Practical VAT tips with bad debts

Share this article

Neil Warren explains the bad debt relief rules for both suppliers and customers and shares a VAT saving tip with the flat rate scheme

Key Points

What is the issue?

The bad debt relief rules are intended to ensure that VAT is not a cost to a business that suffers a bad debt following non-payment by customers. The article considers the procedures for claiming VAT and the relevant time limits and also the need for customers to adjust input tax on unpaid purchase invoices in some cases.

What does it mean to me?

There is a potential VAT windfall on bad debts if a business uses the flat rate scheme, even if it uses the cash based turnover method where VAT is not included on a return until an invoice has been paid. It is important to be aware of this opportunity and how it

works in practice.

What can I take away?

If a business joins the cash accounting scheme, then bad debt relief is automatic. But the disadvantage of the scheme is that input tax cannot be claimed on purchase invoices until suppliers have been paid.

Despite a general healthy economy, there are still many businesses that have suffered recent bad debts. They might have supplied goods or services to some of the high profile casualties that have gone into liquidation in recent years, a major travel company being the most recent example. There is nothing more frustrating for a business than a bad debt but the good news is that the VAT element of unpaid sales invoices should not be a problem if the relevant rules for bad debt relief are properly followed.

I’ll review these rules in this article and also consider a historic court case that clarified the rules for bad debt relief and VAT only invoices. And as a bonus for smaller businesses, there is an unexpected tax windfall for users of the flat rate scheme (FRS) as far as bad debts are concerned.

Basic rules

A business can claim bad debt relief on a VAT return (positive entry in Box 4) when all the following conditions are met:

- The sales invoice in question is more than six months overdue for payment.

- The invoice has been written off in the business records; i.e. the customer’s sales ledger account has been credited and a bad debt expense account is created.

- Output tax must have been paid to HMRC on a past VAT return.

- The debt must not have been sold, factored or paid under a valid legal assignment.

