Public attitudes to tax – who cares?

Share this article

Andy Lymer examines how tax advisers can make a positive contribution to the public debate on taxation

Key Points

What is the issue?

Should we care about public attitudes to how our tax system evolves or is its development something that should be reserved only for those with detailed knowledge?

What does it mean to me?

As tax specialists, each of us has a role in feeding information and perspective into the public debate about tax that is crucial in countering the occasional one-sided presentation of misleading facts by some in the media

What can I take away?

The process of sensible evolution of the tax system needs our help as experts in tax. Is there a way I can contribute to initiatives on tax education or the development of tax literacy that will help more people understand it and the role tax has to play in building our future?

Every five years, or so, when the nation is about to go to the polls, politicians appear to become interested again in the question: ‘Should we really care about public attitudes to tax?’ Although a rich area of research for academics, think-tanks and lobbying groups, it is an issue that all tax professionals should care passionately about too because effective public debate is necessary for a healthy tax system.

Academic work on this subject has been provided two ways: qualitatively, by interviewing people or listening to focus groups to produce a series of cases; and quantitatively by looking for population-wide understanding through statistics to summarise large surveys or other large-scale data sets.

In the latter is work completed last year by the Centre for Household Assets and Savings Management (CHASM) at the University of Birmingham. It undertook a national survey of 2,000 individuals about the wealth tax changes being discussed in the run-up to the general election. The topics covered mansion tax, council tax reform, capital gains tax (CGT) changes, inheritance tax (IHT) thresholds and income tax at the 45% or 50% thresholds as a proxy for a wealth tax. The survey found that IHT, by some margin, continued to be the most disliked of all wealth taxes, which seems illogical given how so few people will ever pay it or will be subject to receipts after someone else has. Less than 4% of estates are subject to IHT each year. Perhaps not unsurprisingly, more people favoured taxes they aspire to having to pay themselves, such as a mansion tax, or CGT and income tax at the additional 45% or 50% rate.

This work also highlighted something that has been evidenced before – that having a proper debate about tax is difficult because of the variable knowledge about the tax system among the general public. Therefore, media campaigns can steer public debate, sometimes with little in the way of evidence to support it or without there being a chance for an alternative opinion to be fairly or reasonably presented.

In 2000 the Fabian Society published the results of a commission it undertook on tax and citizenship. Paying for Progress: A new politics for tax for public spending argued that discussions about tax had become solely about how it should be cut and lacked meaningful political discussion on whether it could be increased and on what. At the heart of this work was a survey of public attitudes to various aspects of the tax system. It highlighted that ‘people felt disconnected from the taxes they pay and from public services which these finance’. This was partly a function of not knowing what is paid and on what it is spent, and partly the feeling that taxes were badly spent. However, it was suggested that this was not an irreversible position – if people knew how money was spent, there was a willingness to pay more tax.

This pre-financial crisis work was updated in another Fabian Society report, Tax for our Times, in August 2015. The editor, Daisy-Rose Srblin, writes in her introduction: ‘The public should be at the heart of debates about tax, but so far they have been crowded out by technocratic and seemingly apolitical contributions dominated by highly qualified specialists.’ I guess those specialists would be those of us who consider ourselves to be tax professionals, and so this could be construed as a criticism of how we engage in the tax development process. However, I would like to think there is plenty of space for both expert discussion of details and a more general discourse about the direction of travel for the tax system – and that is where the public debate should be.

