Back to basics: principles of stamp duty land tax

Share this article

In a back to basics review of stamp duty land tax, we consider which transactions are chargeable, property purchases by UK resident and non-UK resident individuals, and corporate acquisitions.

Key Points

What is the issue?

This article reminds us of the basic principles we need to bear in mind when considering stamp duty land tax on land transactions in England and Northern Ireland.

What does it mean for me?

Stamp duty land tax is applied to the acquisition of a chargeable interest in England and Northern Ireland for consideration or deemed consideration.

What can I take away?

Stamp duty land tax is payable within 14 days from the effective date of transaction. ‘Effective date’ is when the contract is substantially performed. In most cases, this is completion.

With the ever-changing landscape in property taxes, this article reminds us of the basic principles we need to bear in mind when considering stamp duty land tax on land transactions in England and Northern Ireland. Land transactions in Scotland and Wales are covered by their own taxes.

All statutory references are to Finance Act 2003 unless otherwise stated.

Exempt transactions

Before we go into the detail behind how and when stamp duty land tax is charged, we must first look at those transactions which we can disregard for this purpose. Schedule 3 includes a specific list of exempt transactions. Some of the more common ones are:

- no chargeable consideration (except for cases where s 53 applies);

- transactions in connection with divorce;

- assents and appropriations by personal representatives; and

- variation of testamentary dispositions.

It is normally pretty clear whether or not stamp duty land tax is expected to be payable on a transaction. It is, however, always worth checking that the exemptions can be applied.

Chargeable transactions

Stamp duty land tax is applied to the acquisition of a chargeable interest in England and Northern Ireland for consideration or deemed consideration. Chargeable interest is defined within s 48 to mean:

a) an estate, interest, right or power in or over land in England or Northern Ireland; or

b) the benefit of an obligation, restriction or condition affecting the value of any such estate, interest, right or power other than an exempt interest.

An exempt interest is any security interest (i.e. a mortgage), a licence to use or occupy land, a tenancy at will, an advowson (right to appoint a clergyman or vicar), franchise or manor.

A right over land can include an option (s 48 explains this further) and overage therefore it is not just the ‘normal’ sale of the land itself or long leases.

Consideration

Chargeable consideration (Sch 4), except where expressly stated, is any consideration in money or money’s worth given for the transaction. This can be either directly or indirectly by the purchaser or a person connected with them (Sch 4 para 1). Stamp duty land tax is chargeable on the VAT inclusive price (Sch 4 para 2). This will largely be relevant for non-residential transactions only. The timing of the transaction and any option to tax election on the specific property will be important to determine if VAT should be considered. Where the transaction is deemed to be taking place at market value, then this will not include any VAT.

For circumstances where non‑monetary consideration is applied, the value for this is its deemed market value. Non-monetary consideration can include fees, carrying out works or services (see Example 1: A transaction where consideration is not wholly money). Special rules apply in circumstances including, but not limited to:

- where a repayment or assignment of debt forms part of the transaction (Sch 4 para 8) (See Example 2: Repayment or assignment of debt forms part of the transaction);

- in the event of contingent consideration (s 51);

- where the purchaser is a company and the vendor is connected with them – deemed market value (s 53). ‘Connected’ is defined under Corporation Tax Act 2010 s 1122.

Image

Linked transactions

Where transactions are linked, the total aggregate consideration is calculated to work out any stamp duty land tax payable (s 108). Transactions are linked for the purpose of stamp duty land tax where they form part of a single scheme, arrangement or series of transactions between the same vendor and purchaser or persons connected with them. (Again, connection is defined in Corporation Tax Act 2010 s 1122.)

There is no time limit for these rules to apply. A transaction between the same vendor and purchaser could be linked even if they had taken place over 20 years apart. An important question to ask is: ‘Would the transactions have taken place independently of each other?’ Linked transactions are more likely to apply if the purchase price for one property has been discounted due to the acquisition of a second.

For properties acquired at auction we can look to the case Cohen & Anor [1936] 2 KB 246, which states these will not constitute a larger transaction or series of transactions.

