elements must be considered before advising a client.

What can I take away?

A good rule of thumb is to assume that the surcharge rate applies, unless you can prove otherwise.

In my previous article, I considered the basic fundamentals of stamp duty land tax (SDLT). This article applies those principles to property purchases by individuals.

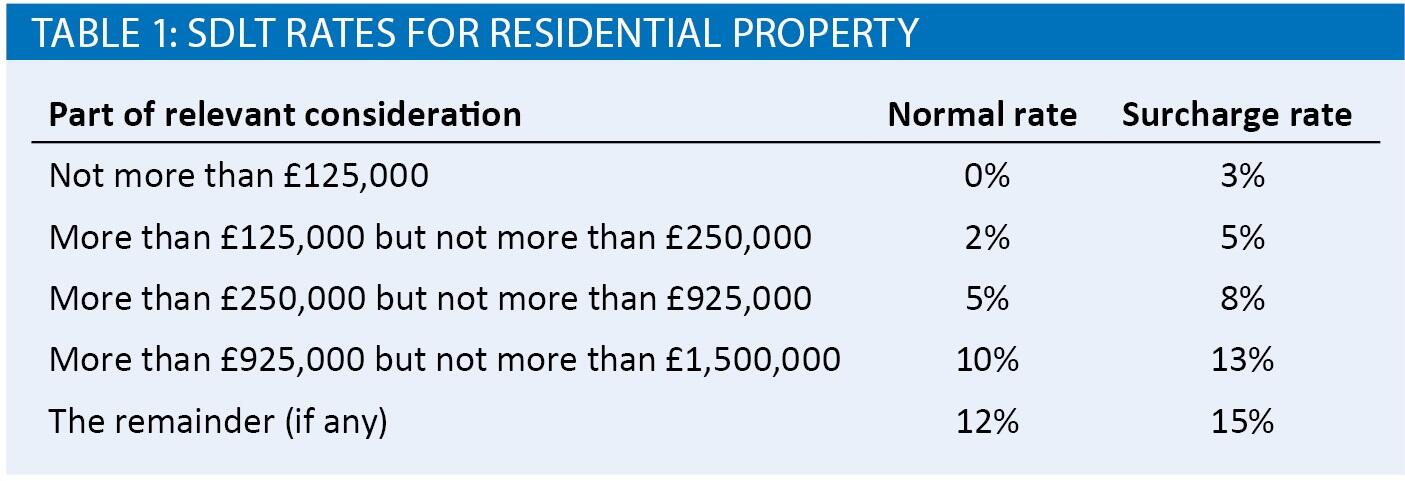

The default position for residential purchases is shown in Table 1, as featured in FA 2003 s 55. However, under FA 2003 Sch 4ZA, a new surcharge rate has been introduced for transactions with an effective date of 1 April 2016, with special provisions in place for properties which exchanged around 25 November 2015. Under the surcharge rate, SDLT is only payable where consideration is £40,000 or more. If consideration is at least this amount but less than £125,000, then SDLT is payable on the whole amount at 3%.

FA 2003 Sch 4ZA will not apply where one of the two exemptions are met, which are:

- The property purchased is not an additional dwelling.

- The property purchased is to replace the purchaser’s main home. In this instance, the purchaser can have an interest in any number of other residential properties and still be exempt from the surcharge rate.

FA 2003 Sch 4ZA uses the terminology ‘dwelling’ in determining if the surcharge rate applies. For this purpose, ‘dwelling’ is not defined in the legislation but HMRC have included their interpretation of the term in their guidance:

‘“Dwelling” takes its everyday meaning; that is a building, or a part of a building that affords those who use it the facilities required for day-to-day private domestic existence. In most cases, there should be little difficulty in deciding whether or not particular premises are a dwelling.’ [SDLTM09750]

HMRC go on to say that a dwelling also includes buildings under construction that are being built or adapted for such use. Off-plan purchases can also count towards the definition of a dwelling. Some key points to note:

- An overseas property will be classed as an interest in a residential property for the purposes of this charge.