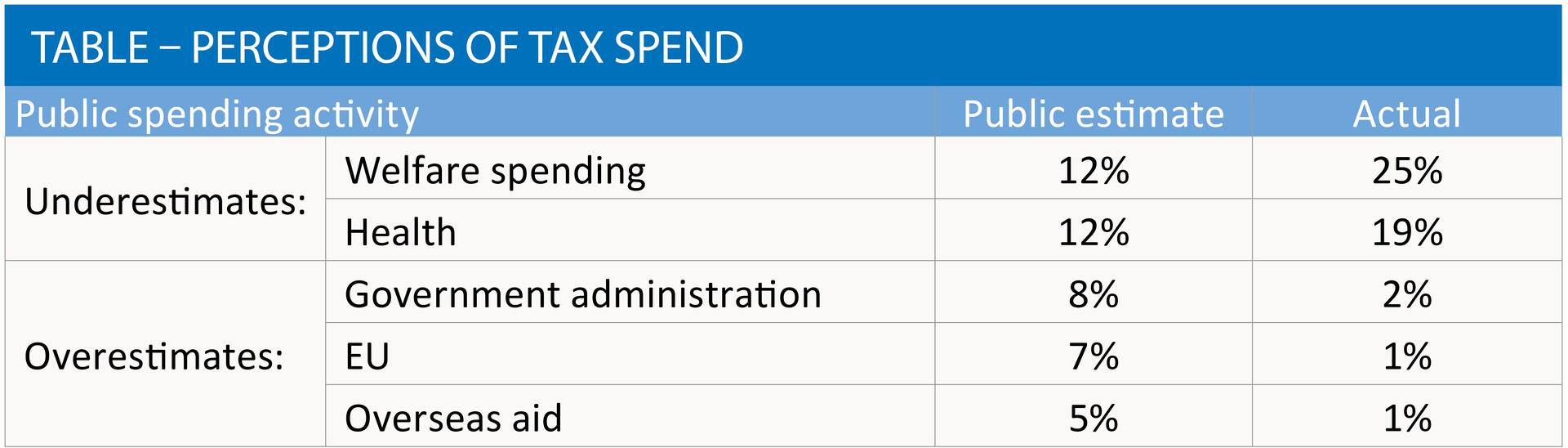

Regular public surveys do appear to support or oppose specific proposals or follow particular changes. In November 2014, YouGov published Perceptions of How Tax Is Spent Differ Widely from Reality, in response to the start of the distribution of personalised tax summarises by HMRC to the first 24 million people in the UK. The YouGov report was one of the specific interventions called for in the Fabian 2000 commission to help reduce the disconnection it highlighted and shows how public perception of tax spend differs from reality (see Table).

In the US the Annual Survey of US Attitudes on Taxes and Wealth has been undertaken by the Tax Foundation since 1937 and produces a rich source of evidence of changing social views. Perhaps there is a need here for a similar yearly systematic study to inform the evolution of our tax system.

Of course, there is little point in stimulating a public debate about tax if the public remains uniformed of the key bases. Here sits the theme of Chris Jones’s call, as this year’s CIOT President, for continued emphasis on tax education and improving levels of tax literacy. This has to be a key role that we tax specialists look to play not only for the end of carrying out our engagement briefs supporting clients or, in my case, helping my ‘clients’ pass their exams, but also to enable public debate to be better informed.

Instead of debating using real facts and examining the challenges of building a workable tax system in a complex world, the press tends to focus on a narrow selection of topics for headline-grabbing purposes. This unhelpful tendency has marked recent debates about corporate tax avoidance or the appropriateness of a ‘mansion’ tax for improving fairness in our tax system. These often one-sided media ‘debates’ have perhaps done as much harm to our profession as they have produced reasoned and clear ways forward that are workable, widely understood and accepted.

Should public attitudes matter? If so, do we have a suitable process for having an informed tax debate from which policy makers can derive a sense of desired direction? I think the answer is yes, they do matter, and matter very much if we wish to continue to develop our ‘modern, democratic’ credentials. However, we have a way to go to ensure debates are well informed and explore a breadth of options that do not merely discuss tax cuts and service provision retrenching, but where it is right and sensible to grow taxes in ways that will create a fairer means of contributing to a fairer society. Academics will continue to play a role in trying to provide that evidence base, I have no doubt. And as the CIOT continues to support such endeavours, including its recent call for research on the impact of tax literacy for example, we hope to continue to chip away at this challenge as a tax profession.

Srblin concludes her introduction in Tax for our Times: ‘Conducting a conversation about tax reform without the public which pays the revenue does not make sense. Tax reform should neither be locked away by politicians from public view, nor left to the expert few.’ I couldn’t put it better myself.

Further information

Centre on Household Assets and Savings Management January 2015 survey results

Fabian Society

New Institute President promises focus on education

Tax Foundation