Prepare for attack!

Share this article

George Gillham provides guidance on dealing with clients at risk of criminal investigation

Key Points

What is the issue?

HMRC and the CPS are making a concerted effort to change taxpayer behaviour at the riskier end of tax avoidance. One of the forms this is taking is the shifting of focus of criminal investigations from promoters of tax schemes to investors in them.

What does it mean to me?

Clients who have gone for tax avoidance structures that fail the ‘smell test’ now run a real risk of criminal investigation and arrest. If those clients are regulated professionals the result is often personal ruin even if they are ultimately acquitted.

What can I take away?

If you have a client who has bought into a tax efficient structure at the riskier end of the spectrum, and the enquiry ‘goes quiet’, consider whether they need advice from a specialist lawyer sooner rather than later; or it may be too late to help them.

HMRC describes evasion as ‘illegal activity, where registered individuals or businesses deliberately omit, conceal, or misrepresent information in order to reduce their tax liabilities’. This is distinct from ‘Criminal attacks’ (smuggling and MTIC fraud) and the ‘hidden economy’ (ghosts and moonlighters). This article is concerned with ‘evasion’ in the HMRC sense.

The politico-legal climate

HMRC exist to raise revenue. Prosecutions of taxpayers for evasion are extremely resource-intensive and uncertain of success. Historically, therefore, criminal investigations and, especially, prosecutions have been a side-show; reserved for the most egregious offenders; with prosecution success rates of well over 90%. Everyone else was dealt with under COP8, COP9, or one of theDisclosure Facilities.

The exception to this general rule was when particular types of tax avoidance or evasion became hot topics politically (or fiscally) and Ministers decided that ‘something needed to be done’. Typically, when the particular type of avoidance or evasion was no longer ‘flavour of the month’ the strategy was dropped.

However, in September 2010, the new coalition government pledged to make funding available to HMRC for a five-fold increase in criminal prosecutions for tax evasion. In January 2013 the DPP promised a seven-fold increase in the number of prosecutions for non-organised tax crime. This focus has been sustained. Despite reservations about the cost-effectiveness of this strategy from the National Audit Office (December 2015) further funding was announced in Budget 2015 for the explicit purpose of enabling HMRC to triple the number of criminal investigations that it can undertake into tax crime.

So: a political decision has been made that more resources are going to be expended, on an ongoing basis, on pursuing people criminally for evasion. It is not that more tax offences are being committed. It is that more resources are available to pursue existing individuals. The CPS and HMRC have had to put their heads together to decide how they are going to meet these targets. The decision has been to push beyond what have previously been seen as the ‘safe boundaries’ (i.e. cases with an extremely high chance of conviction). We are in a ‘new normal’ where HMRC will criminally investigate, and the CPS will proceed to charge, much more frequently. This means that your clients are at greater risk.

‘Perhaps,’ I can hear the HMRC and the CPS musing, ‘we should pursue someone other than just the multipliers. Perhaps we can pursue the investors? Perhaps someone who invests in an asymmetric loss creation scheme, looking to make a tax-deductible loss, on the grounds that they are not “trading with a view to profit” because the profit is mathematically extremely unlikely to happen and they know it? If they claim a loss on their tax return, aren’t they conspiring with the IFA or tax adviser to cheat the public revenue? Or, perhaps we could use one of the statutory offences? Let’s see if it flies with a jury…’

The figures

HMRC uses a range of interventions to tackle tax fraud: running publicity campaigns and direct communications; encouraging tax evaders to settle their tax affairs using disclosure facilities; using task forces; undertaking civil investigations; and pursuing criminal investigations with a view to prosecution.

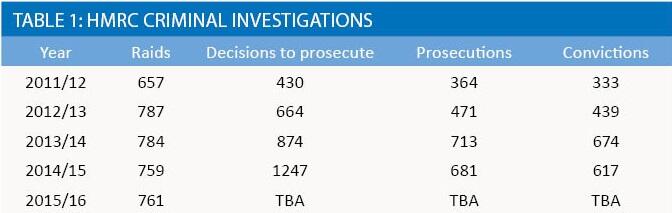

Fieldfisher tracks a number of figures that reveal the extent of HMRC’s criminal investigations activity in relation to evasion. We track the number of warrants executed by HMRC (‘raids’); decisions by the CPS to charge for tax offences (‘decisions to prosecute’); prosecutions; and convictions for tax offences in the courts (‘convictions’). We exclude cases revolving around tax credits offences.

