Putting the plan in place

Share this article

Lindsey Holmes looks at the benefits offered by discounted gift trusts

Key Points

What is the issue?

Some clients have a potential inheritance tax liability, but are unable to gift away capital, as they rely on the income they receive from it.

What does it mean to me?

Understanding how one type of scheme can enable a client to remove capital from their estate, whilst maintaining access to a regular withdrawal.

What can I take away?

How tax advisers can work with a financial planner/wealth manager to establish a discounted gift trust. Gain a better understanding of the practicalities of setting up a plan.

With the recent introduction of the residence nil rate band, inheritance tax planning is firmly at the top of the agenda. However, the challenge for many clients is how they can undertake planning, whilst retaining sufficient access to income and capital to provide for their needs. The uncertainty over life expectancy compounds this issue. According to the Office of National Statistics 2014-16 tables, the average life expectancy for a 65 year old is 83.5 for a man and 85.9 for a woman. However, these figures are a national average and the wealthy are likely to live longer than this. In addition, there is also the uncertainty over health in future years and whether care fees will need to be paid.

It is difficult to implement successful schemes for inheritance tax planning that have an impact, but are not attacked by HMRC. However, HMRC has always been comfortable with discounted gift trusts.

Plan basics

Packaged discounted gift trusts are offered by most major life assurance companies, the majority providing an onshore and offshore version. The plan involves a client putting a capital lump sum into a life assurance bond, which is placed into trust. The client then receives a fixed regular withdrawal for life, provided sufficient capital remains. The client does however lose access to the capital, other than the regular withdrawals. The plan can be established on a single life basis, or jointly with a spouse or civil partner.

The capital placed in the plan is deemed to fall into two parts, which are each treated differently for taxation purposes.

First part of plan

The first part is deemed to represent the withdrawals that the client is likely to receive back during their lifetime. On this basis, this part of the capital falls out of the client’s estate immediately and is known as the ‘discount’. As the size of the discount represents the estimated level of withdrawals the client will receive back, it therefore depends on the client’s age, life expectancy and level of withdrawals. The discount also used to be based on gender, as women live longer, but following the European Court of Justice ruling, from December 2012, the discounts are gender neutral. Due to the fact there is an assessment of life expectancy, the application for the plan is subject to medical underwriting at the outset and the client does need to be in reasonable health.

It is generally considered that a client is only insurable for life cover if they are under the age of 90. Care needs to be taken for those with health issues. For example, if an 86 year old applicant has a heart condition, the life company may deem them to have an age for health purposes of four years older; a process called ‘rating’. In this case, taking the applicant over 90 and making him/her unsuitable for life cover and therefore a discount. Usually in this scenario, it would not make sense to establish a plan.

HMRC guidance is that the value of the transfer is to be determined by the loss to the estate principle outlined in s.3(1) Inheritance Tax Act 1984 (IHTA) which is the amount invested by the settlor, less the open market value of the income stream. It is assumed that a sale of the rights has taken place. A purchaser of an income stream would want to take out life cover on the settlor to protect their investment and if they are over 90, they are deemed to be uninsurable.

The age 90 principle was established by the case HMRC v Bowyer in 2008, whereby Marjorie Bowyer, a lady who was almost 91 years old established a discounted gift trust. The case was fully medically underwritten and due to health issues, she was deemed to have a life expectancy of a 103 year old. Consequently, she was given a discount based on her having another two to three years to live. Sadly, Mrs Bowyer died five months after. HMRC successfully challenged the case arguing that, given Mrs Bowyer’s rated age of 103, there would have been no one willing to purchase the income stream and believed the discount should have been almost nothing.

The Watkins and Harvey v HMRC case in 2011 is also of note. Mrs Watkins was only 89 when effecting the scheme, but died two years later. HMRC successfully argued that the income stream would have no value in the open market and Watkins and Harvey lost at the High Court.

Usually, for younger clients, even if the settlor fails to survive seven years, as long as there has been a full medical disclosure and the plan has been fully underwritten at outset, the discounted portion of the scheme should fall outside of their estate. Of course all plans are potentially subject to HMRC investigation.

If a joint plan is established, the discounts are calculated separately for each spouse, based on their age and life expectancy. So for a couple investing £100,000, £50,000 is deemed to come from each spouse. The discount for each is then applied to their £50,000 share.

Second part of plan

Although the first part of the capital placed into the plan falls outside of the client’s estate immediately, if a discretionary trust version is used, the second part is deemed to be a chargeable lifetime transfer (CLT). If this second part is less than the prevailing nil rate band, then there should be no immediate charge to inheritance tax. As it is only this second part which is measured against the nil rate band, it provides scope to remove larger amounts from the estate, without an immediate tax charge.

