Ready for the impact

Share this article

Caroline McCabe considers the impact of IFRS16 on the corporate interest restriction

Key Points

What is the issue?

The new international accounting standard on leases, IFRS 16 will mean many more leases are accounted for as finance leases (rather than operating leases), with depreciation and finance charges (rather than rent) posted through the income statement. This could increase tax costs, particularly where the CIR applies to restrict the amount of finance costs deductible for tax purposes.

What does it mean to me?

It is hard to say exactly how each group will be affected. Accounting for leases as finance leases rather than operating leases will increase interest costs, meaning more finance costs are potentially subject to restriction under the CIR but it will also increase tax-EBITDA, which could lead to a smaller disallowance.

What can I take away?

The rules are complex to begin with and there remains some uncertainty regarding the tax impact, given that HMRC has consulted on how the CIR rules need to be adapted in the light of IFRS 16, but has not yet responded to comments. Property-intensive businesses, particularly the retail and leisure sectors, are likely to be most affected by the changes.

International Financial Reporting Standard 16 (IFRS 16) is the new international accounting standard on leases. The standard is effective for periods beginning on or after 1 January 2019 and is already available for early adoption (if IFRS 15 Revenue from Contracts with Customers is also applied). The details of IFRS 16 are beyond the scope of this article but in order to understand the tax consequences of adopting the standard, a basic explanation of the changes is required.

The main impact of the change for companies adopting IFRS 16 will be that the vast majority of leases currently accounted for as operating leases (‘off Balance Sheet’) will instead be accounted for as finance leases. In other words, most leases will be brought ‘on Balance Sheet’, meaning a right-of-use asset and a lease liability will be recognised in the financial statements and both will be unwound to the income statement over the period of the lease.

The change could have a significant impact on a company’s income statement:

- What is currently posted as a single overhead expense of rent will now be posted as a mixture of depreciation and finance lease interest costs

- The company’s EBITDA will increase as leasing costs are now outside of that measure.

- The company’s interest expense will increase.

What might this mean for corporation tax?

Depreciation is not allowable for corporation tax purposes, which may lead to an increased tax cost for many companies, although capital allowances may be available in some cases. The Government has confirmed in Leasing: Tax response to accounting changes – summary of discussion document responses and consultation published on 1 December 2017, that the current tax treatment of leased plant and machinery will continue. While it is not yet clear that the current treatment of fixtures and fittings for capital allowances purposes will continue, the Government has not, so far, ruled it out. The starting point is that finance costs incurred wholly and exclusively for the purposes of the company’s trade or business are allowable for corporation tax purposes but there are a number of specific provisions that can preclude or restrict a deduction. One of these is the corporation interest restriction (CIR), which treats finance charges in respect of finance leases as tax-interest, potentially subject to a restriction.

The CIR is a notoriously complex area of tax law but the article ‘New Limit’ in the November 2017 issue of Tax Adviser by Adeline Chan and Roger Murray provides an excellent overview. Briefly, the CIR became effective from 1 April 2017 and applies when the UK companies within a worldwide group (defined using international accounting standard principles) have aggregate net tax-interest expenses above the £2 million de minimis limit. Where that limit is exceeded, the UK group’s allowable net tax-interest expenses are limited to a percentage of the UK group’s ‘tax-EBITDA’ (broadly the group’s UK taxable profits before interest, capital allowances and amortisation) subject to a modified debt cap. The default fixed ratio method uses 30% to calculate this restriction, although highly-leveraged groups can choose to adopt the group ratio rule instead.

One would therefore expect the total disallowance under the CIR to be affected by lessees transitioning to IFRS 16, although the exact effect on each group is hard to predict; tax-interest will increase, potentially leading to a greater disallowance under the CIR but the changes will also lead to higher tax-EBITDA, which may in fact reduce the disallowance. To complicate matters further, current legislation in FA 2011, s53 negates changes in lease accounting standards for tax purposes, meaning leases currently accounted for as operating leases would continue to be treated as operating leases for tax purposes. While that may provide a better tax outcome, it would require affected companies to keep separate accounts for tax purposes, increasing their compliance burden. HMRC has indicated that it expects this section to be repealed with effect from 1 January 2019, so the accounting changes brought about by adopting IFRS 16 will indeed lead to changes in tax treatment. However, early adopters should continue to prepare their tax returns on the basis of the old accounting rules, distinguishing between operating and finance leases.

Impact for users of UK GAAP

Some entities which continue to report under UK GAAP will still be caught within the scope of these changes if they account for leases under Financial Reporting Standard (FRS) 101. Users of FRS 102 will continue to apply the current leasing model, making the distinction between operating and finance leases, although this may in due course be aligned with IFRS 16.

How might lessors be affected?

Under IFRS 16, the accounting treatment for lessors is unlikely to change in most cases, so lessors may continue to account for a property lease as an operating lease, even though their tenant accounts for the same lease as a finance lease.

This asymmetry in the accounting treatment could lead to an asymmetry in the tax treatment; landlords could be subject to tax in full on UK property income, albeit that same rent may not have been fully deductible for their tenant. Where property is rented out intra-group, this may lead to behaviour changes if the group suffers an actual tax cost in the form of an interest restriction and some lessee companies within groups may choose to adopt FRS 102 where possible for their entity-level accounts in order to mitigate against this asymmetry.