All four number are tracked because each gives a different take on the success or failure of the criminal process and because the cycle takes several years.

We obtained by way of requests under the Freedom of Information Act the complete figures for the four tax years from 2011/12 to 2014/15, using these definitions as set out in Table 1.

I’ve updated for 2015/16, where we currently only have the figures for raids.

The indications are that the HMRC criminal investigations team has reached maximum capacity, with the number of raids steady the last four years. We will see if the new money for staff announced in Budget 2015 has any effect on the raids figure in 2016/17 and 2017/18.

However, just on the figures above, the number of decisions to prosecute has risen very sharply – trebling in four years.

I have alluded above to a concern that, absent a significant expansion in the numbers of properly trained HMRC criminal investigations staff, the then DPP’s drive to prosecute more people for tax fraud would (in reality) lead to the CPS taking more risks on prosecutions. The figures set out above would appear to bear that out. Conviction rates would appear to be dropping. So if your client is arrested on suspicion of having committed a tax offence, it is dramatically more likely than it used to be that they will be charged.

Since tax crimes are dishonesty offences, if your client is a regulated professional, it is inevitable that they are going to have their licence to practise suspended. So they will lose their means of earning a living regardless of whether a jury eventually acquits them. If the alleged offence relates to a complicated conspiracy to cheat or defraud (as most tax schemes would if charged) it may take years for the case to come to trial. If your client is acquitted, even if a professional employer will have them back again, getting back the money that they could have earned in the meantime – and getting back all the money they have spent on legal fees – will be effectively impossible.

New structures present new challenges for tax advisers

The challenge that tax advisers (and accountants, and legal advisers) face in trying to advise their clients on the tax efficient arrangement of their affairs is in discerning whether something is lawful or unlawful, and if the latter, whether pursuing the course suggested would render the client liable to civil penalty or criminal penalty.

While I do not create or advise on the creation of structured tax avoidance schemes I am often asked to opine on whether a dispute involving such a scheme is likely to be successful before the Tribunals. It often isn’t. The enhanced scope of Ramsay, especially following the decision of the Supreme Court in the UBS case in March 2016 (UBS AG v HMRC [2016] UKSC 13), means that many structured tax avoidance schemes are unlikely to succeed because the intricate chain of transactions inserted therein do not to have a business or commercial purpose.

I also find myself advising clients that tax avoidance is now unlawful in certain situations. Since 17 July 2013 it is no longer the case that the rule in the Duke of Westminster’s case (‘…every man is entitled if he can to order his affairs so that the tax attracted under the appropriate Act is less than it otherwise would be…’) applies. On that date the GAAR was introduced.

‘Tax arrangements’ are defined for GAAR purposes in section 207(1) Finance Act 2013. Would it be reasonable to conclude that the obtaining of a tax advantage was the main purpose, or one of the main purposes, of the arrangements? If the arrangement is entered into on the advice of a tax adviser or accountant, in response to the query, ‘do you have anything that will reduce my tax bill this year?’ this will automatically be the case; but there will be many other circumstances in which this is also true.

Once one has concluded that this is a ‘tax arrangement’, section 207(2)-(6) Finance Act 2013 apply. If the legislation does not anticipate arrangements resulting in an amount of income, profits or gains for tax purposes that is significantly less than the amount for economic purposes; or arrangements resulting in deductions or losses of an amount for tax purposes significantly greater than the amount for economic purposes; or arrangements resulting in a claim for the repayment or crediting of tax that has not been, and is unlikely to be, paid; then that would indicate that the arrangements contemplated are abusive and thus unlawful.

Without dishonest intent, aggressive tax avoidance still does not render a taxpayer liable to criminal penalties. What constitutes ‘tax evasion’ has not changed. What has changed here is the funding available to HMRC; the likelihood of HMRC challenging a taxpayer they consider might have been dishonest; the chance of HMRC choosing to send the file to the CPS rather than offering COP9; and the chance of the CPS deciding that a prosecution should ensue.