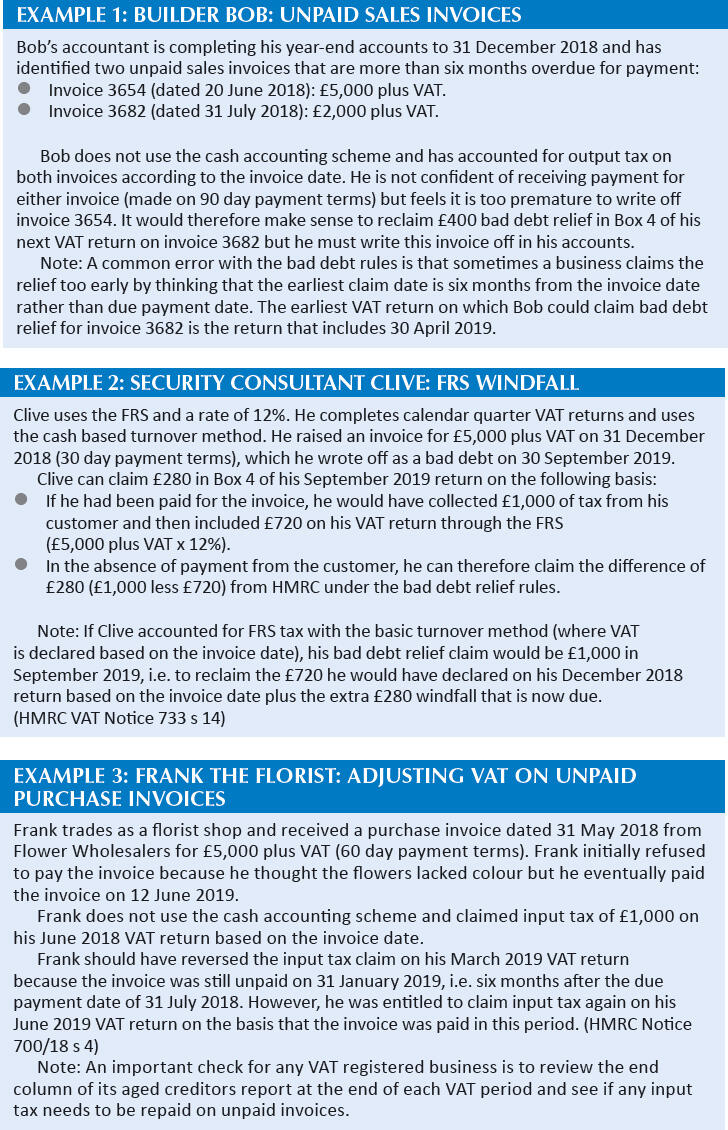

The latest time a claim can be made is four years and six months after the later of the time of supply (usually invoice date) or due date for payment. If an invoice is written off and bad debt relief has been claimed, then output tax must be declared on any payment subsequently received from the customer (HMRC Notice 700/18 para 2.2). See Example 1: Builder Bob: unpaid sales invoices. Note that in cases where the customer makes a round sum payment that is not allocated to specific sales invoices, then the payment should be allocated to the oldest unpaid invoices first.

Cash accounting scheme

An easy solution to avoid a bad debt relief problem is to join the cash accounting scheme. Bad debt relief is automatic with the scheme because output tax is only declared on a return when payment has been received from a customer. However, a downside of the cash accounting scheme is that input tax cannot be claimed until a supplier has been paid:

- A business can join the scheme if it expects taxable sales in the next 12 months to be less than £1.35m (excluding VAT).

- If a business uses the FRS, it cannot use the cash accounting scheme but it can adopt the cash based turnover method, which means that the payment date for sales invoices is again relevant (VAT Notice 733 s 9).

- A business must leave the scheme if, at the end of any VAT period, annual taxable sales excluding VAT have exceeded £1.6m. This fi gure includes the sale of capital assets.

Tribunal case: VAT only invoices

If you act for either a car repair business or a legal firm, it is possible that they will raise VAT only invoices, usually in relation to insurance work. Think about the situation where a VAT registered car owner is involved in an accident (his fault) where his vehicle repair is the subject of an insurance claim. The repair business will invoice the insurance company for the net amount of the job (let’s say £3,000) and invoice the VAT amount (£600) to the business owner as a VAT only invoice. The latter business can claim input tax as a business expense (assuming it is not exempt or partly exempt). But what happens if the car repair business is never paid for this VAT only invoice?

The above question about bad debt relief on VAT only invoices did the rounds in the tribunals a number of years ago in a case involving law firm Simpson and Marwick.

After three different tribunal hearings, it was finally established by the Court of Session in Simpson & Marwick [2013] CSIH 29 that the bad debt relief for a VAT only invoice was 1/6 of the VAT figure and not the full amount of VAT. This seems very logical: if a business makes a supply of £3,000 plus £600 VAT and receives payment of £3,000, it seems correct that the bad debt relief would be £100, i.e. output tax is still payable on the amount of £3,000 received from the insurance company (£3,000 x 1/6 = £500).

Flat rate scheme

If a business uses the FRS and only accounts for tax when it receives payment from its customers, it has adopted the cash based turnover method which I mentioned above. You might think that bad debt relief is irrelevant because no VAT is due if an invoice is unpaid. However, a quirk of the FRS (very good news) is that there is some bad debt relief to claim in this situation. See Example 2: Security consultant Clive: FRS windfall.

Unpaid purchase invoices

The bad debt relief rules affect customers as well as suppliers. The regulations require input tax to be credited by the customer on the VAT return relevant to the date when a purchase invoice becomes more than six months overdue for payment (negative entry in Box 4). But the good news is that input tax can again be reclaimed by the customer if he pays the invoice in the future. See Example 3: Frank the florist: adjusting VAT on unpaid purchase invoices.

Final tip

As a final tip on input tax adjustments, I recently encountered an incredible own goal scored by a partly exempt business. The business wrote off some unpaid purchase invoices on its aged creditors report, and reduced the input tax figure on its next VAT return.

The only problem was that it had never claimed input tax on these invoices in the first place because they wholly related to exempt supplies. The lesson here is that you should never forget the quirks and pitfalls of partial exemption!