The other option, aside from a discretionary trust, is to use a bare trust version, where there is certainty over beneficiaries. This creates a potentially exempt transfer (PET), rather than a CLT. With both plans, the second part should fall outside of the client’s estate after seven years, subject to no relevant failed PETs in the case of the CLT version.

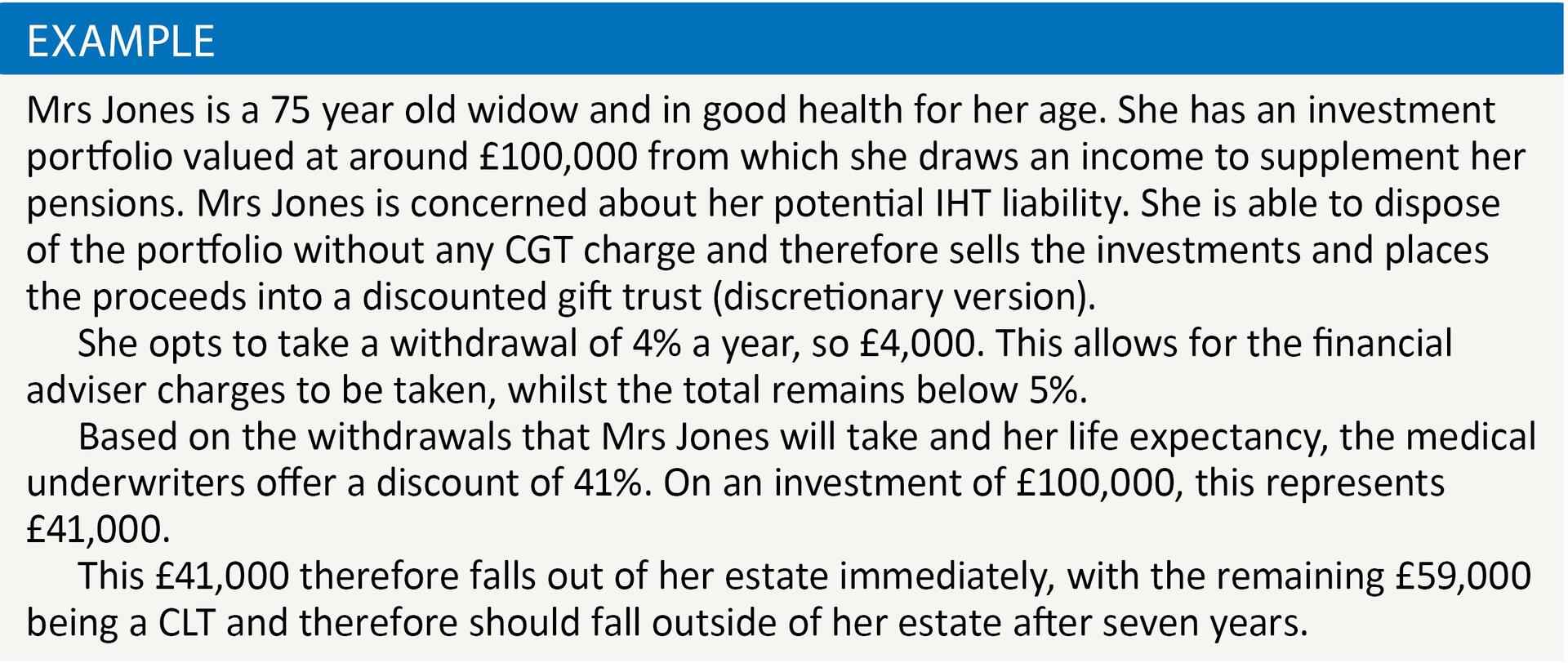

See the example below.

Level of withdrawals

The adviser must carefully consider what level of ongoing withdrawal should be taken from the scheme. As the underlying investment is a life assurance bond, to avoid a chargeable event, the maximum withdrawal is 5% per policy year of the initial investment value. Any tax charge would be levied against the settlor or settlors of the plan, whilst living. This may not be a significant issue for low income settlors where an onshore bond is used and 20% tax is deemed to have been paid within the bond. Where an offshore bond is used and the settlor has a relatively low income, he/she may be able to utilise the savings nil rate band.