- A purchaser can look back up to three years from the effective date of transaction to see if a qualifying dwelling was sold and therefore the replacement home criteria has been met.

- A purchaser can claim a refund of the surcharge rate where they sell their former home within three years of the effective date of purchasing their new main residence.

- If the property is being acquired with another person, the surcharge rate could apply to the whole transaction when the second person owns an interest in another property and the main residence exemption does not apply to them.

- Spouses and civil partners are treated as one for this purpose. Therefore, even if one party to the relationship does not own another property, they will be treated as doing so if their spouse or civil partner does.

- Where properties are being acquired by trustees, the type of trust will have an impact on whether the surcharge rate will apply.

- There are special rules for spouses and civil partners purchasing property from one another.

- There are special rules of property transfers on divorce or the dissolution of a civil partnership.

In all of these circumstances, the rules set out within the legislation are very comprehensive. It is therefore important that all elements are considered before advising a client whether the surcharge rate does or does not apply. A good rule of thumb is to assume that the surcharge rate applies, unless you can prove otherwise.

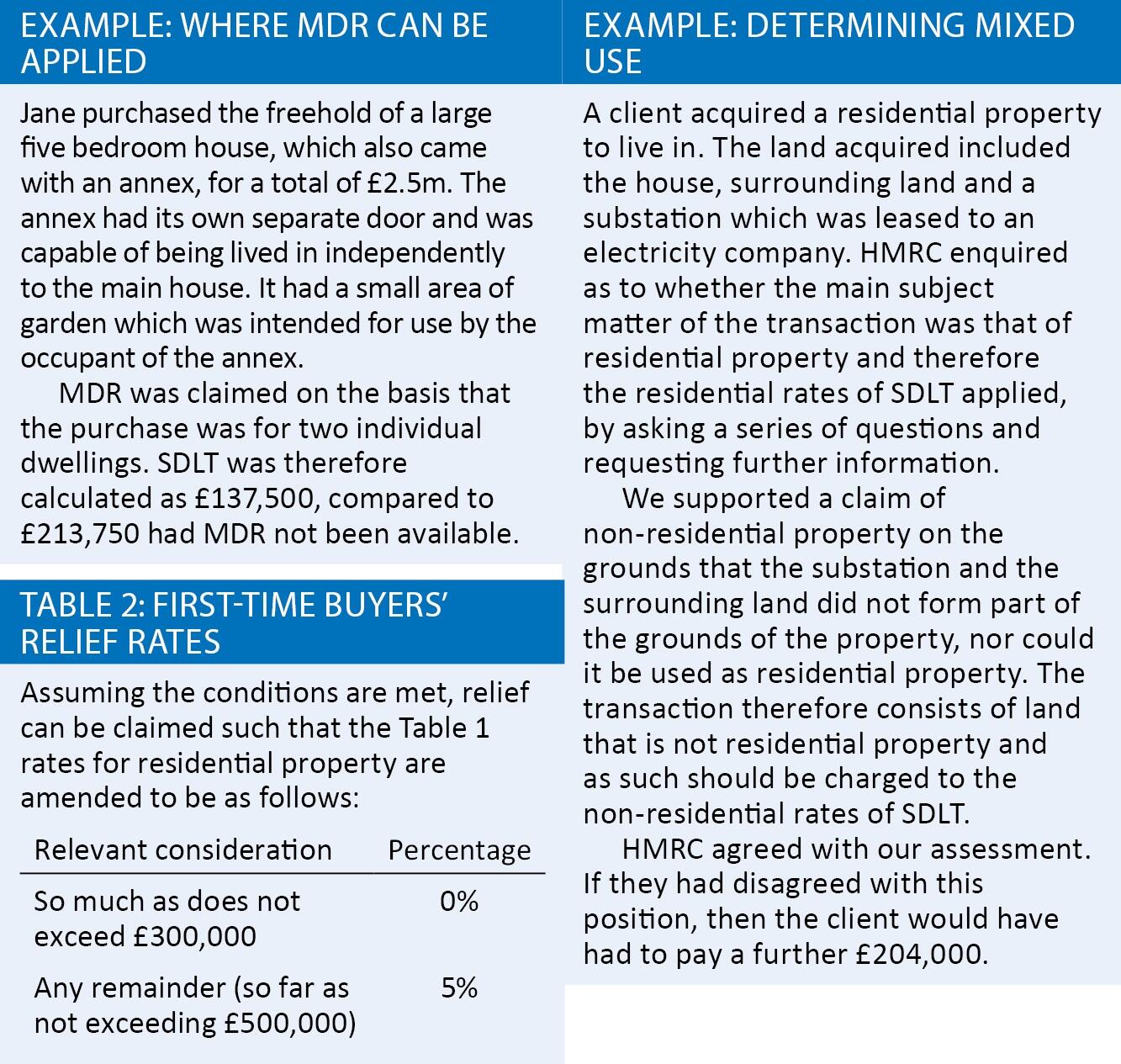

Multiple dwellings relief

This is one of the more widely known reliefs, but it is not always considered at the time the transaction takes place. Where two or more residential properties are acquired in a single transaction (or linked transactions), then it is possible to apply an averaging calculation to determine what SDLT is payable. This is subject to a minimum rate of 1%.

FA 2003 Sch 6B sets the scene for this relief. Under s 2(2), to qualify the main subject matter must consist of:

- an interest in at least two dwellings; or

- an interest in at least two dwellings and another property.

Alternatively, the main subject matter could be an interest in a single dwelling, but forming part of a linked transaction with another (s 2(3)).

Para 7 of the same part defines ‘dwelling’ for this purpose. This is a similar definition to that of the surcharge rate but goes on to state:

- Land that is, or is to be, occupied or enjoyed with the dwelling, such as a garden or grounds (including any building or structure on such land), is taken to be part of the dwelling.

