Welcome incentive

Share this article

Caroline McCabe provides an overview of the new investors’ relief and the opportunities it provide

Key Points

What is the issue?

The introduction of a new relief to encourage external investment in entrepreneurial companies, providing a 10% CGT rate on qualifying gains.

What does it mean to me?

New opportunities for tax-efficient investments for individuals and new ways to raise money for entrepreneurial companies.

What can I take away?

Some of the rules are complex, in particular those on share reorganisations and receipts of value, and demand close attention to ensure access to the relief is not inadvertently lost.

Finance Bill 2016 introduces a new relief to encourage investment in entrepreneurial companies by external backers. Known as investors’ relief, it applies a lower rate of 10% capital gains tax (CGT) to disposals of qualifying shares by individuals, subject to a lifetime cap of £10m worth of gains. This cap is separate from the one that applies to £10m entrepreneurs’ relief (ER). Unlike ER, investors’ relief does not require the investor to be an officer or employee of the company or hold a minimum holding in the company.

As with many tax reliefs, various conditions must be satisfied. ‘Qualifying shares’ must meet these provisos:

- The investor subscribed for the shares wholly in cash and they were fully paid up at the issue date (so new companies should not issue shares until they have a bank account to receive payment).

- The investor has held the shares continuously from subscription until the disposal (‘the share-holding period’).

- The shares were issued on or after 17 March 2016.

- At the issue date, none of the company’s stocks or shares were listed on a recognised stock exchange.

- The shares were ordinary shares at issue and immediately before the disposal.

- The issuing company was a trading company or the holding company of a trading group (broadly similar to the definition for ER purposes) at the date of issue and throughout the share-holding period.

- Throughout the share-holding period, neither the investor nor a person connected with him was an officer or employee of the issuing company.

- The share-holding period is at least three years (counted from 6 April 2016 for shares issued before then).

Anti-avoidance rules stipulate that both the subscription and the issue must be for genuine commercial reasons and not for the avoidance of ‘tax’, which for these purposes is not limited to CGT. The shares must also be issued by way of a bargain at arm’s length. These rules ensure that the relief is targeted to encourage genuine commercial investment.

If all of the above conditions are met, except that the share-holding period is fewer than three years, the shares are ‘potentially qualifying shares’ and may become eligible for investors’ relief in future. Shares that are neither qualifying nor potentially qualifying shares are known as ‘excluded shares’ and will never become eligible for the relief.

Disposals in action

If not all of the shares disposed of are qualifying, investors’ relief is available on Q/T of the gain, where Q is the number of qualifying shares and T is the number disposed of. If only part of the share-holding is disposed of, Q is treated as the lower of the qualifying shares in the holding immediately before disposal and the number of shares disposed of.