HMRC consultation

Recognising that the accounting changes introduced by IFRS 16 could have a major impact on the corporation tax landscape, HMRC launched two consultations: one on the broader tax consequences of the changes, taking into account capital allowances, etc., and another looking specifically at how the CIR might be affected by the changes.

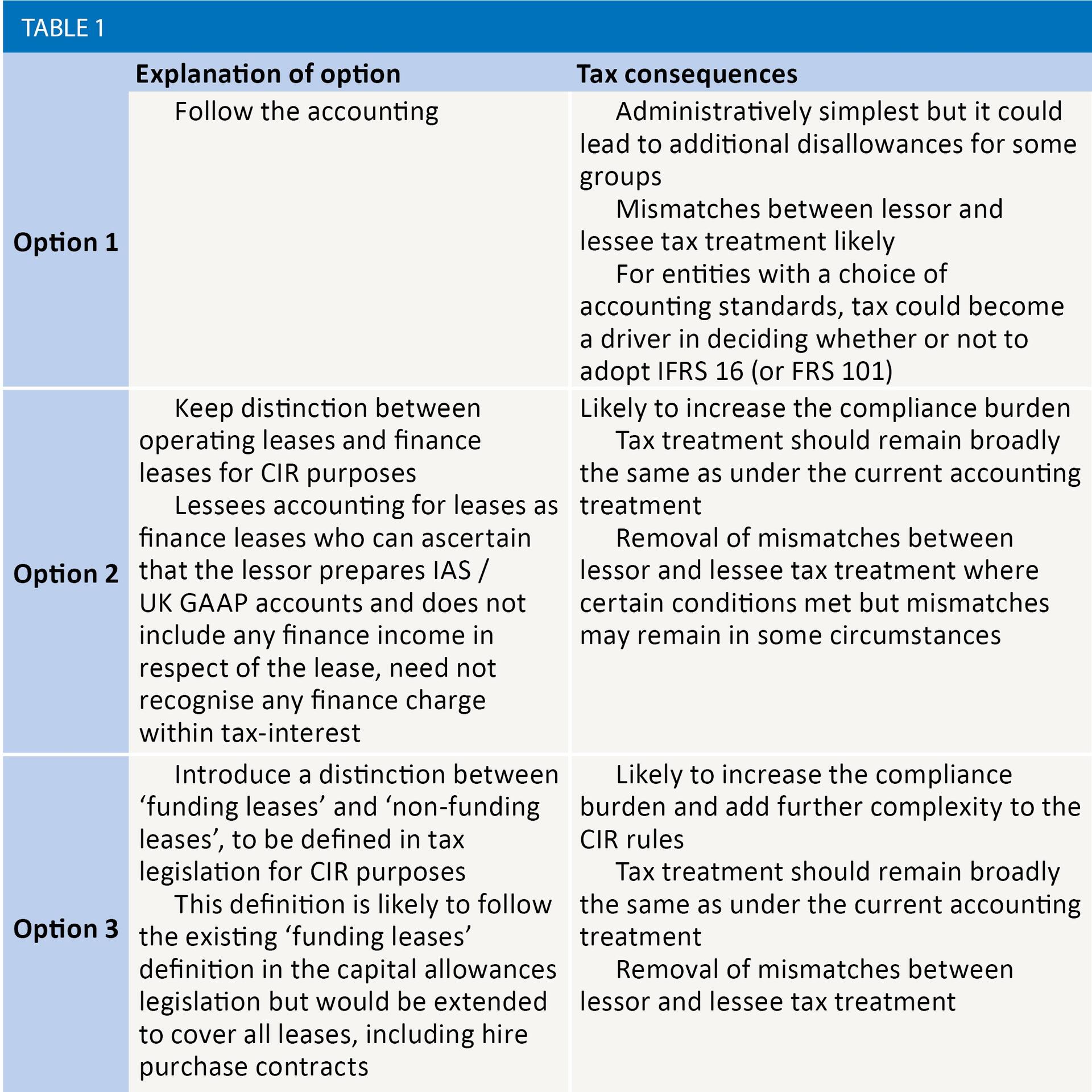

The consultation specifically considering the impact of the changes on the CIR rules laid out three options for amending the CIR in light of the introduction of IFRS 16, summarised in table 1.

HMRC currently expects that any changes made to the CIR rules would apply to all companies within the charge to corporation tax; and not just those adopting IFRS 16. At the time of going to press, HMRC’s summary of responses has not been published but is expected later this year, along with draft legislation. Both of which should provide greater clarification and guidance.

Significance of the impact

The British Property Federation (BPF) estimates that UK business pay approximately £25 billion in rent each year, so the impact across the UK economy could be significant. Property-intensive companies such as retailers and leisure providers, which lease their premises, will be among the most heavily impacted groups. One estimate of the impact on property occupiers suggested that up to £4 billion additional interest costs could be posted through income statements of UK companies each year.

Rent is a true cost of operating a business, and those businesses operating from physical premises should not be penalised by the tax system, particularly at a time when retailers are struggling. Moreover, the motivation behind introducing the CIR was to prevent large multi-national groups from shifting profits to low-tax jurisdictions but rental income and expenses are taxed in the same jurisdiction, meaning there is no possibility of shifting profits outside the UK. It is easy to see why special treatment is necessary to ensure fair tax treatment for property leases but achieving this without adding to the complexity of the CIR is a significant challenge.