Old structures present new challenges for tax advisers too

In recent years, HMRC has been challenging structures with asymmetric relief which will either make a real profit or make losses and purport to receive tax relief far in excess of the cash sum invested (almost invariably the latter). HMRC get particularly annoyed about leveraged investment opportunities where the leveraged element is not actually risked in the business opportunity concerned (which is many of them).

The reality is that HMRC are right to look suspiciously at some of these structures.

Firstly they exist on a wide spectrum of believability and reality. HMRC believe they rarely if ever work. But some of them have non-existent loan leverage being invested in a non-existent film production. Here the tax relief isn’t available because the activity is a lie, quite apart from whether the structure works from a technical point of view.

Secondly, promoters or investors may have been so aggressive in their structuring of a planned ‘business activity’ that a profit is improbable at a mathematical level of proof; in which case any claim to tax relief should fail as there can be no genuine intention to trade with a view to profit.

Thirdly, even where neither the first or second reason applies, the implementation of the scheme may be so poor as to render the scheme ineffective.

HMRC are re-reviewing many existing tax avoidance enquiries, falling under any of these three heads, through the criminal lens. Every old open enquiry where there is a structure at the ‘less believable’ end of the spectrum is a potential risk here.

Take the innocent-sounding question the taxpayer asked above, ‘do you have anything that would reduce my tax bill this year?’ HMRC could argue that the taxpayer is explicitly interested in reducing their tax bill; that the taxpayer was interested in ‘loss schemes’; that when the taxpayer then entered into a ‘tax efficient business opportunity’ (that generated large losses which the taxpayer sought to offset against their income) the taxpayer was not actually trading with a view to profit; that when the taxpayer claimed a trading loss on their tax return they were not telling the truth; and that the taxpayer was therefore dishonest.

This is pushing the boundaries out, but the funding is there for HMRC and the CPS to push the boundaries out, and this is an actual example of the approach that HMRC is now taking. They are aggressively raiding the businesses of purveyors of tax efficient investments of this nature; and trawling documents for precisely these sorts of exchanges; and arresting, and charging, investors.

The offence which HMRC have traditionally most commonly pursued is ‘cheating the Revenue contrary to the common law’. This is probably because all the prosecution have to prove is that the defendant had dishonest intent to defraud the Revenue. The defendant does not have to have succeeded in doing so, and they do not have to have committed an actual act of deception (see R v Mavji (1987)). The maximum sentence is life imprisonment. Terence Sefton Potter of Aquarius Films, who was the promoter in the Jenkins Hyde & McLellan case (2015), received 8 years for ‘conspiracy to cheat’ and the independent financial adviser in that case, Neil Williams-Denton, 5.5 years. The investors each received 4.5 years. Other prosecutions of investors for ‘cheat’ are ongoing.

We are now also seeing cases of HMRC and the CPS pursuing charges against investors on the basis of fraud by false representation contrary to section 2 of the Fraud Act 2006 – alleging that a claim in the tax return is untrue or misleading, and that the person making it knows that it is, or might be, untrue or misleading – such as a claim that one is actively trading in a partnership where this allegedly is not so. We are not aware of any convictions under this head yet; but the maximum sentence would be ten years imprisonment.

Conclusion

The landscape for tax advisers has changed both politically and legally. Many hitherto legitimate strategies for saving clients tax are no longer so; and some structures from the past are receiving attention from the enlarged and much better resourced HMRC criminal investigations team.

Over and above any refusal by HMRC to accept the tax consequences of such a structure, if there is evidence that the taxpayer has been looking at it as a ‘scheme’ from the start, then the investor runs the risk of HMRC alleging either cheat or fraud by false representation; being arrested; and, at best, having a very uncomfortable series of interviews under caution.

We have been called in many times on civil and COP8 enquiries over the last six years that had ‘gone quiet’ and then had suddenly ‘gone criminal’. We have an excellent record of persuading the CPS not to prosecute in such circumstances; but, because we have to marshal the case in minute detail, this is time consuming and expensive.

So: if HMRC show an interest in your client, and you have serious concerns about the viability of a structure they have used, get them to talk to a specialist lawyer, under the protection of legal privilege, at the earliest possible opportunity.