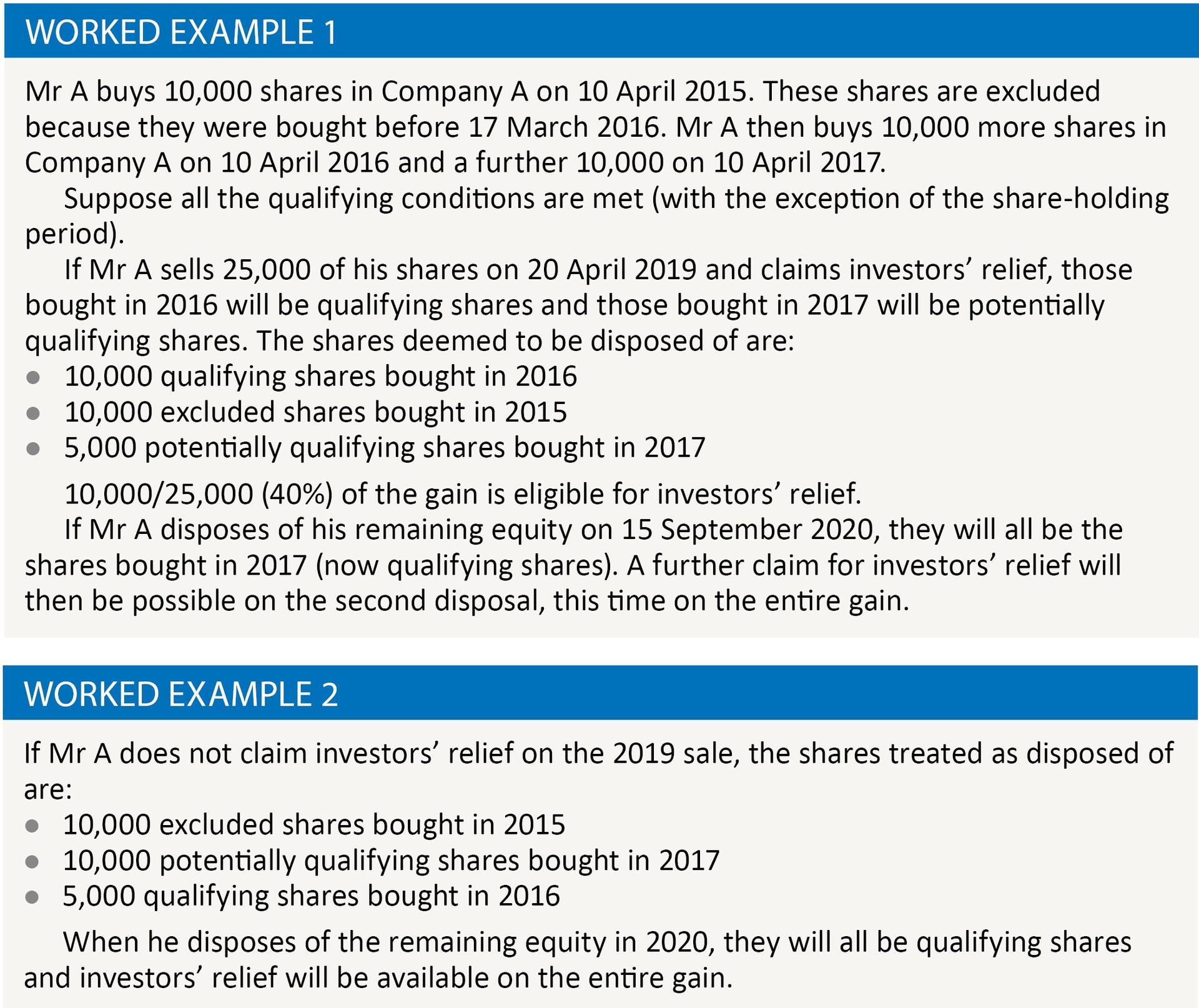

Previous disposals can complicate the situation. It is first necessary to determine how many of each type of share remains in the holding at the time of the current disposal. If an investors’ relief claim has already been made, the earlier disposal is deemed to comprise, first, of qualifying shares, then excluded shares, and finally potentially qualifying shares (with later-acquired shares deemed to be disposed of before those acquired earlier). This gives potentially qualifying shares the maximum possible chance to become qualifying shares. Worked example 1 shows this scenario.

If there has been no previous investors’ relief claim, the earlier disposal is treated as made up first of excluded shares; then potentially qualifying shares (again, shares acquired later take priority over those acquired earlier); and finally qualifying shares. See worked example 2.

Reorganisations

Let us say that, before a disposal, there has been a reorganisation of a company’s share capital (within the meaning of TCGA 1992 s 126) and no new consideration was given for the new share-holding. In this case, the new share-holding is treated as having the same proportions of qualifying, potentially qualifying and excluded shares as the original share-holding before the reorganisation.

Shares in the new company are deemed to have been subscribed for at the same date and held continuously for the same period as the corresponding shares in the original company. Therefore, there should be no automatic disqualification from investors’ relief, as long as no consideration is given for the new shares. However, for the purposes of investors’ relief, any shares received in exchange for consideration are treated as having been issued when they were actually issued. This would jeopardise an individual’s ability to claim investors’ relief on a disposal made within three years of the reorganisation.

New ss 169VL to 169VN explain the treatment after a share exchange within the meaning of TCGA 1992 s 135 or a scheme of reconstruction in line with TCGA 1992 s 136. These rules include a requirement that specific qualifying conditions must be met at two stages: first, in relation to the original share, from its issue date until the reorganisation or reconstruction; and second, in relation to the new share, from the reorganisation or reconstruction to the disposal. Great care must be taken in these situations to ensure that access to investors’ relief is preserved.

An election can be made to disapply the treatment outlined. This ensures that investors’ relief is not lost if the original share-holding would have qualified at the time of the reorganisation but the new one does not (or might not). This would be the case if consideration is given for the new shares after a reorganisation. If this election is made, a gain arises and investors’ relief can be claimed. The disadvantage of making this election is that no consideration will have been received with which to pay the tax due.

Receipts of value

New Sch 7ZB sets out cases when shares that ordinarily would be treated as qualifying or potentially qualifying shares are in fact treated as excluded shares. Broadly, this occurs if the investor ‘receives value’ in some form from the company at any time in the period starting one year before and ending three years after the shares are issued (the ‘period of restriction’). This anti-avoidance measure ensures that the cash subscribed for the shares increases the funds available to the company.

The circumstances in which an investor receives value are listed at para 2 of new Sch 7ZB and are based largely on the definition that applies for the enterprise investment scheme. It can be ignored if the total value received during the period of restriction is of ‘insignificant value’ (no more than £1,000). There are also rules on receipts of value under which, broadly, the investor restores to the company the value received, other than through the share subscription itself. This is certainly an area that demands close attention.

Conclusion

Although the higher rate of CGT on share disposals was cut from 28% to 20% from 6 April 2016 (almost halving the differential between that and the 10% rate for gains on which investors’ relief is claimed), investors’ relief is likely to become an increasingly important incentive to finance British companies. A major advantage is that it does not require the investor to be an officer or employee of the company (as ER does), which is often inappropriate for the company, the investor, or both.

However, investors and issuing companies alike must ensure that the relief is not accidentally lost. Areas demanding particular care are the rules on receipts of value and reorganisations of share capital.