- Land that subsists, or is to subsist, for the benefit of the dwelling is taken to be part of the dwelling.

Where the transaction involves non-residential property, then multiple dwellings relief (MDR) will be calculated on the consideration attributable to the dwellings only. The apportionment would be applied on a just and reasonable basis.

The most common type of transaction I see in MDRs is when a property is acquired with an annex. In order for the annex to be considered, it must be a separate self-contained dwelling in which the residents can live independently of the rest of the building with individual access and domestic facilities such as a kitchen, bathroom, etc. In the context of the surcharge rates, HMRC confirm that this is also their opinion on this position (SDLTM09755).

Where an annex is purchased with another property, then the surcharge rate would not automatically apply providing it fits within the definition of a ‘subsidiary dwelling’.

It is important to note that MDR can be withdrawn if, within three years of the effective date of transaction, the purchaser changes the number of dwellings previously acquired; e.g. if the purchaser knocked through two semi-detached houses to make a single larger one.

Where a property to which MDR has been claimed is sold to an unconnected party, then the three year ‘clock’ ends. If a property is sold to a connected party, then MDR can still be withdrawn if that connected party later alters it in any way within the three years from when the original person acquired it.

First-time buyers’ relief

Introduced in November 2017 (in FA 2003 Sch 6ZA), first-time buyers’ relief reduces the SDLT burden on qualifying purchases by qualifying individuals. In order for a property transaction to be eligible for the relief, the following conditions must be met (Part 1 paras 2 to 6):

- the main subject matter of the transaction consists of a major interest in a single dwelling;

- the relevant consideration (other than any consisting of rent) is not more than £500,000;

- the purchaser (or if more than one, each purchaser) is a first-time buyer who intends to occupy the purchased dwelling as their only or main residence; and

- the transaction is not linked to another land transaction, or if linked, is only done so if it is:

- an interest in land that forms part of the garden or grounds of the dwelling; or

- a right over land that subsists for the benefit of the purchased dwelling, or land that forms part of the garden or grounds of the dwelling.

