Purchase of own shares

Share this article

Hannah Barraclough provides a refresher on the conditions for capital treatment to apply to a company purchase of own shares

Key Points

What is the issue?

With the gap between capital and income tax rates being so wide, it is more important than ever to understand the purchase of own shares tax legislation to ensure that capital is unlocked at the appropriate and most beneficial rate for the shareholder, depending on the circumstances of the transaction.

What does it mean to me?

Understanding when the purchase of own shares can be subject to capital gains tax instead of income tax can allow advisors and shareholders alike to plan ahead and structure their affairs in a tax efficient manner.

What can I take away?

This article will outline the default tax position when a company purchases its own shares, and also provide a refresher on the conditions for capital treatment to apply.

Let’s say Mrs Pancake and Mr Hazel set up their company, Muffin Limited a number of years ago and Mrs Pancake is now looking to exit the business. She offered to sell her shares to Mr Hazel, but he does not have the cash available to purchase them and no other suitable buyer can be found. Muffin Limited, however, has sufficient cash and Mr Hazel has agreed that the company could buy Mrs Pancake’s shares instead… What are the tax implications?

The difference between the tax rates for income distributions and capital gains is as significant as ever and obtaining a capital tax treatment could reduce the applicable tax rate by up to 28.1%.

The purchase of own shares by a company is therefore one area where the tax liability can vary considerably depending on the circumstances surrounding the transaction and whether capital treatment can be secured.

This article will outline the default income treatment position when a company buys back shares before exploring the conditions that Mrs Pancake will need to meet in order to obtain the ever-coveted capital rate.