Due date for payment

Stamp duty land tax is payable within 14 days from the effective date of transaction. ‘Effective date’ is when the contract is substantially performed. In most cases, this is completion; however, this is not always the case. ‘Substantially performed’ is defined in s 44(5) as when:

- the purchaser (or a person connected with the purchaser) takes possession of the whole, or substantially the whole, of the subject matter of the contract; or

- a substantial amount of consideration is paid or provided.

Things to note here are:

- A contract must exist for the effective date to be earlier than completion.

- Possession can include the receipts of rents or profits or rights to receive them (s 44(6)).

- When looking at a transaction involving rent, substantial amount can include the first payment of rent (s 44(7)).

- For non-rent-based transactions, HMRC guidance suggests 90% in the context of ‘substantially the whole’.

In circumstances where the vendor allows the purchaser to access the land, this could also bring forward the effective date.

Property purchases by UK resident individuals

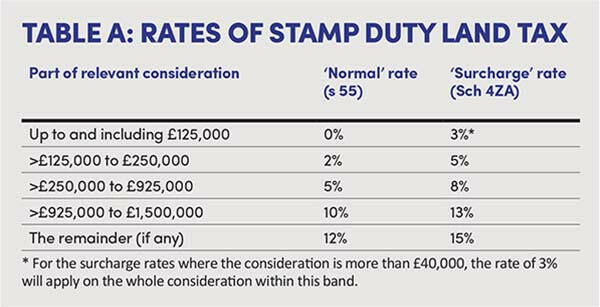

The default position for residential purchases is that shown in s 55 (Table A). However, we must also look to Sch 4ZA to see whether the surcharge rate needs to be applied.

Residential property

Residential property is defined within s 116 as:

- a building that is used or suitable for use as a dwelling, or is in the process of being constructed or adapted for such use; and

- the land that forms part of the garden or grounds of such a building; or

- an interest in or right over land that subsists for the benefit of a building within (1) and (2) above.

The tests within the legislation refer to actual and suitability for use. The use for which the purchaser intends to apply after the transaction date is almost always irrelevant.

HMRC states that:

‘“Dwelling” takes its everyday meaning; that is a building, or a part of a building that affords those who use it the facilities required for day-to-day private domestic existence. In most cases, there should be little difficulty in deciding whether or not particular premises are a dwelling.’ (SDLTM 09750)

It goes on to say that a dwelling also includes buildings under construction that are being built or adapted for such use. Off-plan purchases can also count towards the definition of a dwelling.

Whilst it is easy to identify the garden, it is sometimes harder to identify the grounds. HMRC guidance state that:

‘“Garden or grounds” includes land which is needed for the reasonable enjoyment of the dwelling, having regard to the size and nature of the dwelling. This is usually question of fact depending on the individual circumstances of the case.’ (SDLTM 30030) [my emphasis]

HMRC has confirmed that land which was part of a residential property remains that way even if it is sold separately.

If at the effective date of transaction there is no longer a residential building as it is derelict or demolished, then those grounds and gardens are no longer residential. In order for the property not to be suitable for occupation as a dwelling, it cannot be physically habitable.

Rates of stamp duty land tax

The stamp duty land tax rates for the residential property acquisitions by UK resident individuals are shown in Table A: Rates of stamp duty land tax. Special exceptions to the surcharge rates exist where:

- The property purchased is not an additional dwelling.

- The property purchased is to replace the main home, even if the purchasers own an interest in another dwelling(s). Please note specific rules apply to other property interests which are inherited.

- The transaction is between spouses or civil partners if they are the only parties to the transaction and they are still living together.

- The purchaser is acquiring an additional interest in the same property to which they have an interest, and that property is their main residence.

Some key points to note:

- An overseas property will be classed as an interest in a residential property.

- A purchaser can look back up to three years from the effective date of transaction to see if a qualifying dwelling was sold and therefore the replacement home criteria has been met.

- A purchaser can claim a refund of the surcharge rate where they sell their former home within three years of the effective date of transaction of purchasing their new main residence.

- If the property is being acquired with another person, then the surcharge rate could apply to the whole transaction where they own an interest in another property and the main residence exemption does not apply to them.