First-time buyers’ relief is not available where the chargeable transaction is a higher rate transaction for the purpose of Sch 4ZA para 1. Like with most SDLT reliefs, first-time buyers’ relief can be withdrawn but only where a subsequent transaction is linked to this first.

Mixed use

As a firm, we are seeing more and more cases where HMRC are disagreeing that the non-residential rates of SDLT apply. Despite even their own guidance, their default position used to be that any transactions which involve residential property is subject to the residential rates, potentially therefore resulting in the surcharge rate applying.

FA 2003 s 55 states that ‘Table B: Non-residential or mixed rates’ apply ‘if the relevant land consists of or includes land that is not residential property’. There is no definition as to the amount of non-residential land that needs to be included in the transaction before the Table B rates can apply. Purchasing a house with 40 acres of agricultural land should therefore fall within this definition; therefore, the lower rates of SDLT would apply to the whole transaction. However, despite HMRC’s own guidance in their manuals, their previous approach seemed to be the opposite of this.

HMRC have issued enquiry letters on land transactions where they are asking questions which are not pertinent to the SDLT position. For example, they may ask for:

- an explanation of the non-residential activity the purchaser is to undertake on the land;

- copies of documentation supporting the mixed-use selection, including contracts for third party use before and immediately after the effective date of sale; and

- evidence of the vendor’s non-residential use immediately prior to the effective date of sale and the purchaser’s continuation of the same non-residential activity.

None of the above requests for evidence answer the questions HMRC needed to be asking when determining if the non-residential SDLT rate can apply. The legislation does not require there to be a non-residential activity on the land to qualify as non-residential. Furthermore, there is neither a third party use requirement, nor a requirement for the purchaser to continue the activity on the land after the transaction has completed. We would expect such questions from HMRC when they are considering other taxes, but not for SDLT.

It is always important that in cases like this you ensure that the questions being asked, and arguments being put forward by HMRC, are in line with the appropriate legislation. You should not simply take HMRC’s challenge to any claim as being the final result.

New HMRC guidance on mixed use properties

On 1 October 2019, HMRC released some new guidance on their interpretation of the definition of mixed use properties. This is contained within SDLTM00360 to SDLTM00430.

The new guidance seeks to make it clearer as to what HMRC’s view is on property transactions which are beyond your typical residential property purchases. It is important to bring to your attention at this time HMRC’s other recent guidance (SDLTM00440 – SDLTM00480) in this context. This relates to what they consider to be ‘gardens and grounds’ for the purpose of identifying residential property as defined within FA 2003 s116.

What is interesting about HMRC’s new guidance on mixed use properties is that it isn’t significantly different to what we understood their position to be in the past. I am therefore hoping the level of questions based on future use reduce considerably in this respect. In SDLT00380, they state: ‘Any future intention of the purchaser to use the dwelling for non-residential purposes is irrelevant for the purposes of s 116(1)(a).’

They do now break it down into two distinct categories: being used as a dwelling or suitable for use as a dwelling (Category 1); and in the process of being constructed or adapted for use as a dwelling (Category 2).

Key points to consider here are that just because it isn’t a residence at the effective date does not mean it isn’t suitable for use as a dwelling at the effective date of transaction. Longstanding past use will be considered. For example, if the last use was a dwelling, it is more likely their position is that the property is still suitable for the same use if the building is largely the same as it was. Other factors include whether there are any public or private legal conditions (such as planning permission) affecting the use of the property; for example, a holiday chalet that can only be used as a dwelling for short term visitors. Council tax and business rates will play a part in their review of suitability for use and if the property is no longer habitable then there is a clear argument it cannot be residential property. This latter part is worth considering in the context of the case PN Bewley Ltd v HMRC [2019] UKFTT 65.

HMRC have confirmed that ‘in the process of being constructed’ does mean it has to be physically underway for this category to apply; planning permission in its own right is not part of this process.

In light of Hyman v HMRC [2019] UKFTT 469, we may see more challenges on what is considered mixed use properties from HMRC. It is therefore important that the facts of the case are reviewed thoroughly before any claim for mixed use properties are made in this context.