Income treatment

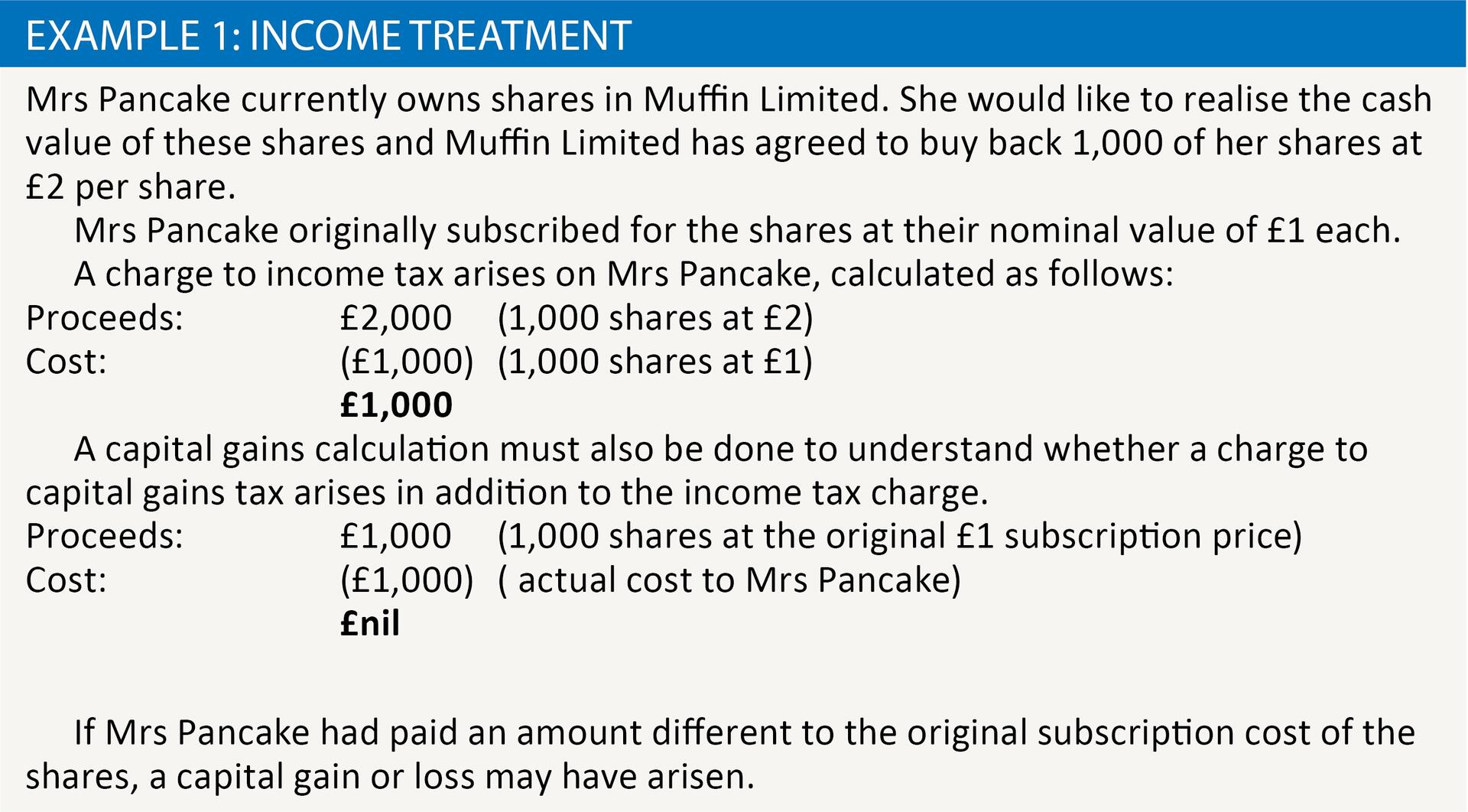

CTA 2010 s 1000 provides that where a company buys back its own shares from an individual shareholder an income distribution occurs. Most share buy backs will therefore result in an income tax charge arising on the distribution, and to the extent that the proceeds exceed the repayment of share capital an income tax charge will arise at the shareholder’s marginal dividend tax rate.

The value of the distribution subject to income tax will be equal to the proceeds arising on the purchase of own shares less the original subscription cost of the shares (more often than not the nominal value).

In addition to being treated as an income distribution, there may also be an exposure to capital gains tax.

In selling their shares to the company, the individual shareholder is disposing of a capital asset and so a capital disposal occurs. As such, a capital gains computation must be prepared to calculate whether the transaction also gives rise to a charge to capital gains tax.

The proceeds in this capital gains tax calculation will be the original subscription price of the shares (regardless of whether the person selling the shares was the original subscriber or not) and the cost will be the base cost to the shareholder (see example 1).

In most cases where the shareholder is the original subscriber, no gain will arise. If the shareholder has not held the shares since they were originally issued, perhaps having purchased them for a price other than the nominal value, a capital gain or loss may arise.

Back to Mrs Pancake. She has always understood that she would pay tax at 10% when she sold her shares as she has ensured that she is eligible for entrepreneurs’ relief, and so the dividend rate for higher rate taxpayers is far more than she was expecting to pay on her exit of the business.

She has heard that in some cases, she may be able to sell her shares back to the company while still only paying tax at 10%.

Capital treatment

Where the relevant conditions as set out at CTA 2010 s 1033 onwards are met, the company purchase of shares would not be considered an income distribution and capital treatment would prevail. Mrs Pancake may be able to pay tax at 10% after all!

Capital treatment can only apply to unquoted trading companies (or unquoted holding companies of trading groups). The buy back must also be wholly or mainly for the benefit of the trade (either the trade of the company making the share purchase or any of its 75% subsidiaries), and it must not be for the avoidance of tax.

The ‘benefit of a trade’ requirement can be particularly subjective and HMRC have offered guidance on this point. This guidance suggests, for example, that a company purchasing shares from a shareholder looking to exit the business (such as in Mrs Pancake’s case) may fall within the definition of ‘for the benefit of the trade’.

It may also be possible to obtain the capital treatment where the purchase of own shares is to fund an inheritance tax liability even if there is no ascertainable benefit to the trade.

There are then four further conditions to be met. This is an ‘and’ test, so each of the conditions must be met for capital treatment to apply.

- Residency: The seller must be UK resident in the tax year of the purchase.

- Period of ownership: The shares must have been held by the seller for five years prior to the purchase. If the shares were received from a spouse or civil partner, look through provisions allow for the length of ownership to be considered in aggregate. This period is reduced to three years if the shares were acquired by will or intestacy.