It is important to consider that the ongoing financial adviser charge needs to be paid for by the trustees from the bond and is included in the 5% withdrawal limit. Most financial advisers typically charge an annual ongoing advice fee of 0.75% to 1%, meaning that the client has to reduce their withdrawals to below 5% to allow for this. Otherwise, a tax charge will arise. It is a good idea to consider fixing the financial adviser charge as a percentage of the initial investment value, due to the fact that the 5% tax deferred withdrawal allowance is based on the initial investment amount. If the adviser charge is a percentage of the current value and there is significant investment growth, combined with client withdrawals, the 5% limit may be breached. The charges levied by the bond provider do not count towards the 5%.

In setting the level of withdrawals, the charges applying to the bond, levied by both the bond provider and the financial planner, must be considered. One must then look at the risk profile of the investments within the bond. If the withdrawal is set at 5% a year in total, and the risk profile is fairly low, there will be low growth potential for the investments and consequently, a high risk of capital erosion in the longer term. This could mean that little is available to be passed on to beneficiaries. As withdrawals cannot be altered, deciding on the right level of withdrawals can be difficult, especially as one does not know how the underlying investments will perform. Also, given the charges, unless the trustees are prepared to invest at least 60% of the trust assets in equities, the growth after charges is unlikely to offer the opportunity for reasonable regular withdrawals.

Some plans do offer the option for the settlor to waive the withdrawals for a period, but the amount waived is deemed to be a further CLT or PET. Some discounted gift trusts also allow small ad hoc payments to be made to beneficiaries. It all depends on the provider.

Capital extraction after the settlor’s death

As the underlying investment is a life assurance bond, there will be tax consequences when it is surrendered, or when withdrawals are taken above the 5% allowance. It is very wise to select at least four fairly young lives assured on the bond and also to choose people that do not travel together. This is due to the fact that the bond and therefore plan, ends on the death of the last life assured. The capital can only be released from the plan after the death of the settlor. As with all life assurance bonds, a tax efficient way of capital extraction is to assign segments of the bond to younger/low income beneficiaries. They can then surrender the segments in their own name more tax efficiently. Conversely, if the beneficiaries are all likely to be higher or additional rate taxpayers and subject to further income tax on bond gains, this reduces the tax efficiency somewhat. As with all investment bonds, a chargeable event only occurs on death of the last life assured, surrender of the bond, assignment for money or money’s worth, maturity, or withdrawals taken in excess of the 5% tax deferred allowance. Most providers of discounted gift trusts also offer the option of using a capital redemption bond.

Which clients could suit this plan

Whilst the very wealthy can often afford to gift away large sums, either directly or into trust, there are many others with an inheritance liability that rely on the income they receive from investments. For clients with an investment portfolio who do not require access to the capital, but require an income to supplement state and private pensions, a discounted gift trust can be an ideal solution.

Where a couple in a marriage or civil partnership benefit fully from the residence nil rate band, there is usually little point establishing these plans where total assets are £1 million or less. However, there will be many clients without children and unable to benefit from the residence nil rate band. In addition, single clients will only have one residence nil rate band and nil rate band to utilise. It is important to note that a discounted gift trust is only suitable for clients that require a regular withdrawal to supplement their income, otherwise the withdrawals will rebuild the value of their estate and the planning will have made no sense. Also, as the withdrawals the client receives are capital withdrawals from an investment bond, they cannot be gifted under the normal expenditure out of income exemption.

One significant benefit of this type of scheme is that the investments can be well balanced and not overly risky. Indeed many clients who possess a portfolio of collective funds from which they receive an income, can replicate the same portfolio within the plan. Of course, the adviser needs to be mindful that the investment advice is being provided to the trustees and must balance the needs of all beneficiaries. This contrasts strongly with a Business Property Relief scheme, where the risk profile is significantly higher and often unsuited to an elderly client. It must be borne in mind that for elderly clients, there is usually little point in incurring a capital gains tax charge when selling existing investments and the gains’ position needs to be carefully considered before replacing investments.

Given the costs of setting up a plan and the administration involved in running a trust, it is only really practical to establish a plan for upwards of £100,000. It is also essential that clients are left with good levels of cash reserves to cover unforeseen circumstances, such as care in the home or nursing home costs.

Working with a financial planner/wealth manager

It is important to emphasise that advice on discounted gift trusts can only be provided by FCA approved financial advisers, due to the investment element. Tax advisers are not authorised to provide investment advice. However, this provides a fantastic opportunity to network with financial planners and wealth managers.

Summary

In summary, for clients with a potential inheritance tax liability and who require an income, a discounted gift trust can be an ideal solution.