- Spouses and civil partners are treated as one for the purpose of this part of the legislation. Even if one party to the relationship does not own another property, they will be treated as doing so if their spouse or civil partner does.

- Where trustees are acquiring properties the type of trust will impact the rate of stamp duty land tax payable.

- There are special rules of property transfers on divorce or dissolution of a civil partnership potentially restricting only one party being able to apply the replacement residence rules depending on the order of the transactions.

A good rule of thumb is to assume that the surcharge rate applies, unless you can prove otherwise.

Corporate acquisitions

Companies are always subject to the surcharge rate of stamp duty land tax for the purchase of a major interest in a dwelling.

Furthermore, the higher rate of stamp duty land tax (Sch 4A) could apply where consideration is in excess of £500,000. This means that 15% is initially charged on the whole consideration, not just the value in excess of £500,000.

Reliefs exist against this charge, but they need to be claimed. Where a claim can be made then the surcharge rates become due. Under Schedule 4A, these include:

- property rental business (para 5);

- business of trading in or redeveloping properties (para 5);

- making a dwelling available to the public (para 5B);

- financial institutions acquiring dwellings (para 5C);

- dwelling for occupation by certain employees (para 5D);

- flat occupied by a caretaker (para 5EA); and

- farmhouses (para 5F).

These reliefs can be withdrawn if the properties use changes within three years of the effective date of transaction, even if it is to another relievable activity.

Purchases by non-UK residents

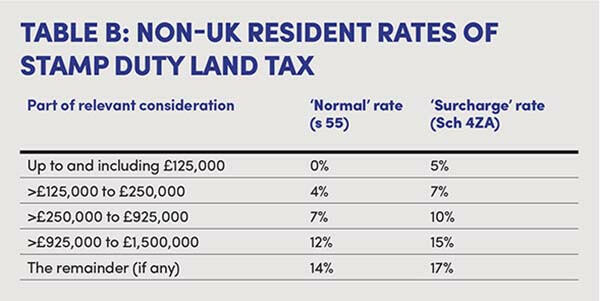

The non-resident stamp duty land tax rules were introduced for property transactions with an effective date on or after 1 April 2021 (Sch 9A).

Where the purchaser is considered a non-UK resident, then an additional 2% rate is applied to the underlying residential property rates, as shown in Table B: Non-UK resident rates of stamp duty land tax. The rate of stamp duty land tax under Sch 4A is 17% for properties with consideration of more than £500,000. This is subject to the relevant reliefs being available.

Whether or not the purchaser is non-UK resident for stamp duty land tax purposes is judged based on the effective date of transaction. A non-UK resident for stamp duty land tax purposes is defined differently to the rules set out in the statutory residence test, used for the purpose of income tax and capital gains tax. Nationality or citizenship are not considered. Visa policies or the right to reside rules are not also relevant in these circumstances.

Where the property is acquired by more than one purchaser, then the non-resident rates of stamp duty land tax will apply if only one of them meets the non-UK residence tests. The only exception is for married couples or those in civil partnership where one party is UK resident (Schedule 9A part 5 para 12).

The tests for the main types of purchasers can be set out as follows:

Individual purchaser: An individual is considered non-UK resident if they are not present in the UK for at least 183 days in the 12 months before the purchase. An individual is UK resident where you are present in the UK at midnight (Sch 9A Part 3). Special rules exist for spouses and civil partners.

Trust: The residency position of the trustee is relevant. The exception being where the trust is a bare trust or the beneficiary is entitled to remain in the property for life or entitled to income arising from the purchased property. In these circumstances, the residency of the beneficiary is considered (Sch 9A Part 5 para 14).

Corporate purchaser: Corporate purchasers are considered non-UK resident if they are not UK resident for corporation tax purposes. This is a look back test only. Special rules exists under the company residency definition where a non-UK resident person directly or indirectly owns a UK company. Such companies are treated as non-resident in where the company:

- is a close company – the same definition as corporation tax is applied here;

- meets the non-UK control test in relation to the transaction; and

- is not an excluded company (Sch 9A Part 4)