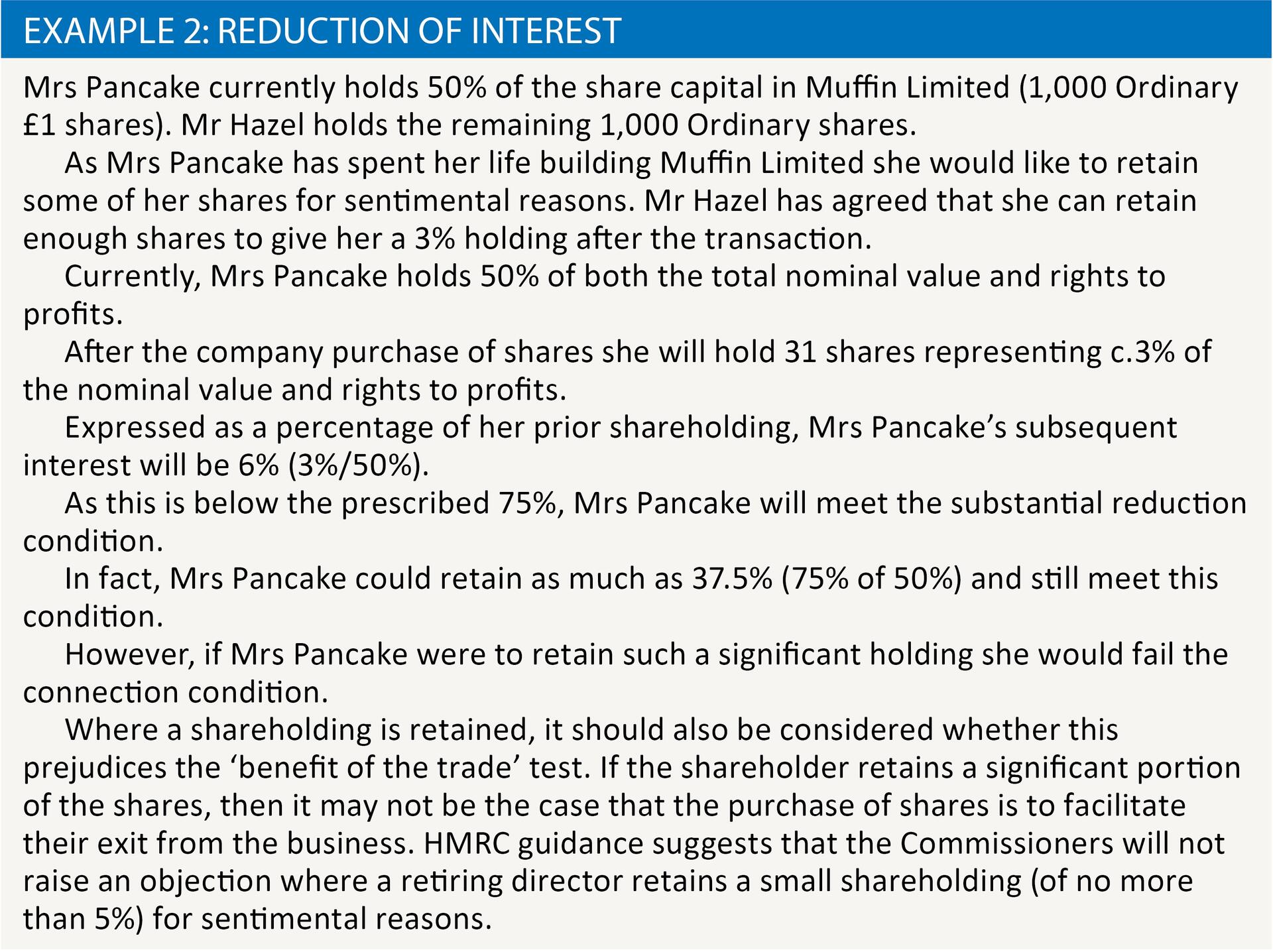

- Reduction of interest: The purchase of shares must substantially reduce the seller’s interest in the company. An interest is taken to be substantially reduced if it is not more than 75% of the seller’s interest prior to the transaction taking place. Both the nominal value held and the entitlement to profits must be reduced, and for the purposes of this condition the seller’s shareholding will be considered in aggregate with the interest of their associates. Example 2 shows how this calculation may work in the case of Mrs Pancake.

- Connection: Immediately after the transaction, the seller must not be connected with the company making the purchase, or any other company in the same group. A person is considered to be connected with the company where they, together with their associates, hold 30% or more of the issued ordinary share or loan capital, including 30% of the voting rights or rights to assets on winding up.

Where all the above conditions are satisfied, no income distribution occurs. Instead, the price paid by the company for the shares will be the proceeds in a capital gains calculation. Should entrepreneurs’ relief apply, the gain will be taxed at the reduced 10% rate in the hands of the shareholder.

The company will also be responsible for notifying HMRC within 60 days of making the payment to the shareholder.

Other considerations

Clearance procedures

The legislation allows for advance clearance to be sought that capital treatment will apply to the transaction (CTA 2010 s 1044).

Where clearance is obtained, HMRC will confirm that the transaction is considered to be for the benefit of the trade and that all other conditions are met.

Anti-avoidance

Where the purchase of own shares is by a close company, the transaction may fall into the scope of Transactions in Securities. For the anti-avoidance provisions to apply, the main or one of the main purposes of the transaction must be the obtaining of a tax advantage.

One of the initial requirements for the capital treatment is that the transaction is for the benefit of the trade. It is therefore unlikely that it would be considered that the main purpose of the transaction is to obtain a tax advantage.

Advance clearance can be sought that HMRC will not seek to apply the Transactions in Securities rules under ITA 2007 s 701 alongside the clearance under CTA 2010 s 1044 to confirm that the transaction is for bona fide commercial reasons.

It should also be noted that where the vendor is a corporate shareholder, capital treatment will always apply (Statement of Practice 4 [1989]).

Interaction with other taxes

As the company will be purchasing shares, the transaction will fall within the scope of stamp duty. The consideration for the share buy back may therefore be subject to stamp duty at 0.5%.

Legal requirements

When considering a company buy-back of shares, it is important to consider the legal requirements imposed by Companies Act 2006. The purchase of own shares will be funded by the profit and loss reserve and so the company must have sufficient distributable reserves to cover the purchase price of the shares. CA 2006 s 691 also requires that the shares bought back must be paid for in cash at the time they are purchased, and cannot be settled by deferred consideration or instalments. If the shareholder intends to loan the money back to the company following the company purchase of shares, the cash must still be moved between company and shareholder and back again or the transaction may fall foul of CA 2006.

The articles of association should also be checked to ensure the articles do not prohibit the desired buy-back of shares.